This article is the first part of a two-part article. Due to its length and importance, we split it to help readers’ better digest the information. The purpose of the article is to define money and currency and discuss their differences and risks. It is with this knowledge that we can better appreciate the path that massive deficits and monetary tomfoolery are putting us on and what we can do to protect ourselves.

How often do you think about what the dollar bills in your wallet or the pixel dollar signs in your bank account are? The correct definitions of currency and money are crucial to our understanding of an economy, investing and just as importantly, the social fabric of a nation. It’s time we tackle the differences between currency and money and within that conversation break the news to you that deficits do matter, TRUST me

At a basic level, currency can be anything that is broadly accepted as a medium of exchange that comes in standardized units. In current times, fiat currency is the currency of choice worldwide. Fiat currency is paper notes, coins, and digital 0s and 1s that are governed and regulated by central banks and/or governments. Note, we did not use the word guaranteed to describe the role of the central bank or government. The value and worth of a fiat currency rest solely on the TRUST of the receiver of the currency that it will retain its value and the TRUST that others will accept it in the future in exchange for goods and services.

Whether its yen, euros, wampum, bitcoin, dollars or any other currency, as long as society is accepting of such a unit of exchange, trade will occur. When TRUST in the value of a currency wanes, commerce becomes difficult, and the monetary and social prosperity of a nation falters. The history books overflow with such examples.

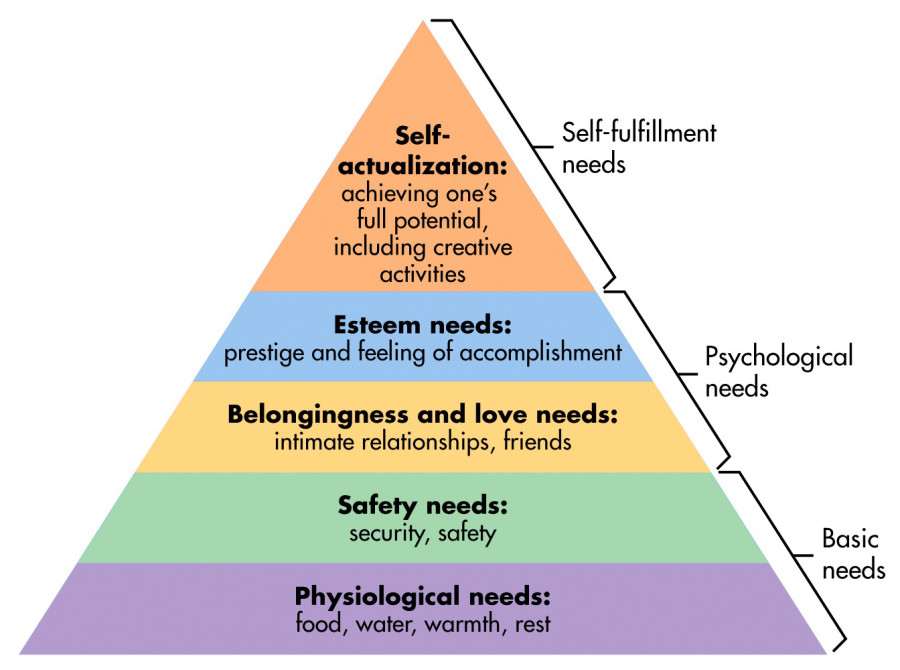

Maslow and Currency

Before diving into the value of a currency, it is worth considering the role it plays in society and how essential it is to our physical and mental well-being. This point is rarely appreciated, especially by those that push policies that debase the currency.

Maslow created his famous pyramid to depict what he deemed the hierarchy of human needs. The levels of his pyramid, shown below, represent the ordering of physiological and psychological needs that help describe human motivations. When these needs are met, humans thrive.

Humans move up the pyramid by addressing their basic, lowest level needs. The core needs, representing the base, are physiological needs including food, water, warmth and rest. Once these basic needs are met, one then seeks to attain security and safety. Without meeting these basic physiological and safety needs, our psychological and self-fulfillment needs, which are higher up the pyramid, are difficult to come by. Further, as we see in some third-world countries, the social fabric of the nation is torn to shreds when a large part of the population cannot satisfy their basic needs.

In modern society, except for a few who live “off-the-grid,” fiat currency is the only means of attaining these necessities. Possession of currency is a must if we are to survive and thrive. Take a look back to the opening paragraphs and let’s rephrase that last sentence: possession and TRUST of currency is a must if we are to survive and thrive.

It is this most foundational understanding of currency that keeps our economy humming, our physical prosperity growing and our society stable. The TRUST backing the dollar, euro, yen, etc. is essential to our financial, physical and psychological welfare.

Let’s explore why we should not assume that TRUST is a permanent condition.

Deficits Don’t Matter…. or Do They?

Having made the imperative connection between currency and TRUST and its linkage to trade and commerce along with our physical and mental well-being, we need to explore the current state of the United States government debt burden, monetary policy, and the growing belief that deficits don’t matter.

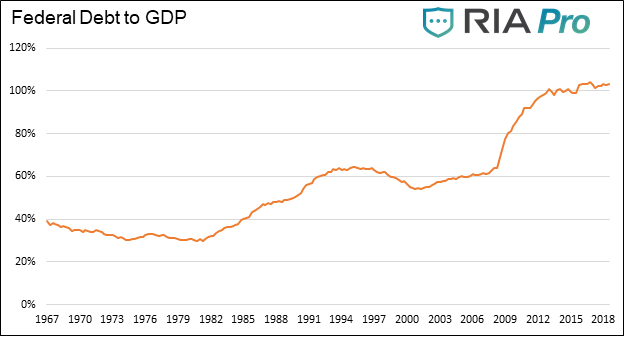

Treasury debt never matures, it is rolled over. Yes, a holder of a maturing Treasury bond is paid in full at maturity, however, to secure the funds to pay that holder, the government issues new debt by borrowing money from someone else. Over time, this scheme has allowed deficits to expand, swelling the amount of debt outstanding. Think of this arrangement as taking out a new credit card every month to pay off the old card.

The chart below shows U.S. government debt as a percentage of GDP. Since 1967 government debt has grown annually 2% more than GDP.

Data Courtesy: St. Louis Federal Reserve

Continually adding debt at a faster rate than economic growth (as shown above) is limited. To extend the ability to do this requires declining interest rates, inflation and a little bit of financial wizardry to make debt disappear. Fortunately, the U.S. government has a partner in crime, the Federal Reserve.

As you read about the Fed’s methods to help fund deficits, it is important to consider the actions they routinely take are at the expense of the value of the currency. This warrants repeating since the value of the currency is what supports TRUST in the currency and allows it to retain its functional purposes.

The Fed helps the government consistently run deficits and increase their debt load in three ways.

- The Fed stokes moderate inflation.

- The Fed manages interest rates lower than they should be.

- The Fed buys Treasury and mortgage securities (open market operations/QE) and, as we are now witnessing, monetizes the debt.

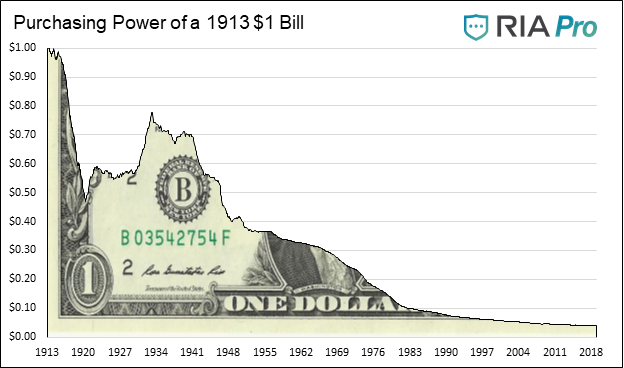

Inflation

Within the Fed’s charter, Congress has mandated the Fed promote stable prices. To you and me, stable prices would likely mean no inflation or deflation. Regardless of what you and I think, the Fed interprets the mandate as an annual 2% rate of inflation. Since the Fed was founded in 1913, the rate of inflation has averaged 3.11% annually. That rate may seem inconsequential, but it adds up. The chart below illustrates how the low but consistent rate of inflation has debased the purchasing power of the dollar.

Data Courtesy: St. Louis Federal Reserve

$1 borrowed in 1913 can essentially be paid off with .03 cents today. Inflation has certainly benefited debtors.

Interest Rate Management

For the better part of the last decade, the Fed has imposed price controls that kept interest rates below what should be considered normal. Normal, in a free market economy, is an interest rate that compensates a lender for credit risk and inflation. Since Treasury debt is considered “risk-free,” the predominant risk to Treasury investors is earning less than the rate of inflation. As far as “risk-free”, read our article: The Mind-Blowing Concept of Risk-Free’ier.

If the yield on the bond is less than inflation, as has recently been the case, the purchasing power and wealth of the investor declines in the future.

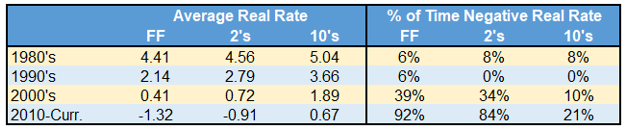

The table below highlights how U.S. Treasury real rates (yields less CPI) have trended lower over the past forty years. In fact, over the last decade, negative real rates are the norm, not the exception. When investors are not properly compensated by the U.S. Treasury, the onus of government debt is partially being put upon investors. We have the Fed to thank for their Fed Funds (FF) policy of negative real rates.

Data Courtesy: St. Louis Federal Reserve

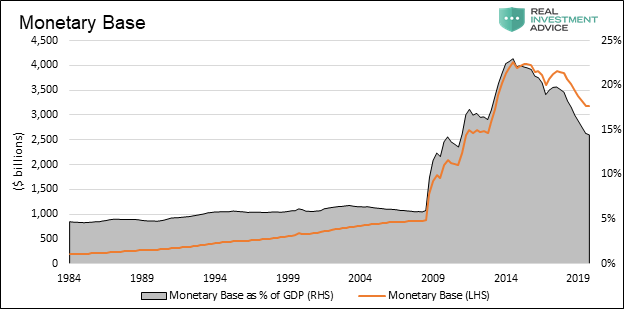

Fed Balance Sheet

The Fed uses its balance sheet to buy and sell U.S. Treasury securities to manage the money supply and thus enforce their interest rate stance. In 2008, their use of the balance sheet changed. From 2008 through 2013, the Fed purchased nearly $4 trillion of Treasury and mortgage-backed securities in what is called Quantitative Easing (QE). By reducing the supply of these securities, they freed up liquidity to move to other assets within the capital markets. The action propped up asset prices and helped keep interest rates lower than they otherwise would have been.

Since 2018, they have reversed these actions by reducing the size of their balance sheet in what is called Quantitative Tightening (QT). This reversal of prior action essentially makes the benefits of QE temporary. However, if they fail to reduce it back to levels that existed before QE was initiated, then the Fed permanently monetized government debt. In plain English, they printed money to extinguish debt.

As we write this article, the Fed is in the process of ending QT. Based on the Fed schedule as announced on March 20, 2019, the balance sheet will permanently end up $2.28 trillion larger than from when QE was initiated. To put that in context, the balance will have grown 269% since 2008, as compared to 48% economic growth.

Data Courtesy St. Louis Fed

The methods the Fed employs to manage policy as described above, all involve using their balance sheet to alter the money supply and help the Treasury manage its deficits. We can argue the merits of such a policy, but we cannot argue a basic economics law; when there is more of something, it is worthless. When something of value is created out of thin air, its value declines.

At what point is debt too onerous, deficits too large and the Fed too aggressive such that TRUST is harmed? No one knows the answer to that question, but given the importance of TRUST in a fiat currency regime, it would be wise to avoid actions that could raise doubt. Contrary to that guidance, current fiscal and monetary policy throws all TRUST to the wind.

Prelude to Part 2

As deficits grow and government debt becomes more onerous, the amount of Fed intervention must become greater. To combat this growing problem, both political parties are downplaying deficits and pushing the Fed to do more. In part 2 we will explore emerging fiscal mindsets and what they might portend. We will then define money, and with this definition, show why the difference between currency and money is so important.

Comments

Log in or sign up to join the conversation.