It's great to be king

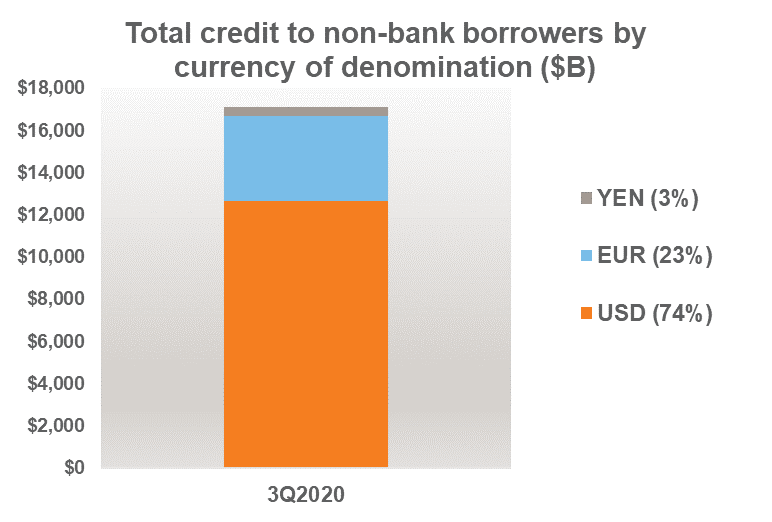

The U.S. dollar (USD) plays a vital role in global finance. It functions as the world's reserve currency and is the currency of choice for international commerce. As Figure 1 highlights, nearly three-quarters of global non-bank lending debt is denominated in the USD.

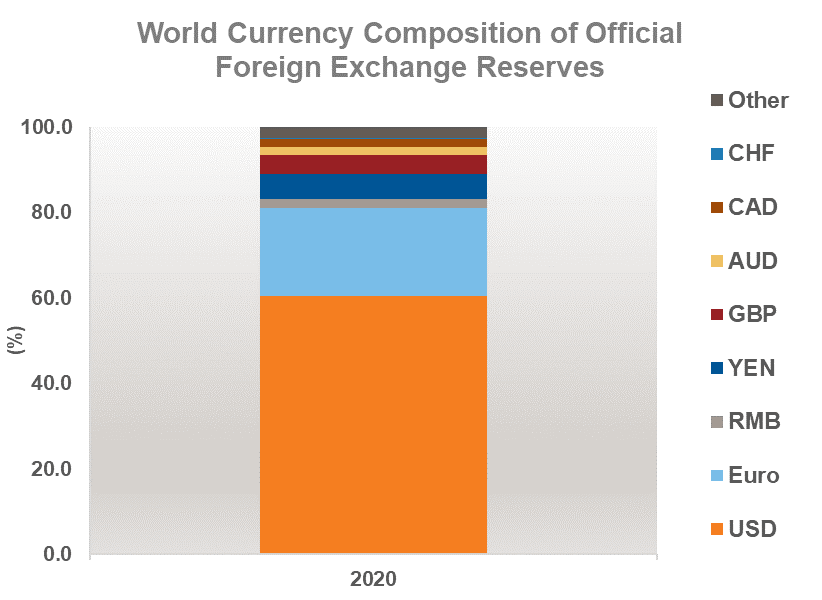

Its primacy in global trade also necessitates foreign central banks to hold the USD as part of their foreign exchange (FX) reserves. In fact, 60% of global central banks' foreign exchange reserves are invested in the USD as Figure 2 shows. The Euro is a distant second at 20%. It’s noteworthy that despite China's economic ascent since 2000, the Renminbi's (RMB) share of global FX reserves is only 2%. While it's reasonable to expect the RMB and other high-growth nations' currencies to continue their advance, it seems clear that the USD's reserve currency status is secure for the foreseeable future.

(Click on image to enlarge)

Source Figure 1: Bank of International Settlements (BIS), Russell Investments, as of 3Q2020. Yen and Euro data were converted to USD based on the conversation rate as of 3Q2020. Source Figure 2: IMF, Russell Investments. Note 2020 as of 3Q2020.

The U.S. dollar and the business cycle

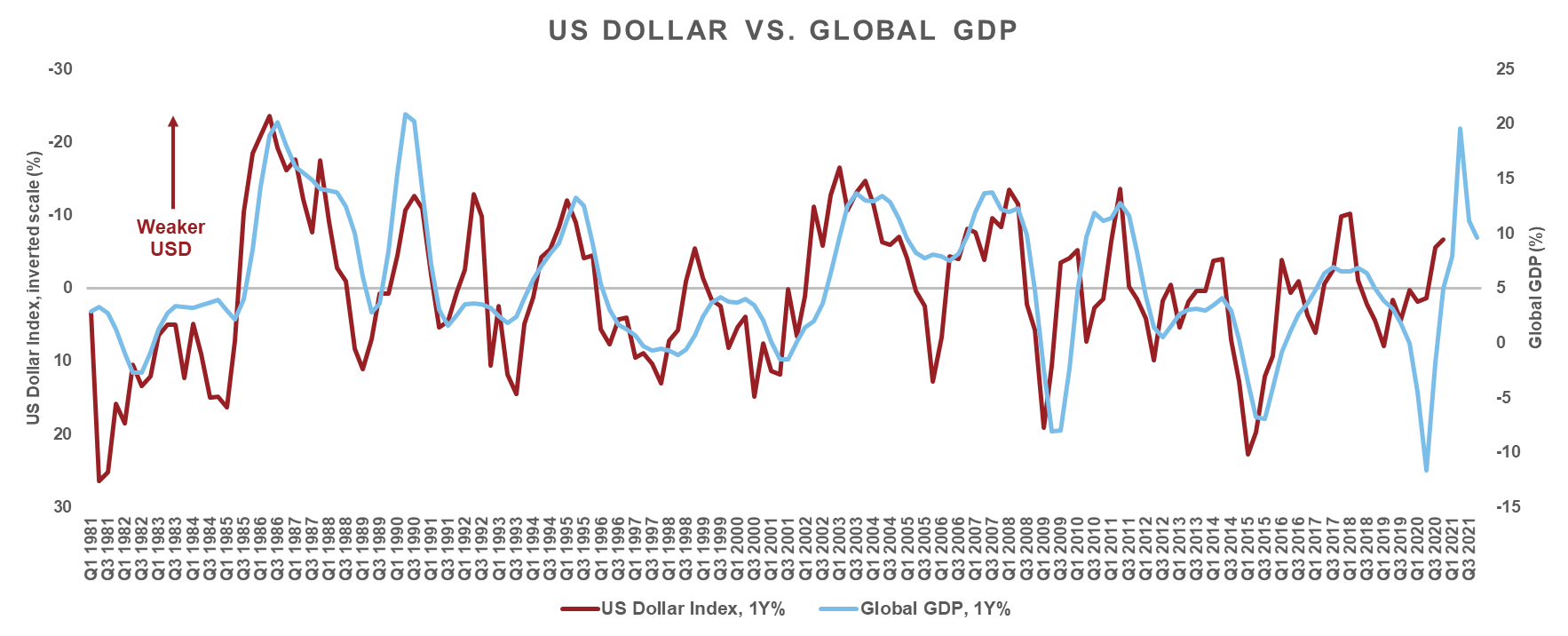

The USD's wide acceptance for international commerce makes it a highly sought-after currency, especially when economic conditions are deteriorating. For this reason, it's said the USD is a counter-cyclical currency, meaning it trends in the opposite direction of the business cycle: strengthening as the business cycle slows and weakening as the economic outlook improves. This inverse relationship is illustrated in Figure 3. A weaker USD corresponds with improving global growth, while a stronger USD suggests a slowdown in growth.

(Click on image to enlarge)

Source: Refinitiv DataStream, Russell Investments. As of 4Q2021. GDP based on Oxford Economics data, estimated from Q1 2020.

The U.S. dollar and equity market trends

If we consider that USD weakness suggests an improving global business cycle, then it's reasonable to expect that would favor international equities over U.S. equities. This makes intuitive sense. As the USD depreciates, global financial conditions ease. This is in part because servicing US-denominated debt, of which there is plenty as shown in Figure 1, becomes a little less onerous. The relationship between the USD and U.S./international equities relative performance is illustrated in Figure 4. As suggested, a depreciating USD trend generally corresponds with international equities outperforming the U.S., and vice versa.

(Click on image to enlarge)

Source: Refinitiv DataStream, Russell Investments. As of December 2020. Returns are based on 2 years annualized return for USD and 2 years annualized return differential for MSCI USA les MSCI EAFE.

The outlook: International vs. U.S. and growth vs. value

Figure 4 also shows that U.S. equities have steadily outperformed international equities since 2008. Due to the higher concentration of cyclical sectors like financials and industrials, international equities benefit from accelerating economic activity. However, that has not been the case for some time. The global economy started to lose momentum around mid-2018, suggesting the economic expansion had transitioned into the late stage. Economic growth was ultimately punctured by the pandemic-induced global recession. As such, the business cycle backdrop of the last three years disproportionately benefited the U.S. stock market for three main reasons.

First, the U.S. has a higher allocation to growth sectors linked to technology and health care, which benefit as economic activity slows—this was the environment before the pandemic. Second, Covid-19 is a health care crisis that effectively chocked mobility to varying degrees—this has been our reality since the pandemic started. The culmination of these scenarios has been a tremendous force boosting U.S. equities relative to international.

With that said, we believe U.S. equity outperformance has mostly run its course. The global economy quickly transitioned from the slowdown of 2018 to 2019 into a deep but short-lived recession in 2020 and is now early in an economic recovery. Moreover, a recuperating business cycle suggests USD weakness ahead. Together, these trends favor international shares over U.S. shares.

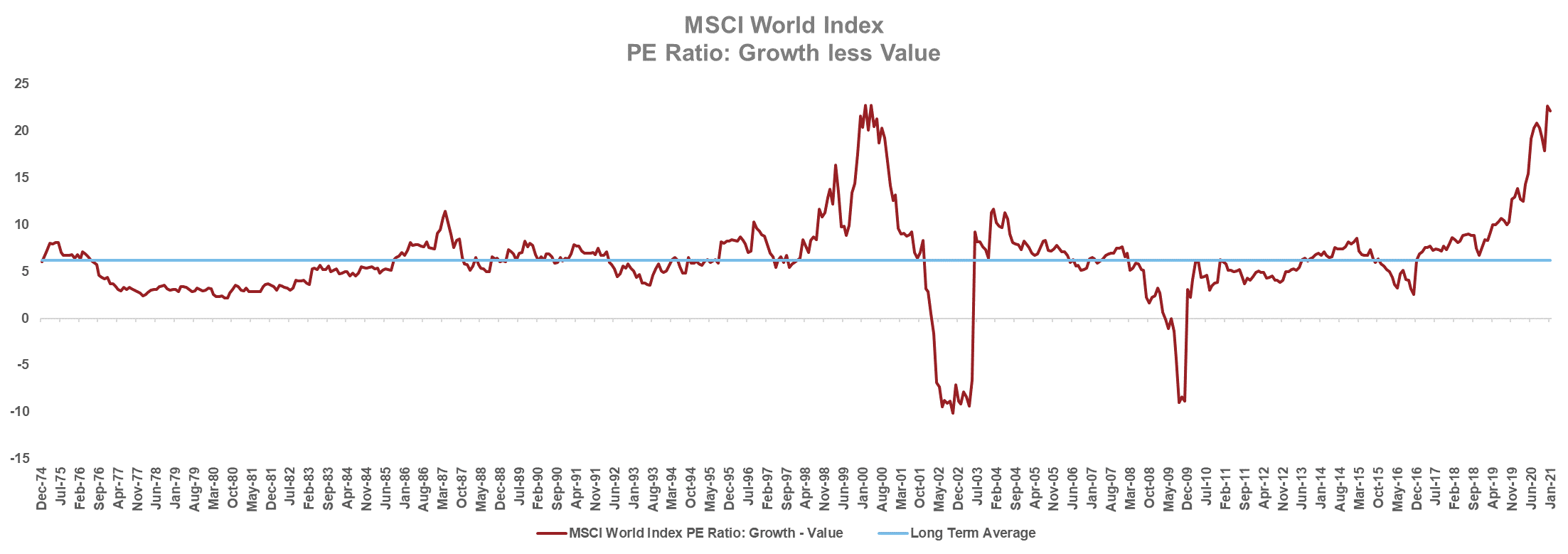

It is also worth mentioning factor performance, specifically, growth versus value. U.S. large-cap growth has been a winning trade, and even more so since the pandemic began. We believe that could change with the reopening of the global economy. The value factor has a high allocation to cyclical sectors, which have lagged miserably but now possess significantly better valuation versus their growth counterpart.

As Figure 5 illustrates, based on the price-to-earnings (PE) ratio, the value factor has not traded at such a striking discount to growth since the dot-com bubble of the late 1990s. Additionally, the value factor is bolstered by encouraging business cycle trends over the next 12-18 months. Coincidently, the rotation away from growth and toward the value factor also supports international equities due to their more significant cyclicality.

(Click on image to enlarge)

Source: Refinitiv DataStream, Russell Investments. As of January 2021.

To summarize, we believe the business cycle recovery has room to run. We expect the USD will face cyclical challenges as the global economy strengthens. Therefore, improving prospects for the global economy and a weaker USD, collectively, favors international equities over U.S. equities—and by extension, value over growth.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and ...

more

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

The MSCI Word Index captures large and mid cap representation across 23 Developed Markets (DM) countries*. With 1,600 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. With 620 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the US.

The MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries* around the world, excluding the US and Canada. With 874 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The U.S. Dollar Index (USDX) is a measure of the value of the U.S. dollar relative to the value of a basket of currencies of the majority of the U.S.'s most significant trading partners.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2021. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11810

Disclaimer: Opinions expressed by readers don’t necessarily represent Russell’s views. Links to external web sites may contain information concerning investments other than those offered by Russell Investments, its affiliates or subsidiaries. Neither Russell Investments nor its affiliates are responsible for investment decisions with respect to such investments or for the accuracy or completeness of information about such investments. Descriptions of, references to, or links to products or publications within any linked web site does not imply endorsement of that product or publication by Russell Investments. Any opinions or recommendations expressed are solely those of the independent providers and are not the opinions or recommendations of Russell Investments, which is not responsible for any inaccuracies or errors. Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

Investing in capital markets involves risk, principal loss is possible. There is no guarantee the stated outcomes in the presentation will be met.

This is a publication of Russell Investments. Nothing in this publication is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The contents in this publication are intended for general information purposes only and should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional concerning your own situation and any specific investment questions you may have.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

less