The Magnitude Of Long Term Profits In A Gold Secular Cycle

Gold has recently been setting all-time highs on a nominal basis and has broken the $2,000 an ounce barrier. It had been eight years since a new high had been set, and this is obviously an important event.

However, when compared to the magnitude of gold gains over a secular cycle, the recent price movements have been quite small in comparison to what history shows us could be on the way. To see why this is the case, we need to move from measuring the consistency of the price advantage that gold builds over stocks in a secular cycle, to the cumulative magnitude of the relative gains.

As we will explore, for two investors starting with equal assets, the historical norm is for an investor in the correct asset to have 2 times to 5 times the net worth of an investor in the wrong asset, within 3-5 years of a new secular cycle starting. This extraordinary degree of wealth creation/destruction is so large that it may seem improbable - but it is just what history shows us, and a swing in wealth of this magnitude occurred in all four of the secular cycles studied herein.

(Click on image to enlarge)

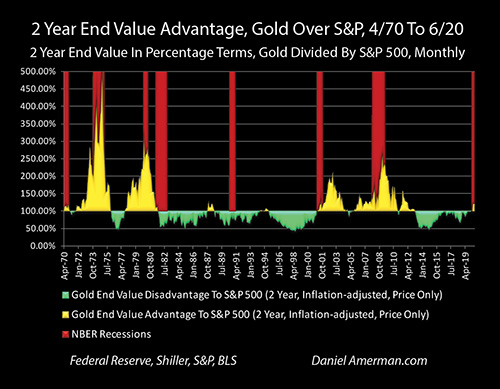

As developed in Chapter Nineteen (link here) and other prior analyses, using two-year rolling comparisons is a very good way of seeing the contracyclical and secular relationship between gold prices and stock prices (as shown with the S&P 500 index above). There are long cycles, where the rolling two-year comparisons almost always favor gold, and there are long cycles where the rolling two-year comparisons favor stocks.

While very useful for identifying the contracyclical relationship and the cycles, the two-year rolling comparisons do not show the very large cumulative advantage to one asset over the other, that builds over the long course of the cycle.

Rephrased, the two-year rolling advantage comparison is a good measure of the consistency of the advantages of an asset over a cycle, but not a good representation of the relative magnitude of the advantages to that asset over the other for the cycle.

If we do indeed turn out to be beginning another long term (secular) cycle favoring gold over stocks, most of the gains do not occur during the first year, but instead steadily build over time. Each of the two-year rolling averages effectively stack upon each other, and lead to a much greater magnitude to the advantages for one asset class over the other, for whichever is the ascendant asset class in that cycle.

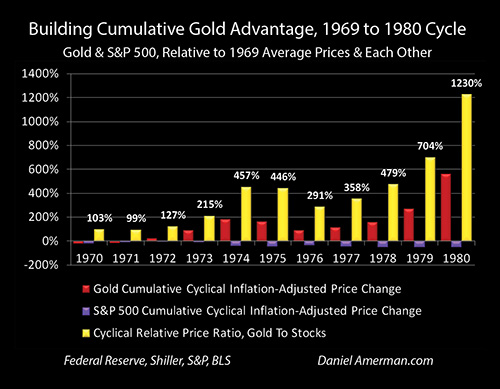

To see the magnitude, we need to move from two year comparisons to looking at changes in value over the full course of the secular cycle, as measured from the first year of the cycle. A good historical example can be seen when we review the 1969 to 1980 cycle that favored gold over stocks in the graph below, with all comparisons being relative to the starting year of 1969.

This analysis is part of a series of related analyses, which support a book that is in the process of being written. Some key chapters from the book and an overview of the series are linked here.

The 1969 To 1980 Cycle: Gold Over Stocks

(Click on image to enlarge)

For 1970 and 1971 the asset classes were each slightly negative, and very close - on an inflation-adjusted basis. As developed in previous analyses, to properly see the cycles and the contracyclical relationship, the prices always need to be viewed on an inflation-adjusted basis. This is also appropriate because both gold and common stocks are considered to be inflation hedges over the long term, and whether the inflation hedge succeeds in practice or not can be of vital importance to long term investors, particularly in retirement.

A result of 0% means the asset class exactly kept up with inflation - there was no change in value in inflation-adjusted terms - which means it was a successful inflation hedge. Even zero percent is success for investors seeking inflation protection, the asset was a stable store of value. Any result less then 0% means the asset, whether stocks or gold, did not keep up with inflation. Any result above 0% means the asset not only kept up with inflation but went beyond that.

When we look at inflation-adjusted price changes in percentage terms for each asset over the long term, the contracyclical nature of the two assets becomes boldly obvious. Every year from 1972 and beyond, gold is worth more in inflation-adjusted terms than it was in 1969, it was in a secular up cycle. Every year from 1972 and beyond, stock prices are worth less in inflation-adjusted terms than they were in 1969, it was in a secular down cycle. They produced opposite results for investors.

Taking a closer look at 1974, compared to their starting values in 1969 (annual averages), the inflation-adjusted average price of gold was up by 188%, and the inflation-adjusted price for stocks was down by 37%. As a starting point then, during that time of rapidly rising inflation and the early years of stagflation (which could yet be of great relevance when it comes to the 2020s), gold did not just meet its requirement to protect against inflation, but greatly exceeded that threshold. Instead of a 0% change in inflation-adjusted value, gold almost tripled in purchasing power.

If we look at the S&P 500 index for those same years, then on the surface, stocks "only" fell in value by about 16% over the five years. However, when we adjust for the 25% destruction of the purchasing power of the dollar over those same years, then in inflation-adjusted terms the value of the S&P 500 index was down by 37%. So, in the same first five years, while gold was exceeding what was needed in order to be an effective protection against inflation for investors, common stocks were failing as an inflation hedge.

(Click on image to enlarge)

When we put the two together, by 1974 an investor in gold would have had 288% (100% + 188%) of the purchasing power of the money they started with in 1969. On an inflation-adjusted price basis (not including dividends) an investor in the S&P 500 would have had 63% (100% - 37%) of the purchasing power they started with. So, if an investor had chosen to be in gold instead of stocks over the five years, they would end up with 4.57X the assets in 1974 that they would have had on a price basis if they had chosen stocks instead (288% / 63% = 457%), as shown with the yellow bar for 1974 above.

That magnitude of an almost 5X difference in ending net worth, over a period of just five years is a life changing difference, particularly for someone in retirement or on the verge of retirement. This is the cumulative power of the contracyclical cycles, and a saver having almost five times the net worth as a result of being in the correct asset for the cycle in a time of economic distress and rising inflation was the actual historical result.

Over the course of the secular cycle, the rolling two-year advantage was not 100% (reality rarely is), but it was highly consistent overall, with 109 of the 137 monthly rolling two year advantages favoring gold over stocks, and only 28 favoring stocks over gold (this is measured by monthly averages rather than annual). So, over the secular cycle, if someone had owned gold rather than stocks in any given month, then 80% of the time they would have better off two years later.

When we look at magnitude, then the 109 rolling two-year advantages to gold built up on top of each other, albeit being partially offset by 28 two year advantages to stock going the other direction. In combination, as shown by the height of the gold bars, on a price basis starting from 1969, an investor in gold would have had been 2.1X better off than a stock investor by in four years, 4.5X in six years, 3.6X in eight years, and 12.3X better off in eleven years.

What the historical record of the contracyclical relationship between gold and stocks shows is that combination of consistency and magnitude were indeed of life changing significance when measured using average results over long term periods.

The 1980 To 2000 Cycle: Stocks Over Gold

(Click on image to enlarge)

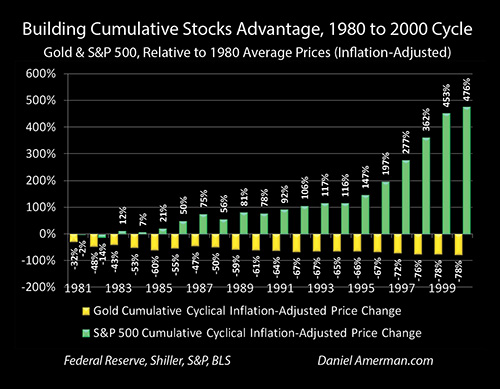

However, when the cycle changes, then everything else changes. From 1983 onwards, every green bar is now positive, meaning the price of the S&P 500 was higher in inflation-adjusted terms than it was in 1980.

For the entire 20 years, every yellow bar is now negative, meaning gold was worth less in inflation-adjusted terms. As explored in more detail in Chapter 16 (link here), the actual historical relationship between gold and inflation is not at all what many people think it is.

When we compare the 1980 to 2000 secular cycle to the 1969 to 1980 secular cycle, while we do not see the commonly expected inflation protection from gold, what we do see is a complete inversion in how stocks and gold perform over the long term, which validates the very valuable contracyclical relationship between the two asset classes.

If we look at the 1980 to 2000 period, there is a very consistent secular cycle of stocks outperforming gold. There were 213 rolling two-year comparisons favoring the S&P 500 over gold over almost 20 years, and only 21 with an advantage favoring gold.

Despite its reputation as a reliable source of inflation protection, gold in fact lost 53% of its value by the time we were four years into the new secular cycle - even while the S&P 500 was slightly outperforming inflation, increasing by 7%. It was now stocks that were acting as a successful inflation hedge, even while gold was failing investors.

Over 10 years, the consistency of stock prices outperforming gold meant that stocksprices would not just keep up with inflation but would exceed it by 78% - even while gold prices fell by 61% in inflation-adjusted terms.

The consistency would continue over the next 10 years, and by the time we reach 20 years after the start of the cycle in 1980 - stock prices were up by 476%, even after adjusting for the dollar having lost 52% of its purchasing power. Meanwhile, the contracyclical asset of gold had utterly failed as an inflation hedge, losing 78% of its value in inflation-adjusted terms.

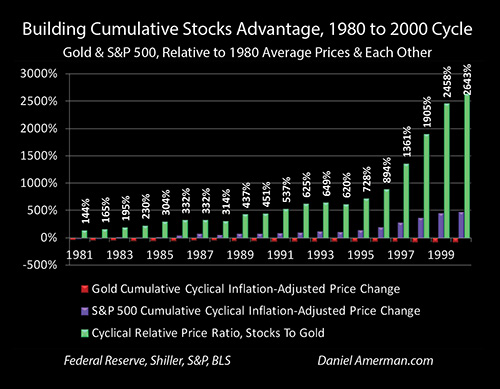

(Click on image to enlarge)

This highly consistent rolling two-year advantage to stocks over gold over the twenty years produced an ever growing magnitude of gains for stock investors relative to gold investors. In just the first five years, an investor in the S&P 500 on a price basis would have had three times the net worth of an investor in gold.

Indeed, the magnitude of the historical swings might seem hard to believe or to be improbable - but it is just simple history. The issue is how many savers and investors are following common belief systems that they believe to be accurate but are not consistent with actual history.

Historically, an investor in gold in 1969 would have had almost five times the net worth five years later in 1974 than they would have had if they had been invested in the S&P 500. Historically, an investor in stocks in 1980 would have had more than three times the net worth five years later in 1985 than what they would have had if they had been invested in gold (and this is before dividends).

The advantage to being invested in stocks instead of gold in almost any given two year holding period would then continue for the next fifteen years. And as those consistent gains built, and built and built upon each other, the magnitude of the gains over the secular cycle kept rising as well.

The advantage to being in stocks would be to have more than 6X the net worth over ten years, relative to being invested in gold.

Someone who started with $500,000 in 1980 would have had $170,000 in inflation-adjusted terms by 1995 if they had been entirely invested in gold but would have had $1,235,000 in inflation-adjusted net worth (on a price only basis) if they had been invested in the S&P 500 over the fifteen years. The magnitude of that real world, real history 728% net worth advantage could have had truly life-changing implications when it comes to financial security, the ability to retire, and the standard of living in retirement. It is also vital to keep in mind that this is in inflation-adjusted terms, if we look at in just simple dollar terms, the stock investor would have turned $500,000 into $2.3 million (before dividends), while the gold investor would seen their value fall to $314,000.

Over the following five years, stocks would enter bubble territory, creating a long string of consistent two-year rolling advantages and a new generation of day traders, even while gold continued its two-decade slide. So that by the year 2000, the final year of the secular cycle, the magnitude of the cumulative advantage to stocks over gold was an astounding 26 to 1 increase in relative net worth.

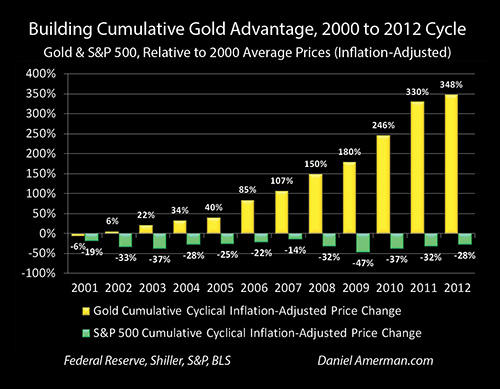

The 2000 To 2012 Cycle: Gold Over Stocks

Then the secular cycles flipped again, with the collapse of the tech-stock bubble and the resulting recession.

Memory and belief systems are an interesting thing. Ask many investors, and they would likely say that gold took off in the financial crisis of 2008, but then peaked and began falling in 2012 when as it turns out, the world didn't end after all. There is some truth to that - but not the whole truth, indeed the actual historical record was quite different.

(Click on image to enlarge)

As can be seen in rolling two-year advantage graph above, almost the entire area of the graph between 2000 and 2012 is yellow - with each one of the those data points being a separate, consistent two year advantage to investing in gold over stocks.

It wasn't just the collapse of the tech-stock bubble. It wasn't just the collapse of the real estate bubble or the financial crisis of 2008. On a highly consistent basis, right through the early and mid-2000s, gold just kept climbing, and climbing, and climbing, right through the growth of the real estate bubble. This was also a time when the S&P 500 fully recovered on a nominal (not adjusted for inflation) basis, with an annual average index price of 1477 in 2007, which exceeded the prior average annual high of 1427 set in 2000.

(Click on image to enlarge)

Again, the remarkable consistency of the contracyclical relationship between gold and stocks over the secular cycles can be seen in the graph above. We have another inversion, and for every year from 2002 onwards it is the yellow bars of gold that are experiencing inflation-adjusted gains that exceeded the rate of inflation on a cumulative basis by a greater margin each year. So the value of gold in cumulative and inflation-adjusted terms rose 40% from 2000 to 2005, then 85% from 2000 to 2006, then 107% from 2000 to 2007, and so forth.

Stock prices meanwhile were consistently negative in every single year in inflation-adjusted terms (relative to 2000), meaning that stocks were consistently failing as inflation-hedge, even as gold was exceeding the requirements for an inflation hedge by ever greater margins each year.

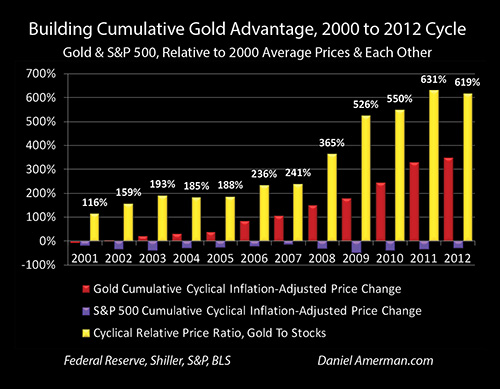

(Click on image to enlarge)

When we take the consistency of the two-year advantages and let them build on top of each other over time, then we get the magnitudes shown in the graph above. An investor in gold would have had almost twice the net worth compared to an investor in stocks after just the first three years.

When we look at 2007 - before the financial crisis and during the year the S&P 500 set all-new nominal average annual highs - the cumulative magnitude of the advantage to gold prices over stock prices was still up to almost 2.5 to 1.

By 2009 the financial crisis had occurred, and an investor who started with $500,000 in the year 2000 would have had $1.4 million in inflation-adjusted wealth if they had invested in gold, but if they had invested in stocks instead then their inflation-adjusted net worth would have been down to $265,000. This 5.3 to 1 net worth advantage to gold over stock prices could again have made a life-changing difference to an investor when it comes to financial security, or the ability to retire, or the standard of living in retirement.

Yes, that 5.3 to 1 advantage occurred in the year of the depths for the U.S. economy and stock market - but on a relative basis, gold would still consistently outperform stocks for the next three years, using the rolling two-year comparison basis. And those consistent advantages, building on the base of the 5.3 to 1 advantage in 2009, would lead to a 5.5X advantage for 2010, a 6.3X advantage for 2011, and a 6.2X advantage for the full 12 years of the secular cycle.

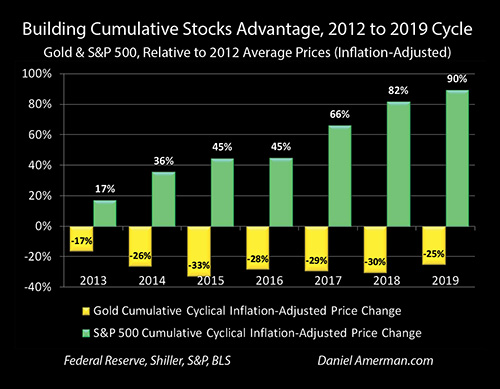

The 2012 To 2019 Cycle: Stocks Over Gold

(Click on image to enlarge)

When the secular cycles flipped again in 2012 - we see another inversion and another demonstration of the contracyclical relationship between gold and stocks. The green bars flip to all positive, and the yellow bars flip to all negative

It is now the green of the S&P 500 that has a remarkable consistency - with prices equal to or higher than the previous year, without exception. Keep in mind - a 0% change in inflation-adjusted price means a perfectly successful inflation hedge, one that exactly maintaining purchasing power. Stocks not only exceeded that requirement in every year, but they did so in a manner such that investors steadily built ever greater amounts of wealth in excess of the rate of inflation in each year.

The gold bars of gold prices are now well below the average inflation-adjusted price in 2012, without exception. Rephrased, when compared to 2012, gold failed as inflation hedge in each year thereafter.

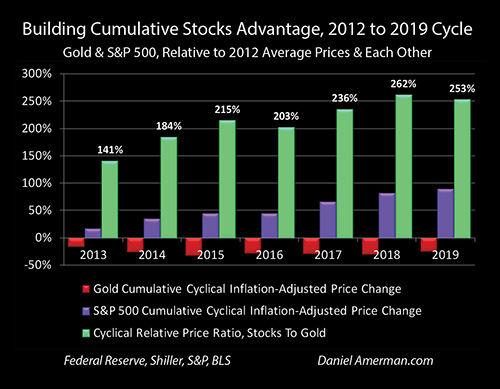

(Click on image to enlarge)

When we put the relative price changes together, then it took only three years to reach the place where a stock investor would have more than twice the net worth than they would have had if they had been a gold investor. By six years, they would have had about 2.6X the assets on a price basis, and by seven years, it would have been 2.5X the assets.

The latter 2010s are a good period for distinguishing between the consistency of two-year rolling returns, and the cumulative magnitude of those returns.

(Click on image to enlarge)

When we look at the green area of rolling relative two-year returns on the graph repeated above, it looks like the peak advantage to stocks was early on, and it occurred by around 2014. There is truth to that perspective, and that was the biggest jump.

However, while the degree of relative price change was the greatest fairly early on - it didn't end then. So long as there is green on the graph, then there is a fresh two-year advantage to stocks over gold. Long after 2014, we were seeing fresh two rolling advantages from different months in 2015 to 2017, and from 2016 to 2018, and so forth. On a cumulative basis, those new gains stacked on top of the old gains, and the cumulative magnitude of the advantage to being in the correct asset for the secular cycle continued to build and build and build.

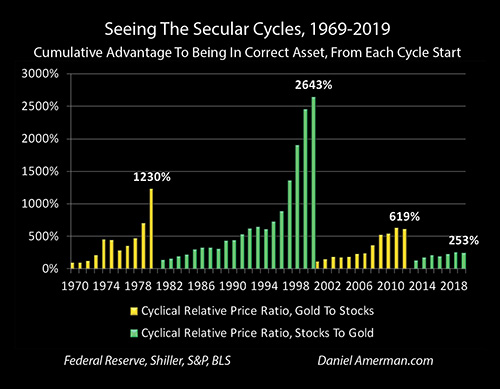

Putting The Cycle Magnitudes Together

This cumulative building magnitude of a series of consistent relative advantages strung together and building upon each other can be seen with all four secular cycles when they are combined in the graph below.

(Click on image to enlarge)

The advantage to gold over stocks built over 11 years between 1969 and 1980, and even though the peak rolling two-year advantage was 1972 - 1974, the cumulative advantage to gold over stocks kept building right through 1980. It was all those years stacking on top of each other that was produced the amazing 12 to 1 cumulative price advantage for long term investors in gold.

If we look at the stock secular cycle of 1980 to 2000, then it is boldly obvious that the last three years of the cycle, with the growth of the stock bubble, was a good part of the extraordinary 26 to 1 advantage that stock investors had over gold investors during this time. However, that wasn't the most important part of the cycle, it was the 17 years of stringing together a very long series of consistent relative advantages to stocks over gold, year after year after year, that built the cumulative advantage to stocks to 13 to 1 by 1997.

Looking at the 2000 to 2012 cycle, then yes, the surge in gold prices relative to stock prices during the financial crisis of 2008 and the Great Recession can be clearly seen. But it is quite obvious that the secular advantage to gold over stocks had been steadily building for a number of years before the crisis, and that this continued after the crisis as well.

The contracyclical relationship and the power of the building cumulative magnitude of the gains in the asset in its up cycle versus the asset in the down cycle are then quite clearly demonstrated again in 2012 to 2019 cycle, with stocks powerfully outperforming gold by a 2.5 to 1 ratio.

A Potential Change In The Cycles

(Click on image to enlarge)

As shown above and as explored in a previous analysis (link here), the relationship between stocks, gold, and recessions has reached a place in 2020 that has only been seen twice before over the last fifty years. After a long green cycle favoring stocks over gold, the two-year rolling advantages have flipped over to gold over stocks, and a golden spike is moving upwards in the midst of the red of a severe recession. Each of the previous times that has happened - there has been a change in the secular cycles.

If that is indeed happening again, then the potential magnitude of the implications for investors needs to be understood, and that was the subject of this analysis. Hopefully, it has been helpful for you in that regard.

However, keep in mind that the magnitude of the swings in the contracyclical relationship does much more than just reward correct market calls. It is the swings in the magnitude that produce the risk reduced combined strategies, including the rebalancing strategies, the ratio strategies, and the ratio rebalancing strategies. Using these strategies that are specifically designed for contracyclical assets in secular cycles, there is the ability to at least partially participate in the upside for each cycle, while taking much less risk on a portfolio basis than would be the case with pure stock or pure gold strategies.

Learn more about the free book.

Disclosure: This analysis contains the ideas and opinions of the author. It is a ...

more