Image Source: Pixabay

Asian equities experienced mixed performance to close out the week, as a result of tepid earnings Stateside and lingering concerns over US regional banks, with several names hitting circuit breakers during US trading. The subdued performance in the United States, coupled with disappointing initial jobless claims, contributed to overall negative risk sentiment. The Nikkei 225 outperformed, reaching its highest level since November 2021. The advance was primarily driven by positive earnings results, particularly from prominent domestic blue-chip stocks. The Hang Seng and Shanghai Composite displayed uncertainty, influenced by a range of factors. From a positive perspective, talks between US National Security Adviser Sullivan and China's top diplomat Wang Yi hinted at a potential call between President Biden and President Xi. However, investors were less impressed by weaker-than-anticipated Chinese loans and financing data. The scheduled meeting between President Biden and congressional leaders has been delayed until next week, House Leader McCarthy was keen to state that the delay doesn't mean that debt talks are in peril.

This morning investors will shift their attention to a series of economic releases from Europe, after British gross domestic product (GDP) data once again managed to sidestep technical recession by printing meager economic progress with a 0.1% quarterly gain, however, the year-over-year number came in just shy of the expected 0.4% at 0.3%. The pound experienced a significant decline on Thursday following the Bank of England's decision to raise interest rates and maintain the possibility of further monetary tightening, investors will eye comments later from BoE’s Pill to add color regarding the future glide path for UK rates especially in light of the BoE’s acceptance around forecasting missteps. Additionally, inflation reports from France and Spain will be on the slate this morning, shedding light on the effects of European tightening measures on regional prices. These reports will offer additional insight into the impact of monetary policies in local regions.

Stateside a somewhat quieter end to what has been a fairly data-intensive week, with US export/import prices and the first look at the University of Michigan sentiment. Treasury Secretary will be on the wires again this morning as she makes remarks ahead of the G7 finance ministers meeting, expect further doomsday rhetoric around any notion of the US failing to raise the US debt ceiling and consequently defaulting on US debt, however, the background mood music appears to be showing improving open lines of communication between congressional parties.

FX Options Expiries For 10 am New York Cut

(In bold represent larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0835 (280M), 1.0920-25 (439M), 1.0950 (300M), 1.0975 (410M)

- 1.1020-30 (1.2BLN), 1.1050 (696M)

- USD/CHF: 0.8850-60 (310M), 0.8945-50 (267M)

- GBP/USD: 1.2400 (285M), 1.2600 (292M)

- EUR/GBP: 0.8725 (300M), 0.8740 (200M), 0.8845-50 (267M)

- AUD/USD: 0.6700 (290M), 0.6740 (444M)

- USD/CAD: 1.3465 (374M), 1.3500-05 (1.1BLN)

- USD/JPY: 134.00 (341M), 134.20 (515M), 134.50 (562M), 135.00 (1.3BLN)

CFTC Data As Of 02/05/2023

- USD spec net short cut in Apr 26-May 2 period, $IDX +0.11%

- EUR$ +0.36% in period, specs +4,089 contract now +173,489 ahead of ECB hike

- $JPY +1.98%, specs +420 contract, now -68,324; Fed rate path uncertain

- GBP$ +0.43%, specs -4,774 contracts now +1,065, sellers into strength

- AUD$ +0.54% spec short grows by 5,548; $CAD 0.04% spec short grows to 50,096

- AUD, CAD under pressure amid global growth concerns, oil hit hard in period

- BTC +2.56% in period flips to positive as specs buy 461 contracts on dip early in period (Source RTRS)

Overnight News of Note

- US Pres Biden Meeting W/ Congress Leaders On Debt Limit Postponed

- ECB’s Push To Raise Borrowing Costs Runs Up Against Wall Of Cash

- EU Says China Will Take Advantage Of Russian Defeat In Ukraine - FT

- China Inflation Seen Rebounding In H2 - Shanghai Securities News

- NZ 2-Year Inflation Expectations Ease To Within RBNZ Target Band

- NZ'S Robertson: Now Is Not The Time For Inflationary Tax Cuts

- Fitch Ratings: Economic Backdrop Remains Supportive For APAC Banks

- China's Yuan Weakens Past Key Threshold To 2-Month Low

- Hong Kong Dollar’s Hibors Fall Across Curve As Liquidity Eases

- Bitcoin Dips to Lowest Since March After Falling for Second Day

- Oil Holds Two-Day Drop As Demand Concerns Offset SPR Refill Plan

- Japan Stocks, China Tech Bolster Subdued Risk Mood Friday

- Apple To Open First Online Shop In Vietnam In A Push To EM

- SocGen Debt Traders Beat Peers In First Quarter As Profit Gains

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

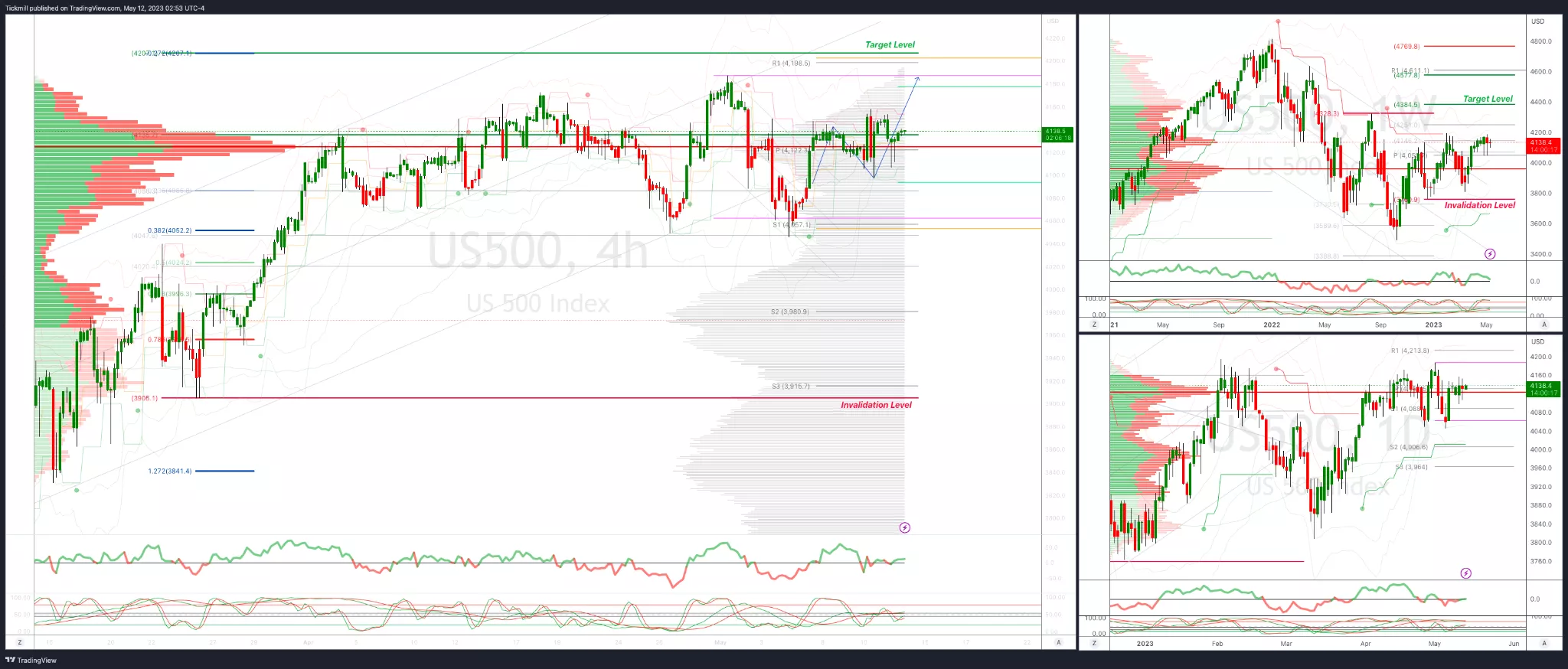

SP500 Bias: Intraday Bullish Above Bearish Below 4100

- Below 4090 opens 4040

- Primary support is 4000

- Primary objective is 4207

- 20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

EURUSD Bias: Intraday Bullish Above Bearish below 1.09

- Below 1.09 opens 1.08

- Primary support is 1.07

- Primary objective is 1.1128

- 20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

_638194742532976740.webp)

GBPUSD Bias: Intraday Bullish Above Bearish below 1.25

- Below 1.2475 opens 1.24

- Primary support is 1.2350

- Primary objective 1.2750

- 20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

_638194742883369361.webp)

USDJPY Bias: Intraday Bullish above Bearish Below 134

- Below 133.90 opens 133

- Primary support is 133

- Primary objective is 138.80

- 20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

_638194743261649751.webp)

AUDUSD Bias: Intraday Bullish Above Bearish below .6720

- Below .6710 opens .6670

- Primary support is .6640

- Primary objective is .6826

- 20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

_638194743604690074.webp)

BTCUSD Intraday Bias: Bullish Above Bearish below 29300

- Primary resistance 30000

- Primary objective is 26000

- Below 26000 opens 25800

- 20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

_638194743929755319.webp)

More By This Author:

FTSE 100: Pressured As ECB Follows Fed’s Lead, BoE EyedDaily Market Outlook - Thursday, May 11

FTSE 100: Struggling For Upside Traction As U.S. Inflation Ticks Lower

Comments

Log in or sign up to join the conversation.