Natural Gas Review For Thursday, July 2

SUMMARY

-

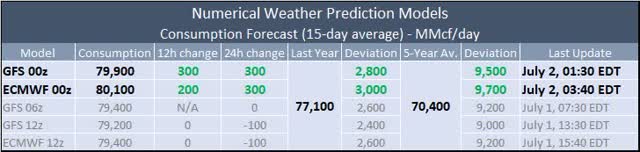

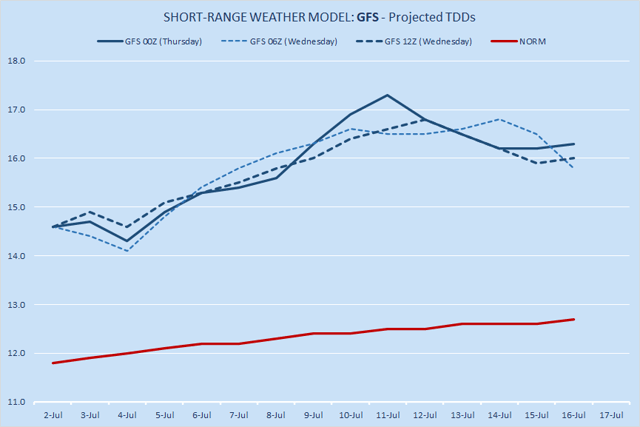

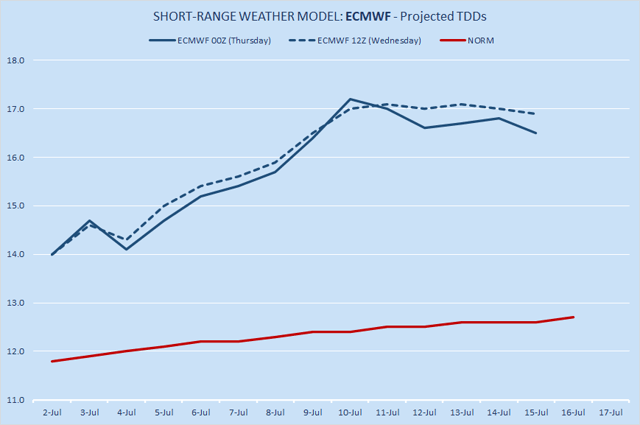

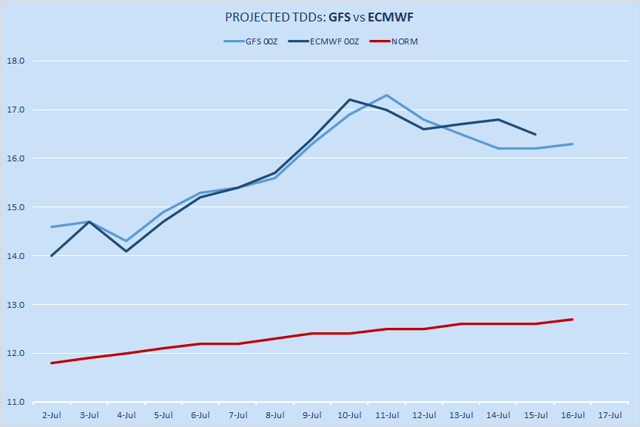

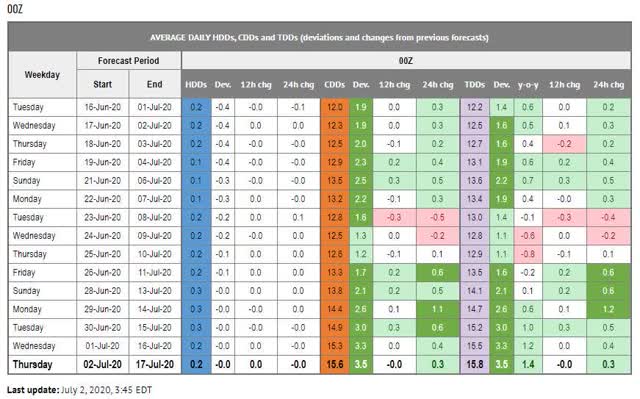

Consumption-wise, ECMWF 00z Ensemble is bullish vs yesterday's 12z results. In absolute terms, ECMWF model is projecting slightly more TDDs than the latest GFS model.

-

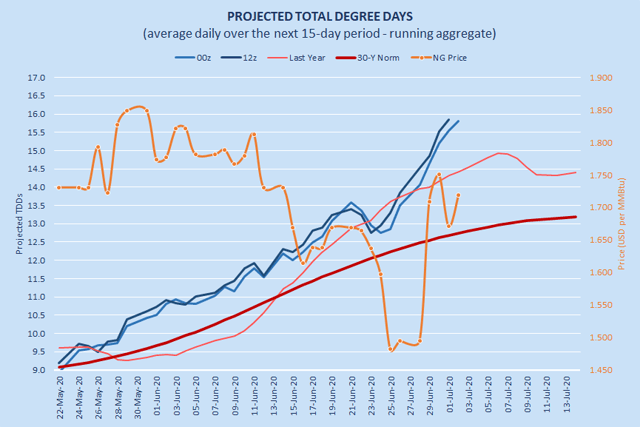

Projected TDDs are trending higher and remain above the norm (+24.0%) as well as above last year's level (+9.5%). Consumption is projected to increase by 5.3% over the next seven days.

-

Today, the fundamental signals are mixed. On the one hand, the weather factor is very bullish, but LNG feedgas flows are at multi-month low and dry gas production remains surprisingly strong.

-

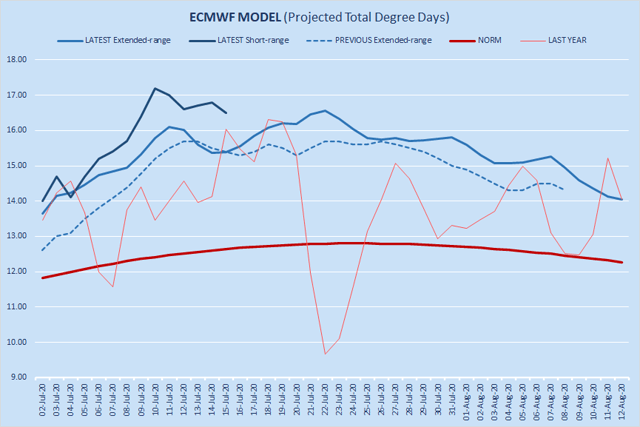

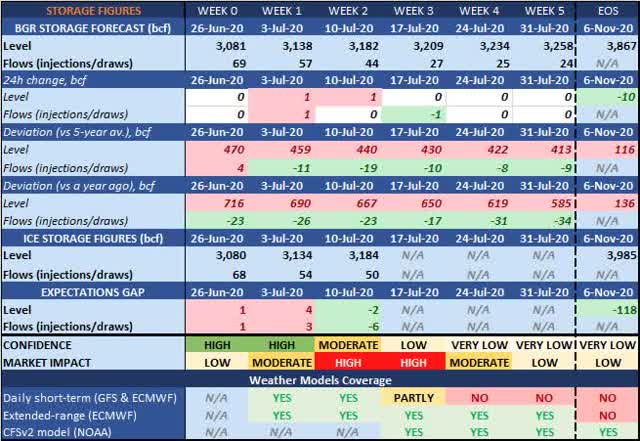

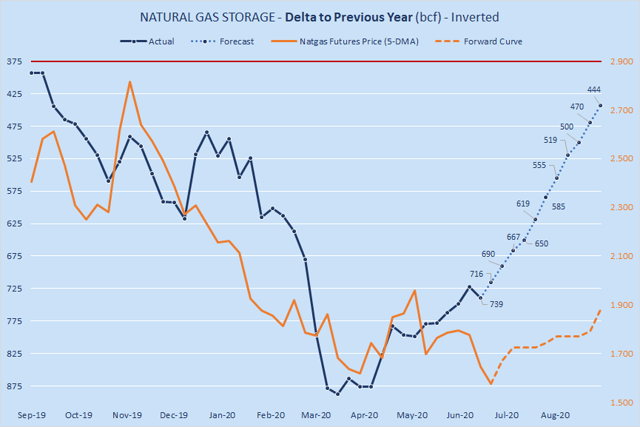

Natural gas consumption is projected to reach a "seasonal high" on July 15. Annual storage "surplus" is projected to shrink by -131 bcf by July 31. Our projection for today’s report is below market consensus.

-

In the short-term, the bears are in control. As long as the price remains below 1.695, the short-term trading bias will remain bearish.

TRADING VIEW

Exposure

-

We currently have no active positions in progress;

-

We are planning to re-enter the market in July or August.

-

In the short-term, the bears are in control.

-

As long as the price remains below 1.695, the short-term trading bias will remain bearish.

-

Today, the fundamental signals are mixed. On the one hand, the weather factor is very bullish, but LNG feedgas flows are at multi-month low and dry gas production remains surprisingly strong.

-

A break below 1.695, could cause a fall into the 1.655-1.592 range.

-

A break above 1.734 could lead to a gain into the 1.760-1.800 range.

-

It makes sense to sell the rallies - particularly in the 1.800-1.860 range.

-

It makes sense to buy the dips – particularly, in the 1.630-1.590 range.

-

Fundamentally, however, the long-term trend is bullish because annual storage “surplus” is still projected to shrink.

Bullish factors

-

Projected TDDs are trending higher and remain above the norm (+24.0%) as well as above last year's level (+9.5%).

-

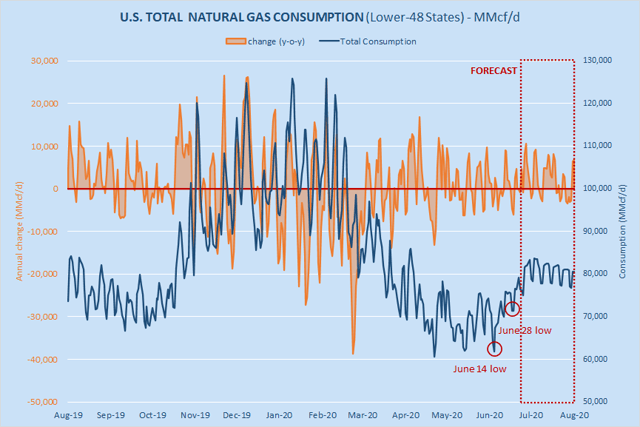

Natgas consumption (7-day average) is projected to increase by 5.3% over the next 7 days (from 75.4 bcf/d today to 79.4 bcf/d on July 9).

-

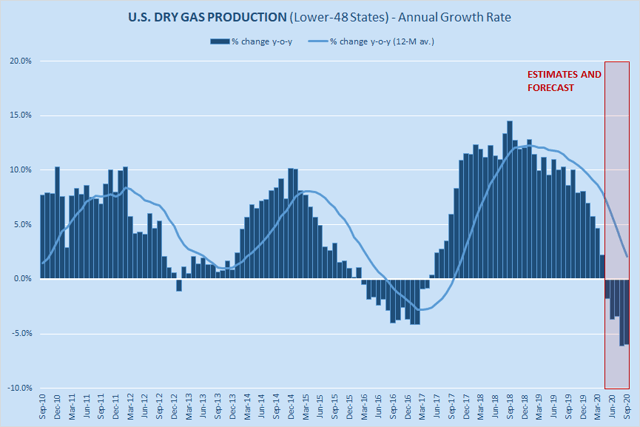

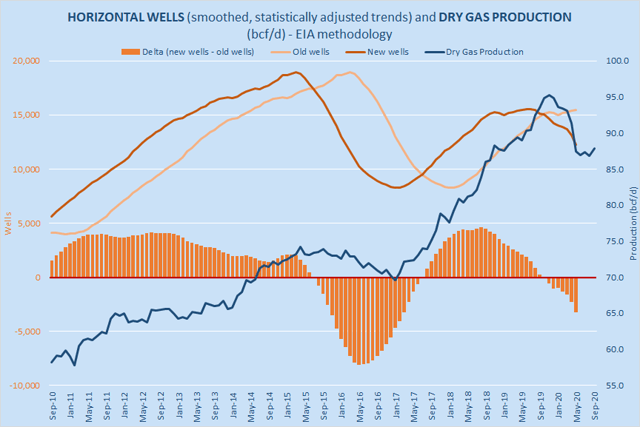

Natgas production growth potential has been severely damaged. Daily production rate is not expected to set a new all-time high for several years. EIA expects dry gas production to continue falling until March 2021. CAPEX remains depressed.

-

Annual storage "surplus" is projected to shrink by -131 bcf by July 31.

-

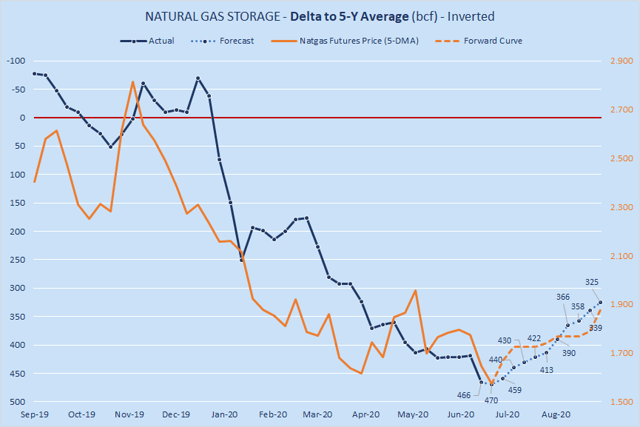

Storage "surplus" vs 5-year average is projected to shrink by -57 bcf by July 31.

-

EOS storage index is 118 bcf below market expectations.

-

Our projection for today’s report is below market consensus. We expect +69 bcf. Reuters survey: +78 bcf. However, other analysts - notably, Point Logic and Platts - expect larger builds: +73 bcf and +75 bcf, respectively. Still, their projections are also below average expectations.

-

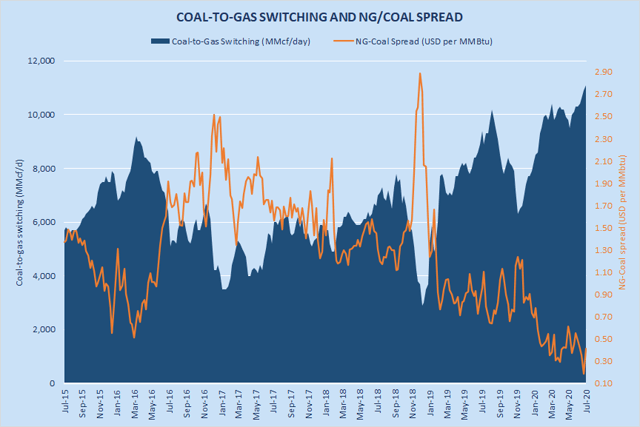

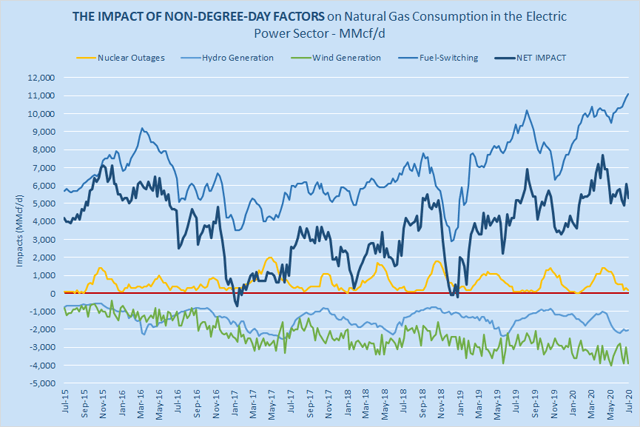

The net impact of non-degree-day factors is bullish (vs 2019) - primarily thanks to robust coal-to-gas switching. Electricity generation from renewable sources will be getting weaker from now on (until September) due to seasonal factors.

Bearish factors

-

COVID-19 cases are still rising - preventing the states from reopening.

-

Some producers began restoring output. Indeed, dry gas production is up +2.9 bcf/d from May 20 low.

-

LNG feedgas flows are down 2.3 bcf/d y-o-y and global LNG demand remains relatively weak so far. As of today, LNG feedgas flows remain at 3.3 bcf/d - the lowest level since April 2019.

-

Natural gas consumption is projected to reach a "seasonal high" on July 15.

-

Technically, natural gas July contract is trading within a descending wedge and is below key long-term moving averages. Technically, the long-term trading bias is still bearish.

-

In the short-term, the bears are in control. As long as the price remains below 1.695, the short-term trading bias will remain bearish.

-

Market's EOS storage expectations are ostensibly bearish (estimated at 3,980 bcf) and although we believe that these expectations are excessively bearish, the market does not care what our beliefs are.

Neutral factors

-

Weekly expectations gap for the next three reports is neutral.

TECHNICALS

August Contract >>

-

Support: 1.655, 1.631, 1.600-1.592, 1.550-1.546, 1.528, 1.517.

-

Resistance: 1.695-1.700, 1.734, 1.750, 1.761, 1.784, 1.798-1.800.

MARKET DATA (CHARTS AND TABLES)

SD Balance

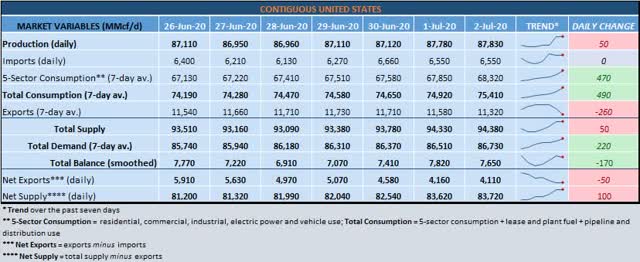

Latest Figures (daily)

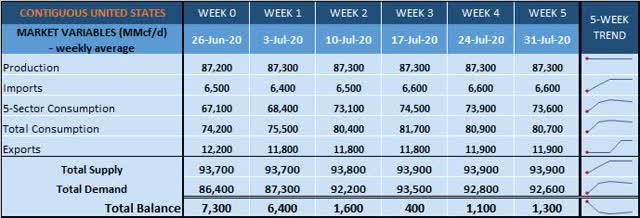

Forecast (weekly)

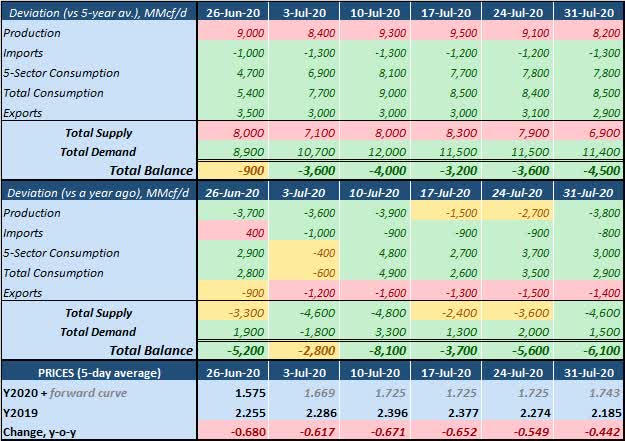

Forecast Deviations (weekly)

DEMAND

WEATHER

GFS Model (raw TDDs)

ECMWF Model (raw TDDs)

Projected TDDs: GFS vs ECMWF

ECMWF Model: long-range vs short-range (raw TDDs)

Projected TDDs (hybrid; running aggregate)

This chart DOES NOT show "historical actuals". This chart shows "historical forecasts".

Consumption

Natgas consumption (7-day average) is projected to increase by 5.3% over the next 7 days (from 75.4 bcf/d today to 79.4 bcf/d on July 9).

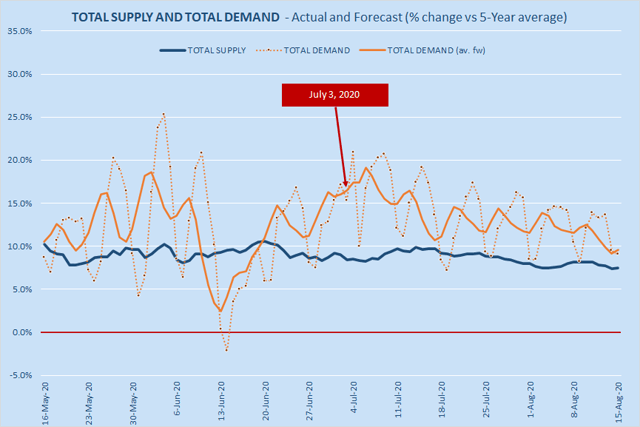

In relative terms, total demand is projected to remain mostly above the total supply curve until August 15 (at least).

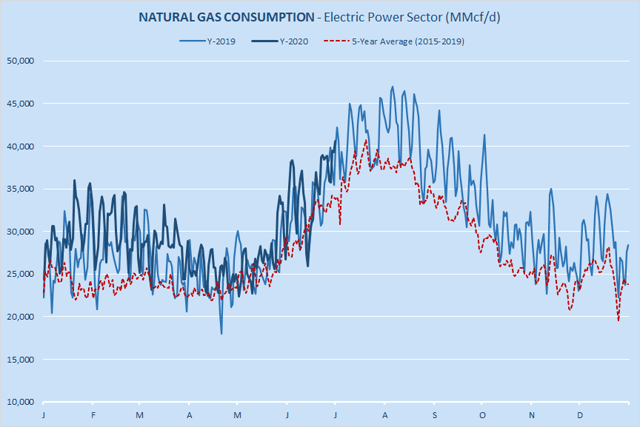

Consumption in the Electric Power sector is within last year's level (the data is derived directly from the "continuous emissions monitoring systems").

Coal-to-gas switching remains strong: 11.1 bcf/d, +1.7 bcf/d vs 2019. The net impact of four non-degree-day factors on natural gas consumption in the Electric Power sector is +5.3 bcf/d (+0.1 bcf/d y-o-y).

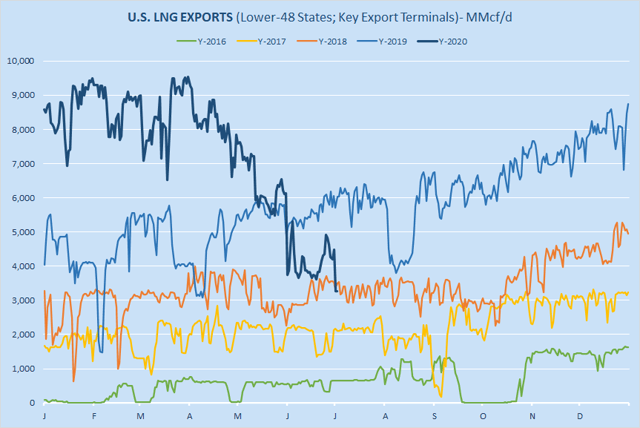

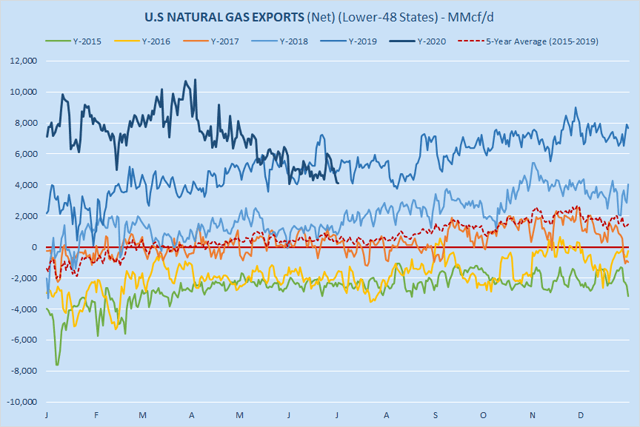

Exports

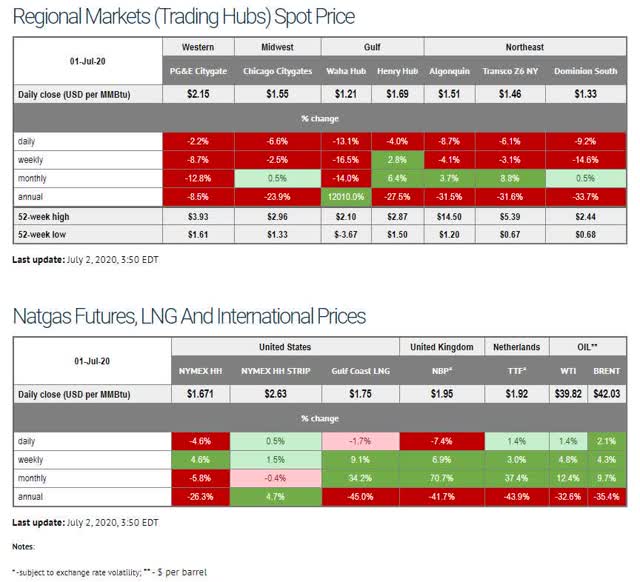

LNG feedgas flows are at 3.3 bcf/d - the lowest level since April 2019.

Net exports (calculated as imports minus exports) are currently estimated at 4.1 bcf/d (-0.8 bcf/d y-o-y).

SUPPLY

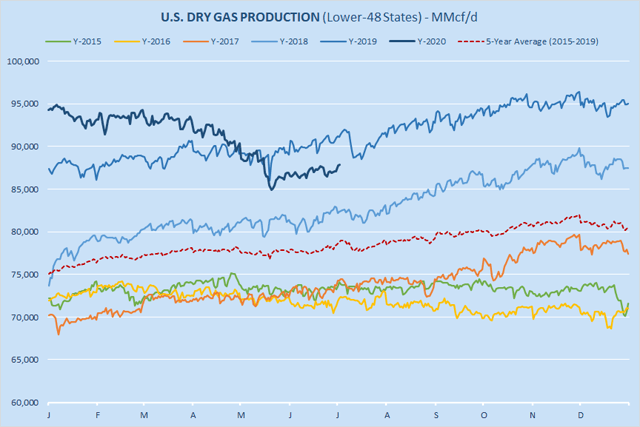

Production

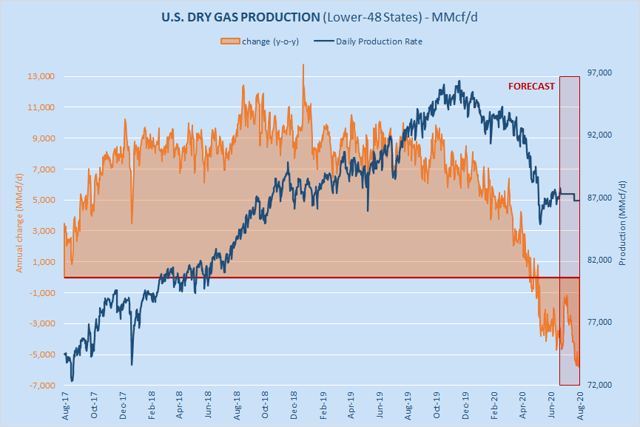

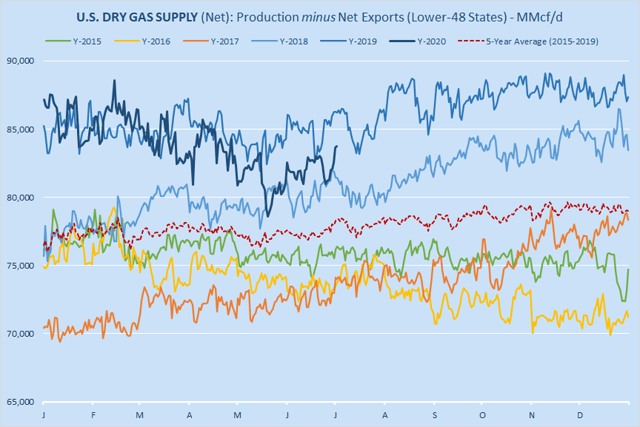

Latest dry gas production estimate (for contiguous United States): 87.8 bcf/d.

-

-8.6 bcf/d from an all-time high;

-

+1.5 bcf/d from a 3-week low;

-

+0.05 bcf/d from Wednesday's results.

We currently expect dry gas production in contiguous United States to average 87.3 bcf/d over the next three months (July-August-September). Annual growth rate is projected to be negative.

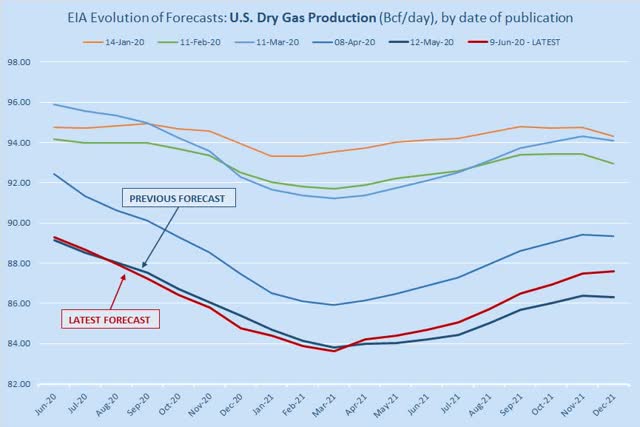

EIA has revised higher its U.S. dry gas production forecast by +0.24 bcf/d (on average). EIA currently expects dry gas production to average 86.03 bcf/d over the next 19 months (June 2020 - December 2021). EIA still projects that U.S. dry gas production will continue to decrease until March 2021.

Net supply (calculated as dry gas production minus net exports) is currently estimated at 83.7 bcf/d, 2.5 bcf/d below last year's level.

STORAGE

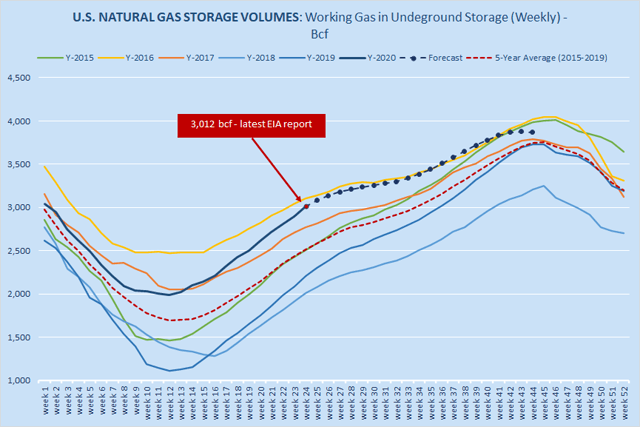

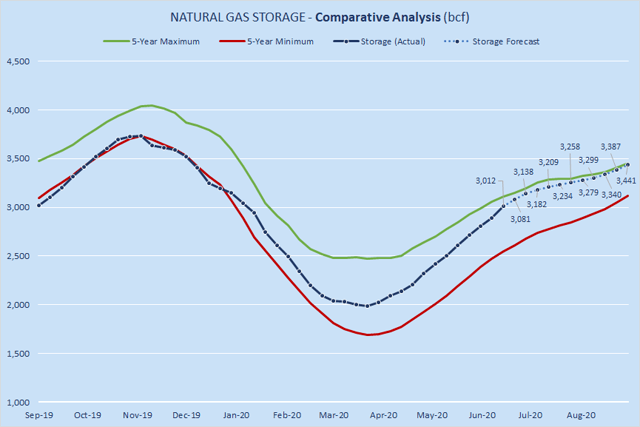

Our storage level outlook remained relatively unchanged (vs Wednesday's results). Currently, EOS storage index is at 3,867 bcf (118 bcf below market expectations).

Our EOS storage index is below market expectations, but the index is very unstable due to its long-term nature.

Weekly "expectations gap" for the next three reports is neutral.

Annual storage "surplus" is projected to shrink by -131 bcf by July 31.

Storage "surplus" vs 5-year average is projected to shrink (by -57 bcf over the same period).

Next Six Reports and EOS

Indices

Charts

Deviations

PRICES

Average spot price (latest survey across seven locations): $1.56 per MMBtu. HH spot was at $1.69 per MMBtu.

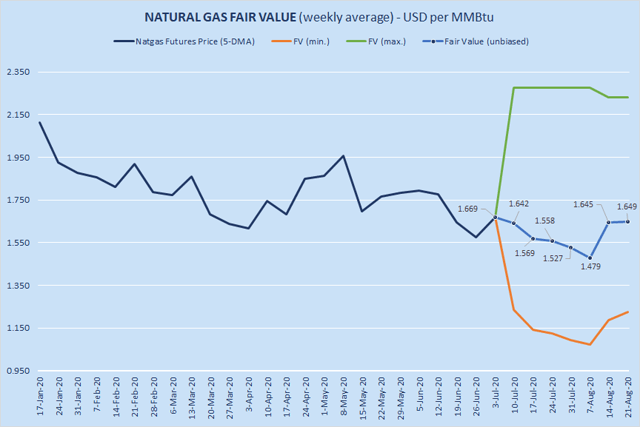

FAIR VALUE

"Fair value" – a rational and unbiased estimate of the potential market price of natural gas. It is totally hypothetical in nature and is derived entirely from historical observations over a certain time period. FV is a statistical experiment, not a fundamental indicator. FV can deviate substantially from the market price.

Forecasting the price of natural gas is exceptionally difficult, especially in the long run. The purpose of the “fair value” model is not to provide an exact price projection, but rather to show a theoretical trend potential based on fundamentals. It is equally important to remember that market is forward-looking and near-term price level can be determined by price expectations several weeks from now.

Extreme sentiment (which is quite common in natgas market) can easily drive the price below or above the "fair value". Overall, the concept of a "fair value" - even if it is econometrically sound - may not be particularly useful in trading.

Disclosure: No open positions. We are planning to re-enter the market in July or August.