The Case For The Canadian Dollar Remains Strong From Good Economic News

While the U.S. inaugurated its 46th President, the Bank of Canada attended to more mundane matters. The Bank of Canada released its latest Monetary Policy Report (MPR) and along the way delivered some good news for the Canadian economy. For a brief moment, the news was good enough to drive USD/CAD, the U.S. dollar versus the Canadian dollar (FXC), back to levels last seen April, 2018.

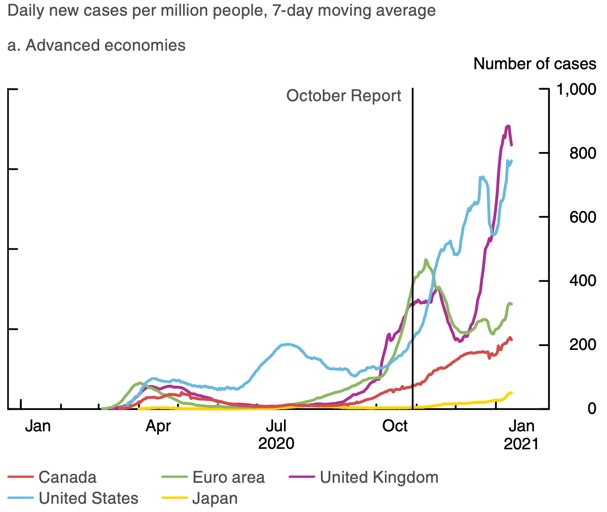

Despite a negative forecast for Q1 GDP growth, Bank of Canada Governor Tiff Macklem revealed an upgrade for 2021 and 2022 GDP growth: 4% and 5% respectively. The Bank of Canada sees beyond the current lockdown-driven slowdown to a coronavirus vaccine launch that puts Canada 6 months ahead of schedule on its road to protecting its citizens. Overall, Canada has managed the pandemic much better than the U.S. The case rates alone can help explain the relative strength for the Canadian dollar using USD/CAD. Currently, Canada's approximate 200 coronavirus cases per million people is a mere quarter of the soaring case rate in the U.S.

Still, the Bank of Canada remains very cautious. Surely the desire to keep monetary policy highly accommodative clamps down on enthusiasm.

“…there is clear reason to be more optimistic about the direction of the economy over medium term. But we are not there yet. The resurgence in COVID-19 cases weighs heavily on the near-term economic outlook. And this underlines the ongoing need for extraordinary fiscal and monetary policies.”

The strength of the Canadian dollar is also a drag on the outlook. However, Macklem acknowledged the Bank of Canada can do little about the relative strength. He pointed to a general sell-off in the U.S. dollar as a key driver. From the very end of the Monetary Policy Report:

“The Canadian dollar has risen steadily since October, reaching its highest level since early 2018. This increase has been driven primarily by broadbased weakness of the US dollar. Appreciation of the Canadian dollar creates direct downward pressure on inflation by lowering the prices of imports. Further appreciation of the Canadian dollar could slow output growth by reducing the competitiveness of Canadian exports and import competing production. Slower output growth would also imply more disinflationary pressures.”

The "broadbased" weakness is intertwined with the soaring COVID-19 cases as the U.S. is forced to continue taking extraordinary fiscal and monetary measures to ameliorate the economic pain from a pandemic raging out of control.

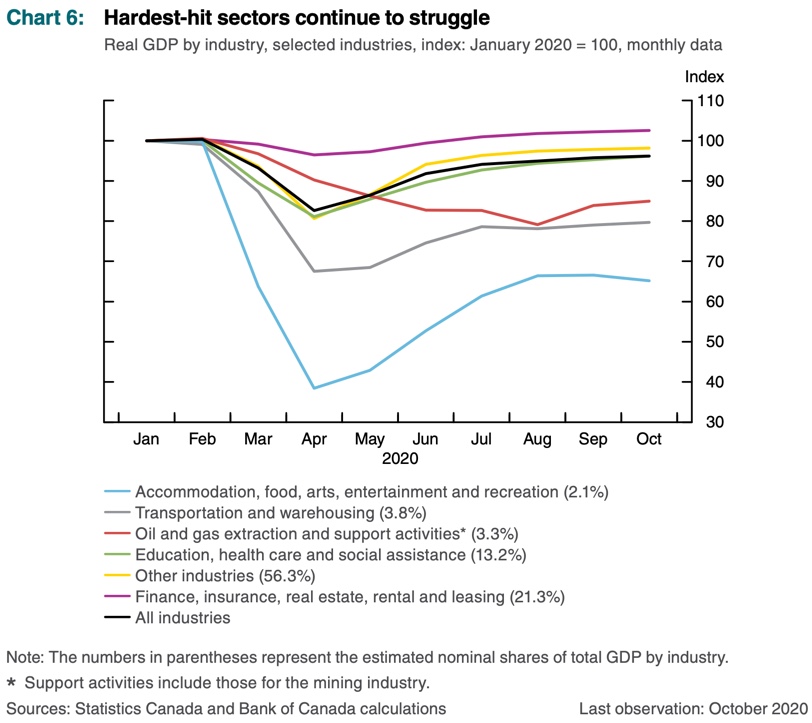

In Canada, as in so many advanced economies, the pain of economic hardship is felt heaviest by service sectors relying on direct contact with customers or serving large gatherings of people. The chart below shows how three Canadian sectors are already back to or close to pre-pandemic levels of economic activity. The biggest laggard is the "accommodation, food, arts, entertainment and recreation" sector. This sector is only back to 65% of its previous level of economic activity. Fortunately, this sector is a very small part of Canada's GDP at 2.1%. So, overall, Canada is almost back to pre-pandemic GDP.

The Trade on the Canadian Dollar

Since hitting a 4-year high at the bottom of last March’s stock market crash, USD/CAD moved along a downward trend. The first chart above shows how the 20-day moving average (DMA) serves as a pivot for this downtrend. The trend is the friend in this case and supports the bullishness I have maintained in the Canadian dollar throughout the pandemic. Canada’s approach to managing COVID-19 risks gave it a GDP advantage over the U.S. starting last summer. For my next trade, I faded the bounce that unfolded after the initial excitement from the Monetary Policy Report waned and completely reversed.

U.S. President Biden is a wildcard for the trade on the Canadian dollar. If Biden’s plans for aggressive fiscal policy and massive deficit spending turbocharge growth in the US., economic strength could (should) eventually bottom out the U.S. dollar. However, the forex market is likely not yet willing to bet on these prospects.

Be careful out there!