Avalon: A Colossal Partnership

Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble. - Warren Buffett

As Buffett said it best, stellar growth companies do not come often. In my years of daily exploration of the bioscience space, I recently encountered a rare investment prospect and you should not miss out. The investment gem is Avalon Globocare (AVCO), a young innovator of the next-generation chimeric antigen receptor - T cell therapy (i.e. CAR-T). Back in 2017, I was quite excited at the CAR-T prospects of Kite Pharma and Juno Therapeutics. And, I am thrilled as Kite and Juno were correspondingly acquired by Gilead Sciences (GILD) and Novartis (NVS) for $11.9B and $9B.

Since cellular therapy evolves at a rapid pace, I now vote my strongest confidence in Avalon's CAR-T. Nonetheless, I'm not the only one who is optimistic about Avalon's precision medicine and diagnostics. For instance, the company recently inked a mega partnership with GE Healthcare (GE). In this research, I'll present a fundamental analysis of Avalon while focusing on the latest partnership development.

Figure 1: Avalon stock chart (Source: StockCharts)

About The Company

As usual, I'll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in Freehold New Jersey, Avalon Globocare is a CellTech company that operates Avactis Biosciences and Genexosome Technologies subsidiaries. Founded in 2016, Avalon is already forging its crown as a leading cell-based technology innovator.

Figure 2: Avalon subsidiary (Source: Avalon)

In the Golden Age of CAR-T, Avalon is focused on the development and commercialization of disruptive medicines and diagnostics to serve the strong unmet needs in cancer and other diseases. Using a trident-like approach of Poseidon, the company captures opportunities in three highly promising niches. They include exosomes diagnostics, regenerative medicine, and cellular immunotherapy. I elucidated in the prior research,

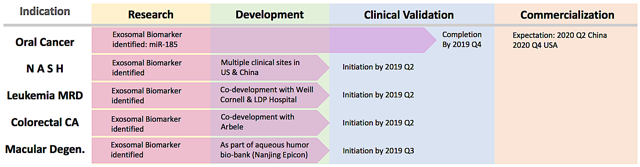

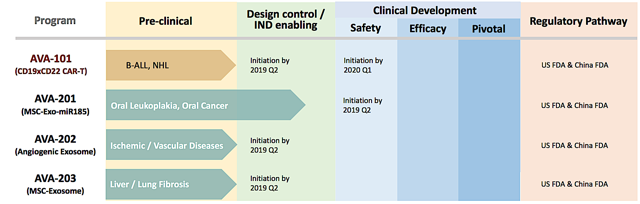

Powering the diagnostic portfolio is precision medicine based on "exosomal biomarkers." Accordingly, Avalon is delivering a diagnostic avalanche against oral cancer, nonalcoholic steatohepatitis ("NASH"), leukemia, colorectal cancer, and macular degeneration. Notably, exosomal biomarkers can quickly pinpoint a diagnosis to give physicians an edge against dreaded diseases. In the battle of life and death, I believe that accuracy and precision are of paramount importance. That aside, Avalon is brewing various potential blockbusters, including AVA-101, -201, and -203 as depicted below.

Figure 3: Diagnostic and therapeutic pipeline (Source: Avalon)

Pipeline Advancement

On June 22, 2019, Avalon announced a highly strategic partnership with GE Healthcare. Under the collaboration, the companies will work together to improve the logistics such as automation and standardization for good manufacturing practice ("GMP"). As a result, this will galvanize Avalon's global cell production capabilities and thereby positioned it to become an undisputed leader in cell-based medicine.

Figure 4: GE solution (Source: Aithority)

As a subsidiary of General Electric, GE Healthcare provides logistic solutions to healthcare providers and innovators. Their service and product facilitate research and development of advanced therapies and vaccines. As such, GE improves the outcomes for healthcare providers, innovators, and most importantly patients.

Figure 5: GE Healthcare (Source: Glassdoor)

With the aforesaid deal, Avalon strategically leverages GE's FlexFactory Cell Therapy platform and FastTrak process development/training services. Moreover, the company has access to GE's standard operating protocol and protocol library for therapeutic development. Furthermore, users can obtain training at GE sites and Avalon's Nanjing Epicon facility. Enthused by the partnership, the GE Global Commercial Enterprise Solution Leader (Angela Chen) remarked,

Cellular medicines as a bio-industry sector have been growing and evolving at a rapid pace during recent years with vast potential to change the way various diseases are managed. GE continues investing in technologies and services aimed at the thriving cellular medicine industry with a firm commitment to making these promising cellular therapeutic modalities accessible through successful industrialization. We are pleased to work with Avalon GloboCare, a global leader in cell-based therapeutics and exosome technology, who share our mission and vision for advancing innovation and delivering automation, standardization, and bio-production solutions for cellular medicines.

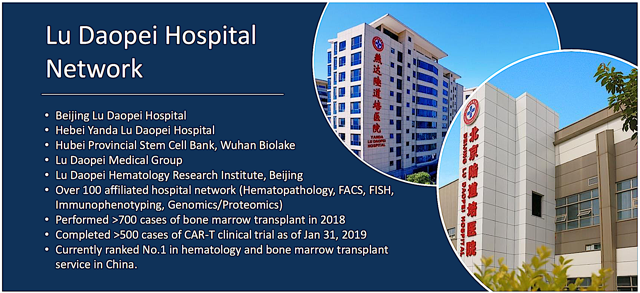

In my view, the collaboration is also favorable for GE because it can strengthen its brand through Avalon's extensive clinical network in China through Lu Daopei hospital network. Though Avalon has strong ties to Cornell Medicine, Lu Daopei hospital is just as reputable as Cornell. After all, it was founded by a stellar physician who is held in high regard in China. I believe that medical innovation is now shifting toward the East. And, China is becoming a global leader in serving the world's largest and increasingly wealthy population.

As a ramification, the partnership will galvanize Avalon's capability to answer the strong demand for cell-based therapies worldwide. For instance, the company can now ramp up its supply of clinical-grade cellular products consisting of chimeric antigen receptor (CAR-T), CAR-NK (natural killer cells), and stem cell-derived exosomes. Specifically, it ensures an adequate supply of biological specimens through scale-up manufacturing throughput and efficiency. Moreover, standardization and automation improve the specimen's uniformity.

Figure 6: Avalon's presence in the vast China market (Source: Avalon)

In growing its clinical and commercialization programs for cellular medicines, it's important for Avalon to have standardization, automation, and uniformity. The GE partnership provides all of that and more. Notably, Avalon is conferred with complete control of the whole development lifecycle. Hence, the company has the helm to fine-tune the innovation process from bench-research to treatment delivery. Consequently, the infrastructure and depth capability of GE ensure the successful execution of ongoing clinical investigations. As he captured the colossal deal in the most poignant terms, the President and CEO of Avalon (David Jin, M.D., Ph.D.) is stoked,

We are pleased to establish this strategic partnership with GE. This is a crucial and exciting time in the evolution of cellular medicines and our combined skills will drive Avalon to move innovation forward and ultimately deliver the best therapeutic solutions for patients. This partnership enables Avalon to more fully leverage and integrate our core technology platforms and accelerate our clinical programs in cellular immunotherapy and stem cell-derived exosome-based regenerative therapeutics. Empowered by GE’s leading automation and standardized cell processing/bio-production capabilities, we look forward to further upgrading our infrastructure, services and products, as well as expanding our leadership role in cellular medicines.

I concur with the illustrious Chief, as I believe in GE's centuries of legacy. In my view, it bodes well for shareholders when a young company can entice a highly reputable firm like GE. If the technology is subpar, I highly doubt that GE would be interested. Asides from its uncanny medicines and diagnostics, it's quite likely that Dr. Jin's reputation secured the deal. A larger firm usually works with a strong management who will deliver good results. The cream of the crop leadership improves the chances of successful innovation that in turn enhances the reputation of the partner. I explicated in the prior article,

As a physician and scientist, Dr. Jin provides Avalon an intellectual advantage in pipeline development. Due to his background and expertise, Dr. Jin has the capability to quickly size up a pipeline prospect for its chances of success. Correctly forecasting which drug has the best chance of success can save the company from billions of dollars that otherwise go into unfruitful and lengthy studies. It's interesting to note that Dr. Jin was the CMO of another company BioTime from 2009 to 2016. That experience enabled him to bring his regenerative medicine and stem cell technology expertise to Avalon. That aside, Dr. Jin served as the physician/scientist at the Howard Hughes Medical Institute and the Ansary Stem Cell Center at Weill Cornell Medical College of Cornell University.

Financial Assessment

Just as you would get an annual physical for your well-being, it's important to check up on the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll analyze the 1Q2019 earnings report for the period that concluded on March 31. Notwithstanding, I'll briefly touch on the most insightful metrics because I previously dissected the financials.

As follow, Avalon registered $284.1K in revenues compared to $307.9K for the same period a year prior. That aside, the research and development (R&D) came in at $152.4K. Additionally, there were $4.4M ($0.06 per share) net loss compared to $1.4M ($0.02 per share) decline for the same period of comparison. On the balance sheet, there were $1.8M in cash versus $2.1M for last year. With $6.0M from a direct offering raised back on April 25, the total cash position increased to $7.8M.

Against the $4.4M quarterly operating expense (OpEx) rate, Avalon will likely execute a public offering this quarter. In my observation, investors usually shy away from a public offering. Nevertheless, I prefer a young bioscience company to raise capital this way rather than incurring substantial bank debts. Short-term bank debts can be recalled anytime that can prompt a company to file a Chapter 11. The key to raising capital is to do it when the shares are trading high.

Though I do not mind a public offering, it's important for you to determine if you are holding a "serial diluter." A firm that employs dilution as a "cash cow" will render your investment essentially worthless. As the shares outstanding increased from 69.7M to 73.7M for Avalon, my rough arithmetics yield the 5.6% dilution. At this rate, Avalon easily cleared my 30% dilution cutoff for a profitable investment. Looking at the financial metrics, it's quite clear that Avalon is working for the best interests of the shareholders and patients.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strength. At this point in its growth cycle, I believe that the main concern is if Avalon can deliver positive data for various franchises. As the bulk value of the company resides in CAR-T, a negative clinical reporting for AVA-101 can cause the stock to tumble over 60% and vice versa. After accounting for all probability, I expect that AVA-101 to deliver excellent results. Therefore, the chances of a negative clinical binary are approximately 35%. The other risk is that the firm might grow aggressively and thereby runs into a potential cash flow constraint. GE can also terminate the partnership, thus limiting Avalon's reach.

Conclusion

In all, I maintain my strong buy recommendation on Avalon Globocare with the five out of five stars rating. On a one to three years horizon, I anticipated the $12.5 price target to be reached. You can read my valuation in the previous note. Due to the GE collaboration, I increased the "investment profitability score" to 70%. In a nutshell, you have a strongly favorable chance of making money on Avalon, provided that you hold the stock for the long haul. As it captures lightning in a bottle, Avalon is growing a prodigious pipeline of precision medicine that includes diagnostics, immunotherapy, and regenerative meds.

Among the countless CAR-Ts that I studied, Avalon's CAR-T is the most advanced. AVA-101 is ingeniously innovated by a Chief who knows the ins and outs of pharmaceutical developments. Going forward, I believe that it will disrupt the oncology space. But that's not all. The diagnostic for NASH or macular degeneration alone can easily garner blockbuster results. Then, there's regenerative medicine and diagnostics to confer additional profits and diversification. With GE's support, Avalon is cementing its leadership in this Golden Age of CAR-T.

As a reminder, the choice to buy, sell, or hold is ultimately yours to make. Nevertheless, it's prudent to accumulate stakes in Avalon to anticipate future data readouts. With Phase 1 and 2 trials having a high percentage of positive results, you can position yourself to enjoy the upcoming rally. In my view, this is a much better investment than betting on a preclinical-stage company.

Thanks for reading! Please hit the "Follow" button on top for updates.

Disclosure: As a medical doctor/market expert, Dr. Tran is not a registered investment advisor. Despite that we strive to provide the most accurate information, we neither guarantee the accuracy nor ...

more