Strong October Jobs Data Stun Gold. For How Long?

The recent employment report points to the continuing strength of the U.S. labor market. The earlier months' upward revisions paint the same picture. Yet the unemployment rate ticked higher - is a recession looming, or not? And what does it all mean for gold?

October Payrolls Better Than Expected, But Unemployment Rate Edges Up

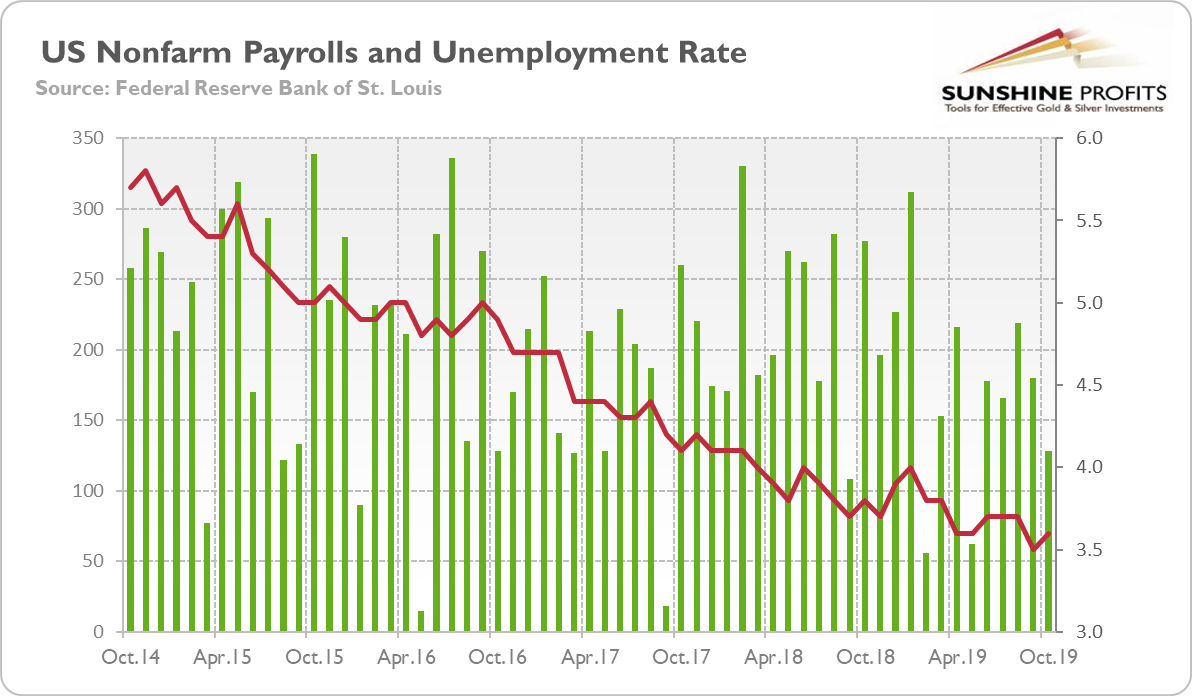

The U.S. created 128,000 jobs in October, following an increase of 219,000 in September (after an upward revision). The nonfarm payrolls came above expectations. The analysts forecasted only 75,000 new jobs, as they thought that the strike at General Motors would be more detrimental for the employment numbers. The gains were widespread, but with a leading role of leisure and hospitality (+61,000), and education and health services (+39,000). Manufacturing again cut jobs, which is another sign of the industrial slowdown. This time the reduction was really deep, as 36,000 people lost jobs in manufacturing. However, the big cut was in part caused by the strike in General Motors.

The surprisingly decent headline number was accompanied by upward revisions in September and August. Counting these, employment gains in these two months combined were 95,000 higher than previously reported. That's a lot! Consequently, the job gains have averaged 176,000 per month over the last three months, and 167,000 so far this year - very respectable but still significantly below the average monthly gain of 223,000 in 2018.

Although the U.S. economy is still creating jobs at a reasonable pace, the unemployment rate ticked up, from 3.5 to 3.6 percent, as the chart below shows. It is still near the 50-year low, but if it rises again soon, we could start to worry.

(Click on image to enlarge)

Chart 1: U.S. nonfarm payrolls (red bars, left axis, change in thousands of persons) and the unemployment rate (green line, right axis, %) from October 2014 to October 2019.

Last but not least, the average hourly earnings for all employees on private nonfarm payrolls have increased 3.0 percent over the last twelve months, following a 2.9-percent rise in September. The acceleration in the wage inflation should please the Fed, but it should not significantly impact its stance.

Hence, the October jobs report is positive for the U.S. economic outlook. The labor market shows resilience in general, with above-consensus hiring and upward revisions to prior months. The downturn in manufacturing sector has not yet caused broader issues in the labor market. The overall economy is, thus, still doing relatively well and the U.S. labor market is likely to further contribute to the longest expansion on record, at least for a certain time. This is bad news for gold prices.

We hope you are enjoying today's analysis so far. Normally, the above paragraph would mark the end of the free analysis and the rest would be reserved only to premium subscribers. However, since this is the very first issue of our new product: Fundamental Gold Report, we are publishing it free in its entirety. In order to receive the following (posted bi-weekly) analyses and stay informed on all things fundamentally golden, please subscribe now on our website. And now for the remaining part of the analysis...

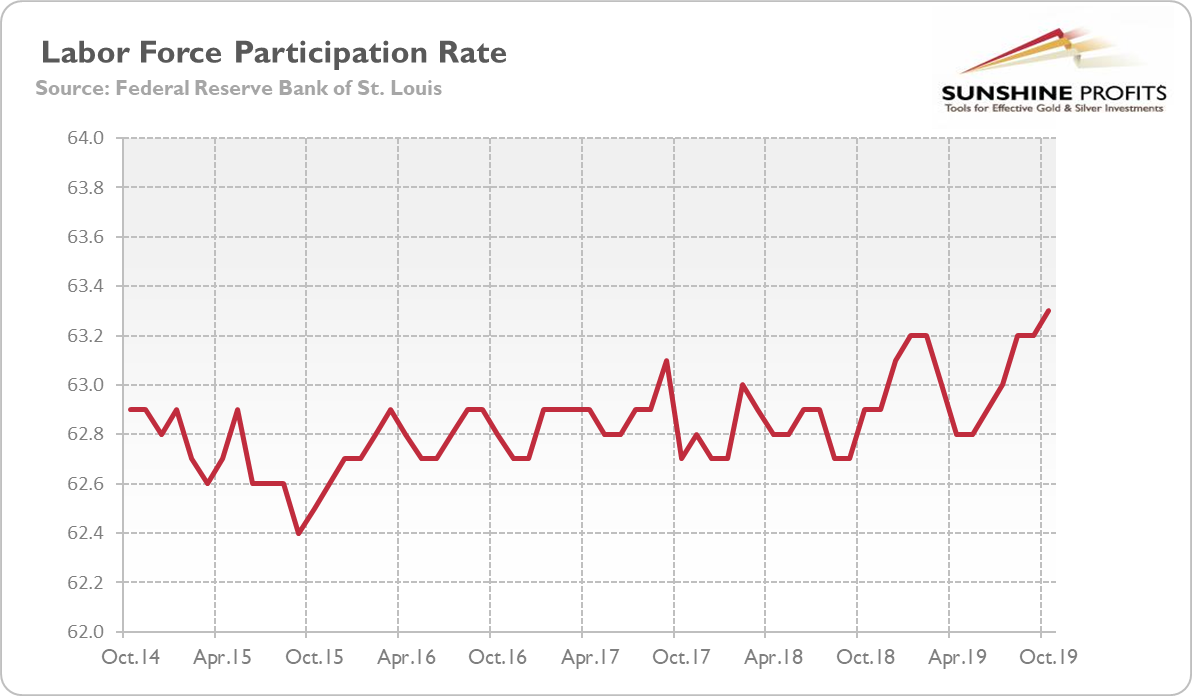

The unemployment rate increased in October. Is it a worrying sign for the U.S. economy? Not really. First, the rise in the unemployment rate in October was accompanied by the increase in the participation rate, from 63.2 to 63.3 percent, as one can see in the chart below. It means that more people - about additional 325,000 previously discouraged individuals - entered the labor market to find a job, pushing the unemployment rate higher.

(Click on image to enlarge)

Chart 2: US labor force participation rate from October 2014 to October 2019

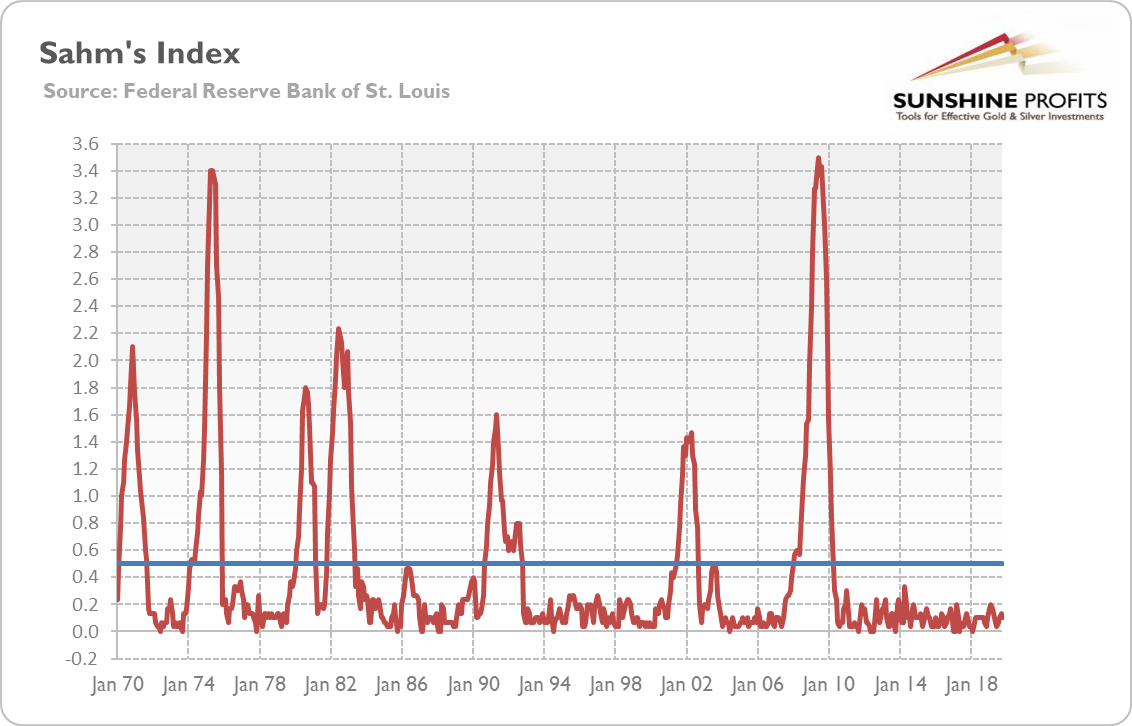

Second, Sahm's indicator tells us not to worry. What is the Sahm's index anyway? It's the indicator based on the unemployment rate. The raw unemployment rate is powerful recessionary indicator, but it's not easy to determine it in real-time. The Sahm's index is a new tool to solve this problem. As I explained in the August edition of the Gold Market Overview, the economy is thought to be headed for recession, when the three-month average unemployment rate is at least 50 basis points above its minimum from the previous twelve months.

So, let's take a look at the chart below. The three-month average unemployment rate is just 0.1 percentage point above its minimum of the past twelve months. It implies that the labor market remains healthy and does not signal an imminent recession, despite the recent rise in the unemployment rate. The Sahm's indicator stays at a very low level, and it is not rising toward the recessionary threshold, at least not yet.

(Click on image to enlarge)

Chart 3: Sahm's Index (the difference between the three-month average of unemployment rate and the minimum from the previous twelve months) from January 1970 to October 2019.

Implications for Gold

What does it all mean for the gold market? Well, strong U.S. labor market does not help gold prices to go up. The Fed officials welcomed the October job report. Richard Clarida, the Fed Vice Chair, said on Friday that he is "very happy" with the stance of monetary policy, suggesting no more interest rate cuts for a moment. The decent job creation will support the current record-long expansion, preventing the yellow metal from rallying.

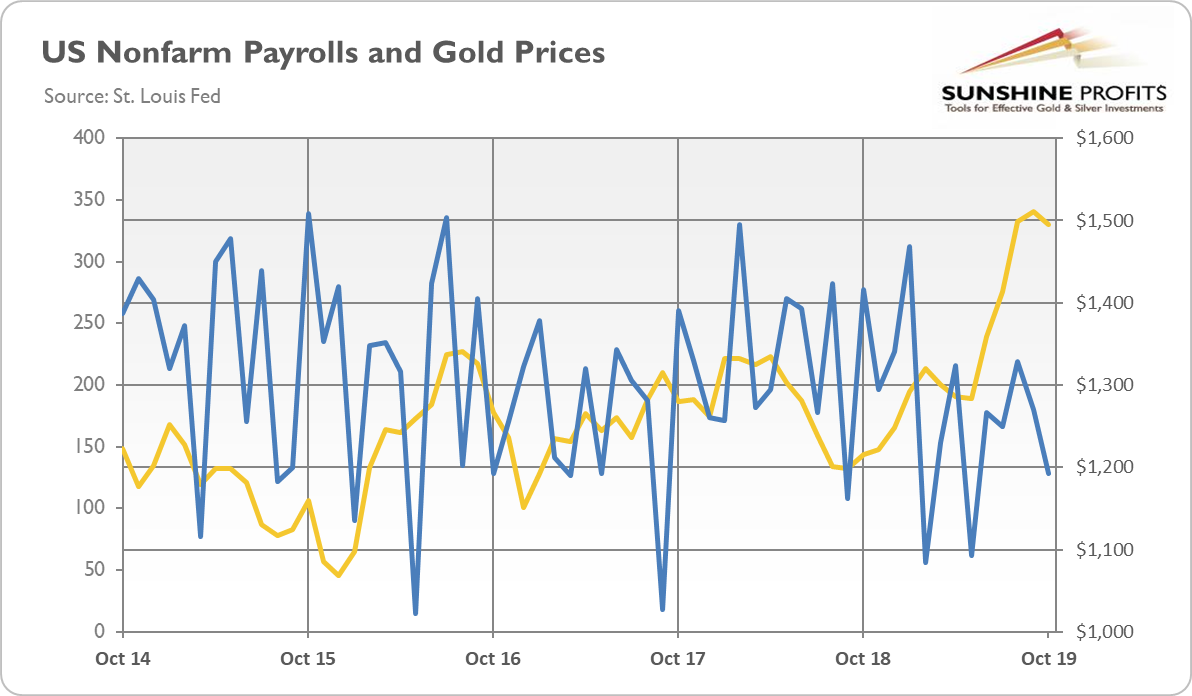

However, investors should be aware that there is no clear long-term relationship between the gold price and job gains (see the chart below). I mean that the correlation between the monthly changes in the nonfarm payrolls and the monthly averages of gold prices is very low. In the past, the relationship was stronger. For example, the correlation was -0.34 in 2017. But in 2019, it amounts to a mere 0.06.

(Click on image to enlarge)

Chart 4: Total nonfarm payrolls (blue line, left axis, monthly change in thousands of persons) and the price of gold (yellow line, right axis, London P.M. fixing) from October 2014 to October 2019

What explains the differences? Blame the Fed. You see, sometimes the developments in the labor market are key inputs in the Fed's reaction function. Then, the relationship between the nonfarm payrolls and gold, especially in the short-term, may be stronger. But sometimes, such as today, inflation become more important. Or political pressure. Or trade wars and general uncertainty. Or the yield curve. In such periods, the link between the job gains and gold prices will be weaker.

So, although currently the relationship is relatively weak now, it does not have to stay so in the future. Actually, when labor market conditions deteriorate and the unemployment rate rises, gold could react more intensively to the Employment Situation Report.

By the way, the shifting correlations is why the gold market is very challenging for beginners and why investors should always analyze the broader macroeconomic context instead of focusing on simple and fragmented relationships. This is why it's worth to read our Fundamental Gold Report regularly - it presents you with all the nuances of the gold fundamental outlook.

If you enjoyed the above analysis and would you like to know more about the most important macroeconomic factors influencing the U.S. dollar value and the price of gold, we invite you to read the ...

more