Image Source: Pixabay

Asian markets experienced gains ahead of trade negotiations between China and the US on Monday, which could help ease the tensions between the two largest economies globally. Asia’s regional stock index rose by 0.9% prior to the London discussions, supported by a rise in technology stocks linked to Meta Platforms Inc.’s investment strategies. Shares from China listed in Hong Kong surged by 1.1%, positioning them to enter a bull market - a term used when there’s a 20% rise from a recent low. A significant index for emerging market stocks increased by 0.7%, on track for its highest close since February 2022. The dollar fell in comparison to all its Group-of-10 counterparts. Yields on 10-year Treasury notes decreased by about 2 basis points to 4.49%, following a spike on Friday. Trade tensions between President Donald Trump and China’s Xi Jinping seemed to lessen as a deadlock over essential minerals was resolved, allowing for more trade discussions. Contributing to the stock market’s positive sentiment was a surprising jobs report released on Friday, which alleviated concerns regarding a recession in the largest global economy. US payrolls added 139k jobs in May, exceeding the 125k forecast, but the report is far from robust. Revisions to March and April cut 95k jobs, marking consistent downward adjustments this year. Job creation is at 70% of last year’s pace, already below the non-recession average. Growth is skewed, with healthcare accounting for 69% of new jobs despite being 14.6% of total employment, while other sectors remain stagnant. Most new roles are in lower-paying sectors like leisure, hospitality, and retail. The data likely overstates labor market strength amid business uncertainties, declining ADP figures, rising jobless claims, and soft surveys. This poses challenges for the Fed, balancing inflation risks and fiscal concerns.

Overnight markets were also attentive to developments in Los Angeles, where National Guard soldiers are confronting protesters who are demonstrating against Trump's immigration policies. Footage revealed a portion of a major freeway in the city was obstructed by activists. California, on its own, ranks as the world's fourth-largest economy, surpassing Japan's gross domestic product, and Trump dispatched guardsmen to its largest city to address what the White House referred to as "chaos, violence, and lawlessness." Governor Gavin Newsom described Trump's response as "the actions of a dictator."

Key economic indicators to watch this week include the US May CPI, alongside inflation and trade data from China. In Europe, the UK will release its monthly GDP for April. In the US, the Federal Reserve's quiet period ahead of the June 18 meeting has begun. The May CPI report due Wednesday will be a focal point as investors assess the effects of tariff policies on prices and the Federal Reserve's interest rate trajectory. Economists anticipate month-on-month (MoM) headline inflation to remain at +0.2%, with core inflation expected to edge up by just +0.03%, down from +0.2% in April. On Thursday, the Producer Price Index (PPI) is forecasted to show a +0.2% increase for the headline measure, following a -0.5% decline in April. Friday will bring the preliminary University of Michigan survey for June, which will provide insights into consumer sentiment and inflation expectations. Economists project the sentiment index to recover to 55.0, up from 52.2 in May. In Europe, the UK will release key data, including labor market statistics on Tuesday and the monthly GDP figure for April on Thursday. Additionally, Chancellor Reeves will deliver the Spending Review on Wednesday. Across the region, noteworthy releases include Italy's trade balance and industrial production data for April, as well as May CPI figures from Denmark and Norway. Several European Central Bank (ECB) speakers are also scheduled to provide updates throughout the week. Japan will see key data releases this week, starting with the Economy Watchers Survey for May on Monday, followed by the Producer Price Index (PPI) on Wednesday.

Overnight Headlines

- China CPI Slumps Again, Deepening Deflation Worries

- Japan GDP Revised Contraction Confirms BoJ Caution

- ECB Has Maximum Flexibility On Interest Rates, Nagel Tells DLF

- ECB Is 'Nearly Done' With Cuts If Forecasts Hold, Vujcic Says

- US Seeks Rare Earth Deal With China At London Talks

- Trump Warns Musk Of ‘Consequences’ If He Backs Democrats

- Trump’s Golden Dome Pits Silicon Valley Against Defence Giants

- US Money Market Inflows Surge On Tariff-Driven Caution

- Russia Advances Into East-Central Ukraine As Tensions Escalate

- UK PM Starmer Urges Nvidia’s Huang To Train AI Talent In Britain

- BlackRock, Vanguard Face High-Stakes Collusion Case In Texas

- OpenAI’s Eyeball-Scanning Digital ID Project To Launch In UK

- EU Urged To Soften Supply Chain Law As Industry Pushes Back

- OPEC+ Quota Hikes Yet To Deliver Oil Surge, Morgan Stanley Says

- China’s Central Bank Buys Gold For 7th Consecutive Month

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- Significant EUR/USD strikes for Monday, June 9, include 1.1300 and 1.1350, each with nearly 1 billion euros, 1.1425 with 2.4 billion euros, 1.1500 with 1.7 billion euros, and 1.1600 with 2.7 billion euros. On Tuesday, strikes between 1.1400-25 total 3.5 billion euros. Wednesday sees 1.1300 at 3 billion euros, 1.1400 at 2.5 billion euros, and 1.1500 at 2.1 billion euros. Thursday has strikes at 1.1300 with 1.4 billion euros, 1.1350 with 2 billion euros, 1.1400 with 2.9 billion euros, 1.1450 with 2.6 billion euros, and 1.1600 with 1.7 billion euros. On Friday, June 13, strikes at 1.1400 and 1.1500 are each valued at 1.3 billion euros.

- For GBP/USD, the largest strikes expire on Monday, June 9, at 1.3650 with 350 million pounds, Wednesday at 1.3450 with 676 million pounds, and 1.3600-05 at 650 million pounds, while Friday has 1.3400 at 620 million pounds. The EUR/GBP strikes are on Monday at 0.8440-50 with 650 million euros, on Thursday at 0.8350 with 500 million euros, and between 0.8480-0.8500 with 650 million euros, and on Friday at 0.8475 with 775 million euros.

- Noteworthy EUR/CHF expiries occur on Thursday, June 12, at 0.9375 with 650 million euros.

- The largest AUD/USD strikes next week are on Monday, June 9, at 0.6500-10 with A$770 million, Tuesday at 0.6420 with A$941 million, and 0.6460 with A$600 million. Wednesday sees 0.6495-0.6500 with A$800 million, and Thursday includes strikes between 0.6475-0.6500 with A$2.4 billion, and 0.6600 at A$800 million.

- Significant USD/CAD strikes expire on Tuesday, June 10, at 1.3695 with $777 million, Wednesday at 1.3760 with $750 million and 1.3800 with $650 million, and Thursday at 1.3750 with $700 million.

- The largest USD/JPY strike expiries next week fall on Monday between 143.55-65 with $1 billion and 144.00 with $900 million, Tuesday at 143.90-144.00 with $1 billion, Wednesday at 143.00 and 144.30 with nearly $1 billion each, and Thursday at 143.00 with $1.6 billion, between 143.30-55 with $2 billion, and 143.85-144.00 with $1.2 billion.

CFTC Data As Of 6/6/25

- Speculators have increased their net short position in CBOT US Treasury bonds futures by 48,483 contracts, bringing the total to 102,373. They also reduced their net short position in CBOT US Ultrabond Treasury futures by 5,029 contracts, now totaling 228,443. Additionally, there was a decrease of 64,348 contracts in the net short position for CBOT US 10-year Treasury futures, which now stands at 705,256 contracts. On the other hand, the net short position for CBOT US 5-year Treasury futures increased by 63,299 contracts to reach 2,396,536. The net short position for CBOT US 2-year Treasury futures also grew, rising by 24,022 contracts to 1,143,925.

- Equity fund managers have cut their net long position in the S&P 500 CME by 40,048 contracts, resulting in a total of 814,481 contracts. Conversely, equity fund speculators have raised their net short position on the S&P 500 CME by 27,860 contracts, now at 285,326.

- The net long position for the Japanese yen is at 151,149 contracts, while the euro has a net long position of 82,764 contracts, and the British pound holds a net long position of 35,215 contracts. The Swiss franc is currently at a net short position of -26,066 contracts, and Bitcoin has a net short position of -2,312 contracts.

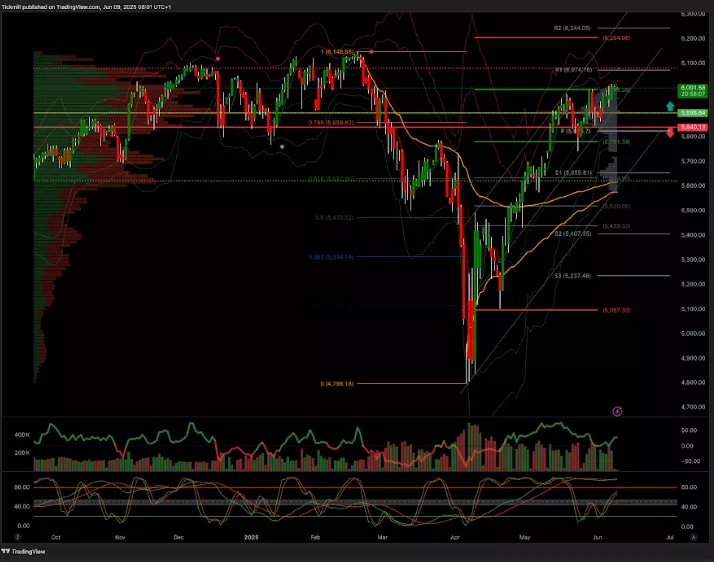

Technical & Trade Views

SP500 Pivot 5900

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 5900 target 6100

- Below 5800 target 5650

(Click on image to enlarge)

EURUSD Pivot 1.12

- Daily VWAP bearish

- Weekly VWAP bullish

- Above 1.11 target 1.19

- Below 1.11 target 1.0950

(Click on image to enlarge)

GBPUSD Pivot 1.34

- Daily VWAP bearish

- Weekly VWAP bullish

- Above 1.34 target 1.38

- Below 1.3350 target 1.32

(Click on image to enlarge)

USDJPY Pivot 147

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 147.10 target 148.26

- Below 146.53 target 139

(Click on image to enlarge)

XAUUSD Pivot 3365

- Daily VWAP bearish

- Weekly VWAP bullish

- Above 3410 target 3600

- Below 3240 target 3000

(Click on image to enlarge)

BTCUSD Pivot 105k

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 105k target 118k

- Below 103k target 100k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Friday, June 6

Daily Market Outlook - Friday, June 6

The FTSE Finish Line - Thursday, June 5

Comments

Log in or sign up to join the conversation.