Some Needed Perspective On Gold And Silver

As the prices for gold and silver continue to vacillate, investors and others who are price dependent might find themselves a bit anxious regarding both metals lack of obligatory action to the upside.

One of the most oft-stated arguments in favor of higher prices for gold (particularly) and silver is their presumed sensitivity to inflation. Simply stated – as inflation gets worse, the prices for gold and silver can be expected to rise, or rise higher and faster depending on how bad things get.

Below are charts for both gold and silver which date back to their most recent inflation-adjusted peaks in August 2020…

Gold Prices (inflation-adjusted) – Historical Chart 2020-23

(Click on image to enlarge)

Silver Prices (inflation-adjusted) – Historical Chart 2020-23

(Click on image to enlarge)

In looking at both charts it is clear that the prices of gold and silver are not reacting ‘favorably’ to the worst inflation numbers in four decades. Rather than “rise higher and faster”, the inflation-adjusted prices for both metals have declined since their peaks in 2020.

We could argue that the rise to the high in 2020 was in anticipation of the worsening inflation numbers yet to come (at that time), but that is not how gold works, and the argument for silver is even weaker.

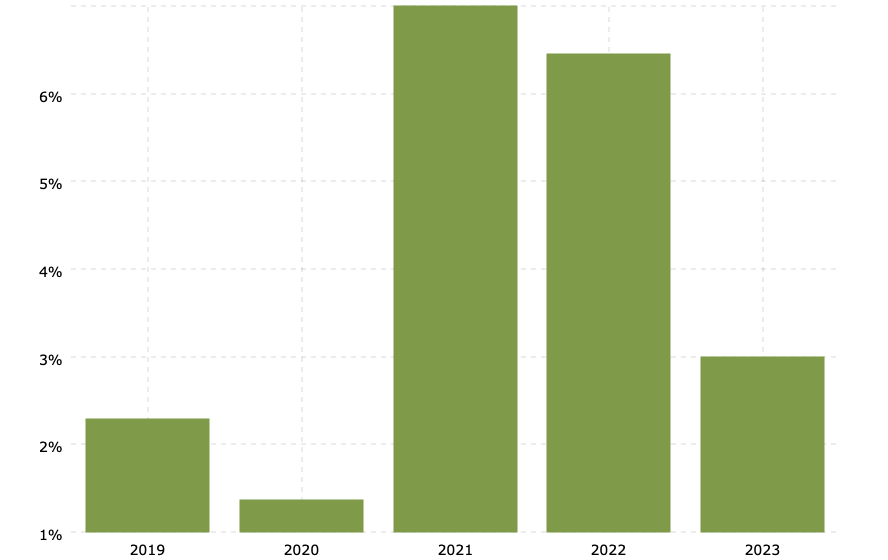

Gold is not forward looking. Its price only rises after the effects of inflation are known and have been recognized for a long enough period of time. Below is a chart of consumer prices (effects of inflation) which corresponds to the time frame for both charts above…

Historical Inflation Rate by Year

(Click on image to enlarge)

The peaks for both gold and silver in 2020 came before those “worst inflation numbers in forty years.” Also, the inflation-adjusted prices for both gold and silver have moved steadily lower – rather than higher – in the face of worsening inflation numbers.

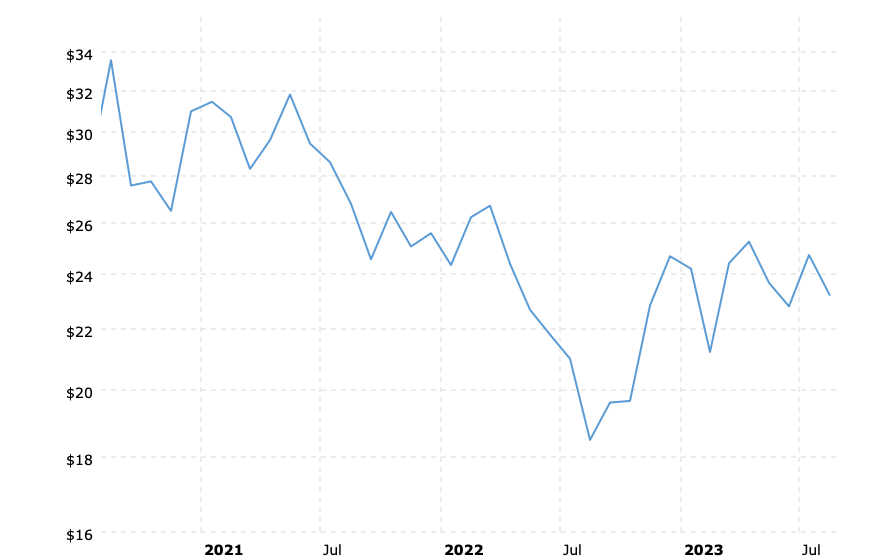

Earlier this year the gold price briefly and barely exceeded its 2020 high. That is shown on the chart below…

Gold Prices – Historical Chart 2020-23

(Click on image to enlarge)

Is matching its previous high an indication that gold is responding to the recent worsening effects of higher inflation? Possibly, but the fact remains that neither gold nor silver are keeping pace with inflation’s effects – at least in the short term.

In the longer term, the gold price does reflect the effects of inflation. However, historically, the response is not very timely. Below is a long-term chart of the gold price…

Gold Prices (inflation-adjusted) – Historical Chart 1970-2023

(Click on image to enlarge)

The three peaks on the gold chart above correspond to the loss of purchasing power in the U.S. dollar.

By 1980, the U.S. dollar had lost ninety-seven percent of its purchasing power. That loss corresponds to a gold price of $680 oz. (monthly average closing price) at that time.

Similarly, a further loss of U.S. dollar purchasing power was reflected in a nominal gold price of more than $1800 oz. in 2011.

The 2020 peak for gold at more than $2000 oz. was indicative of a full ninety-nine percent loss of purchasing power in the U.S. dollar.

Over time, the effects of inflation, i.e., the loss of purchasing power in the U.S. dollar, show up in a higher nominal gold price. The moves in the gold price, however, are few and far between; and are a catch up to the past effects of inflation.

Silver is a different animal entirely. While gold is primarily real money, silver is basically an industrial commodity.

As such, it is more responsive to traditional supply and demand forces. While it does tend to move in sympathy with gold, the silver price over time lags considerably the long-term price appreciation of gold and is much more vulnerable on the downside.

See the long-term chart for silver below…

Silver Prices (inflation-adjusted) – Historical Chart 1970-2023

(Click on image to enlarge)

WHAT YOU NEED TO KNOW

As long as the effects of inflation continue to show up in higher prices for goods and services, a higher nominal gold price can be expected over the long term – eventually.

Once any catch-up move is complete, however, the gold price can lag ongoing inflation effects for years at a time.

Silver is primarily an industrial commodity. Over the long term its price has historically declined in inflation-adjusted terms – in a substantial way.

Whatever arguments are made in favor of a higher silver price need to be strong enough in their own right in order to compensate for the negative inflation drag on the silver price.

More By This Author:

Four Signs The Economy Is In Decline

Too Soon For New Highs In Gold

Stock And Bond Expert Makes Case For PMC Ounce And Gold – National Debt A Key Price Driver