The World Is Running Out Of Gold Mines—Here’s How Investors Can Play It

My good friend Pierre Lassonde, cofounder and chairman of Franco-Nevada, doesn’t know how we’ll replace the massive gold deposits of the past 130 years or so. Speaking with the German financial newspaper Finanz und Wirtschaft this month, Pierre says we’re seeing a significant slowdown in the number of large deposits being discovered. Legendary goldfields such as South Africa’s Witwatersrand Basin, Nevada’s Carlin Trend and Australia’s Super Pit—all nearing the end of their lifecycles—could very well be a thing of the past.

Over the medium and long-term, this could lead to a supply-demand imbalance and ultimately put strong upward pressure on the price of gold.

According to Pierre:

If you look back to the 70s, 80s and 90s, in every one of those decades, the industry found at least one 50+ million ounce gold deposit, at least ten 30+ million ounce deposits and countless 5 to 10 million ounce deposits. But if you look at the last 15 years, we found no 50 million ounce deposit, no 30 million ounce deposit and only very few 15 million ounce deposits.

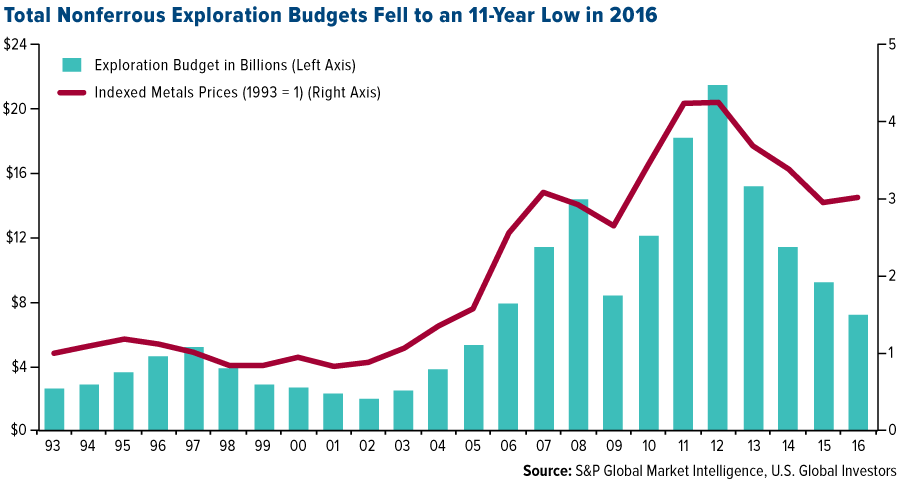

So few new large mines are being discovered today, Pierre says, mostly because companies have had to slash exploration budgets in response to lower gold prices. Earlier this year, S&P Global Market Intelligence reported that total exploration budgets for companies involved in mining nonferrous metals fell for the fourth straight year in 2016. Budgets dropped to $6.9 billion, the lowest point in 11 years. Although we’ve seen an increase in spending so far this year, it still dramatically trails the 2012 heyday.

And because it takes seven years on average for a new mine to begin producing—thanks to feasibility studies, project approvals and other impediments—output could recede even more rapidly in the years to come.

“It doesn’t really matter what the gold price will do in the next few years,” Pierre says. “Production is coming off, and that means the upward pressure on the gold price could be very intense.”

Have We Reached Peak Gold?

|

|

What Pierre is talking about, of course, is the idea of “peak gold.” I wrote about this last year and suggested another factor that could be curtailing new discoveries—namely, the low-hanging fruit has likely already been picked. Gold is both scarce and finite—one of the main reasons why it’s so highly valued—and explorers are now having to dig deeper and venture farther into more extreme environments to find economically viable deposits.

Other factors contributing to the decline include tougher regulations and higher production costs. And unlike with the oil industry, no “fracking” method has been invented yet to extract gold from hard-to-reach areas, though Barrick—the world’s largest producer by output—has been experimenting with sensors at its Cortez project in Nevada.

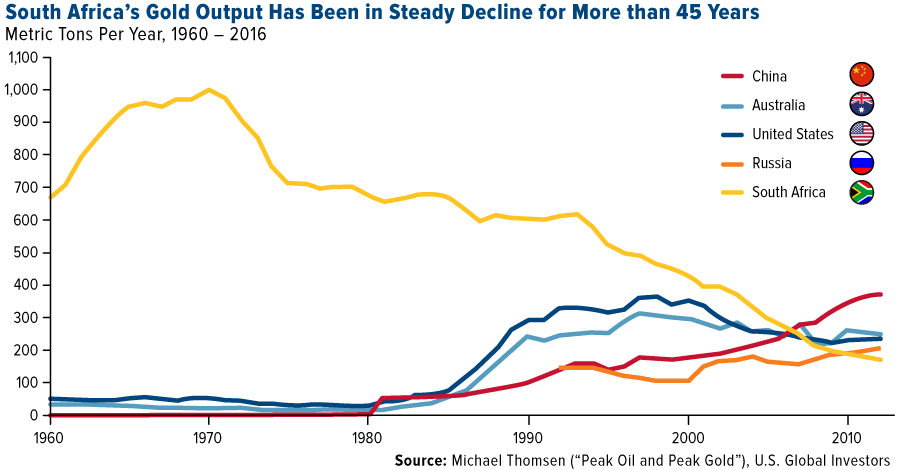

Take a look at how drastically annual output has fallen in South Africa, once the world’s top gold-producing country by far. In the 1880s, it was the discovery of gold in South Africa’s prolific Witwatersrand Basin—responsible for more than 40 percent of all gold ever mined in human history, if you can believe it—that helped transform Johannesburg into one of the world’s largest and most populous cities. Today, South Africa’s economy is the most advanced and stable in Sub-Saharan Africa, all thanks to the yellow metal.

In 1970, miners dug up more than 1,000 metric tons—an unfathomably large amount. Since then, production has steadily dropped. No longer in the top spot, South Africa produced only 167.1 tons in 2016, an 83 percent plunge from the 1970 peak. Meanwhile, miners in the notorious Mponeng mine—already the world’s deepest at 2.5 miles—continue to follow veins even deeper into the earth at greater and greater expense.

Australia could soon be seeing a similar downturn over the next four decades. A first-of-its-kind study conducted by MinEx Consulting and released this month, shows that Australia’s gold production is expected to see a significant drop between now and 2057. By then, all but four of the 71 currently operating mines in the country will be exhausted. Most of these will close in the next couple of decades. Any additional production will be dependent on new exploration success, which will become increasingly difficult if companies don’t invest in exploration and if the Australian government doesn’t relax rules in the mining space.

MinEx estimates that “for the Australian gold industry to maintain production at current levels in the longer term, it will either need to double the amount spent on exploration or double its discovery performance.”

To be fair, large discoveries haven’t disappeared entirely. Back in March it was reported that Shandong Gold Group, China’s second-largest producer, uncovered a deposit in eastern China containing between 380 and 550 metric tons of the yellow metal. If true, this would make it the country’s largest ever by amount. The mine has an estimated lifespan of 40 years once operations begin.

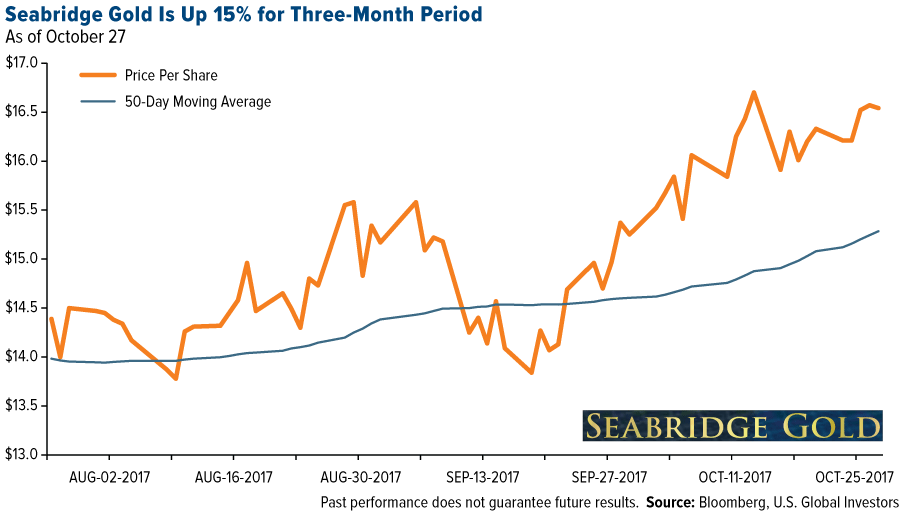

In addition, Kitco reports this month that Toronto-based Seabridge Gold (SA) recently stumbled upon a significant goldfield in northern British Columbia. The find appeared, coincidentally, after a glacier retreated. It’s estimated to contain a whopping 780 metric tons.

“There’s no question that as glaciers retreat, more ground will become available for exploration and more discoveries could be made in that part of the world,” Seabridge CEO Rudi Fronk told Kitco.

The company already has the permits to begin mining.

Exploration Budgets Jumped

|

|

As I said earlier, we just saw an encouraging spike in the amount spent on exploration. According to S&P Global Market Intelligence, exploration budgets increased in the 12-month period as of September for the first time since 2012. Budgets jumped 14 percent year-over-year to $7.95 billion, with gold explorers leading the way. During this period, gold companies spent around $4 billion on exploration, which is roughly half the value of all nonferrous metals mining budgets.

But because exploration is getting more expensive for reasons addressed earlier, senior producers might very well decide instead to acquire smaller firms with proven, profitable projects.

This could create a lot of value for investors, so I would keep my eyes on juniors that look like targets for takeover. Dealmaking in the Australian mining industry, for example, is showing some growth this year compared to last, according to a September report by accounting firm BDO. Last year, Goldcorp (GG) finalized its deal to acquire Vancouver-based junior Kaminak Gold, and in May of this year, El Dorado (EGO) announced it was taking over Integra Gold for C$590 million. I expect to see even more deals in the coming months.

In the meantime, I agree with my friend Pierre’s “absolute rule” that investors should hold between 5 and 10 percent gold in your portfolio. I would also add gold stocks to the mix, especially overlooked and undervalued names, and rebalance once and twice a year.