EUR And ECB: Not Rocking The Boat

The ECB did not surprise today but the glimmers of positive news on the economic outlook were a marginal EUR positive. While the language on FX was somewhat stronger than in Dec (ECB is ‘’very attentive’’), the reduced downside risk to the economy and EUR being below its 6-month average doesn't suggest imminent action. We expect more EUR/USD gains this year.

Modestly more hawkish vs expectations

As expected, the ECB did not deliver a meaningful surprise today (see ECB Review). One can argue that the bias of the statement and of the press conference was towards a hawkish side (vs expectations) as (a) the ECB judged that the downside risks to the economic outlook are less pronounced, and (b) the ECB acknowledged it may not have to spend the entire Pandemic Emergency Purchase Programme (which it topped up by EUR 500bn last month).

Attentive to the exchange rate...

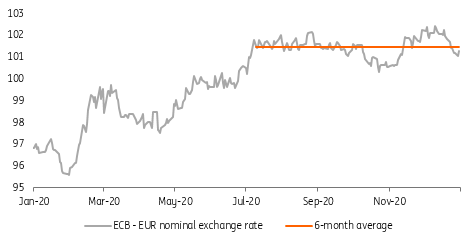

The main focus was on the comments on the currency. President Lagarde reiterated the previous sentence that the central bank monitors the exchange rate ‘’very carefully.’’ However, she also added that the central bank is ‘’very attentive’’ to FX developments. The language with respect to FX is thus somewhat stronger than the last time, but given the ECB's assessment of the economic outlook (''downside risks less pronounced''), President Lagarde's focus on positives during the press conference (Brexit deal, vaccination,...) as well as the fact that the trade-weighted euro is below its 6-month average, all suggests that the FX market should take the exchange rate comments with a pinch of the salt and the impact on the euro should be very muted. We thus see the overall muted, yet modestly postive reaction of the EUR/USD to the press conference as fully justified.

The trade-weighted euro does not show signs of excessive strength

(Click on image to enlarge)

Source: ING, Refinitiv

... but no imminent ECB action is likely or justified

While we don’t rule out further verbal interventions or even a policy reaction in response to currency strength, for this to happen the euro would have to strengthen sharply and meaningfully first. At this point, this is not the case, with the trade-weighted euro being currently at the level where it was when the ECB official embarked on the verbal intervention last summer. Hence, there is no imminent need for the ECB to react at this point.

More upside to the euro ahead

Looking ahead, we expect further gains in EUR/USD and target 1.30 by the year-end. While the idiosyncratic euro story remains unexciting (the eurozone will not outperform the US economy this year and any ECB policy normalization is a very distant story), we expect the bearish dollar dynamics to dominate as the USD will suffer from the mix of negative rates, a non-reacting Fed to rising inflation and the global economic recovery. Under these conditions, the dollar should remain on a broad-based decline, and in turn push EUR/USD higher.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more