FX Positioning: First (Timid) Signs Of USD Short-Squeeze

CFTC data on speculative positions shows some signs of dollar shorts being unwound as GBP, JPY, AUD, and NZD all saw their net positioning drop in the week ending 26 January. That said, EUR/USD still shows no evidence of a correction in its overstretched net long positions.

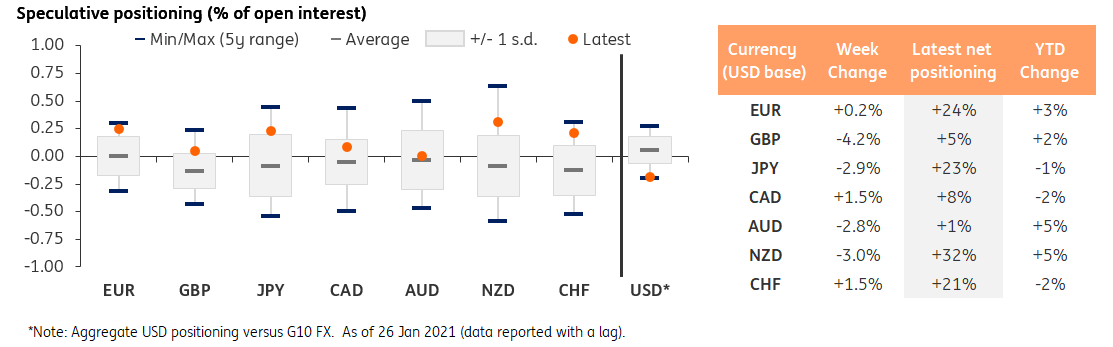

USD positioning starting to recover

After hitting a record low at -19.2% of open interest, the USD aggregate positioning versus reported G10 (i.e. G9 excluding Norway's krone and Sweden's krona) slightly rebounded in the week 20-26 January, moving to 18.3% of open interest. We have been highlighting over the past few weeks how CFTC positioning data has been more and more disconnected from actual market dynamics as dollar shorts increased despite the greenback’s rebound in spot.

Source: CFTC, Macrobond, ING

We were expecting to see some kind of short squeeze in the dollar, so the dynamics shown in the week ending 26 January are not surprising. That said, the divergence with market dynamics persists. And not only because the dollar’s recovery in positioning has been rather marginal, but also because the currencies that showed the largest positioning contraction were the British pound and New Zealand dollar which have been the best G10 performing currencies (among those reported by CFTC) in the last month (both gained vs USD) and both rallied in the week 20-26 January.

It’s been often the case over the past year that positioning data published by CFTC showed some lag to the actual market movements, so we could still see some realignment with the market in the coming reports. For now, it is important to highlight how the picture provided by CFTC data is probably not a highly reliable indicator of market sentiment on G10 currencies. After all, it must be remembered that the report summarises the positions of a rather small segment of the market - mainly short-term speculators - and this may result in such divergences with actual market dynamics.

EUR remains stable, sterling long squeeze is hard to explain

EUR/USD positioning continued to show no sign of correction and remained at 24% of open interest in the week ending 26 January. Any tangible indication that some short squeeze has happened in the dollar will likely have to be mirrored in the EUR/USD gauge, which incidentally makes up 50% of the USD aggregate positioning.

Sterling’s wide drop in net positioning appears hard to justify. A combination of the unwinding of negative rate expectations and encouraging advancements on the vaccination front in the UK have contributed to keeping GBP supported of late in spite of the USD recovery. One currency we were not expecting to experience a long squeeze was indeed GBP: especially because its net-long positioning was rather contained (at 9% of o.i. last week, now at 5%) compared to other overbought currencies such as the euro. Regardless of the recent move in positioning (we are inclined to think the overall market sentiment on GBP is more on the bullish side than shown in the positioning data), the relatively bright vaccination prospects in the UK may keep supporting GBP and we expect to see a build-up in GBP longs in the coming weeks and months.

JPY hit by Treasury sell-off, AUD-NZD divergence remains too wide

Looking at the rest of G10, the yen saw a contraction of 2.9% of open interest in its net positioning, which actually looks fairly in line with recent market dynamics. Despite global risk appetite easing of late, rising safe-haven bets have mostly been channeled through the dollar and left the generally risk-averse JPY without a solid floor. The yen's correlation with US yields, which rose considerably in January, contributed to making the yen a rather unattractive option. The yen ultra-long positioning may have played a role too, and the short squeeze shown in the last CFTC report may be a testament to this.

Looking at the commodity currencies, the Canadian dollar continued to advance into a net long territory and is beginning to have a positioning profile that is more in line with its spot level. The Australian and New Zealand dollars moved in tandem as they both saw their net-positioning drop by around 3% of o.i. in the week under consideration. Still, while NZD was starting from a very high level of net longs (and has remained the most overbought G10 currency), AUD's tiny net long positioning was, in our view, already underestimating the actual bullish sentiment on the currency. Despite NZD having experienced better momentum than AUD over the past weeks, the divergence between the two currencies remains too wide to consider AUD’s neutral positioning to be indicative of the actual market sentiment on the currency.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more