Image Source: Pixabay

The mid-tier and junior gold miners in this sector’s sweet spot for upside potential just finished reporting a spectacular record quarter! All-time-high gold prices combined with relatively-contained costs catapulted unit earnings to another epic record. Those incredibly-rich profits leave mid-tiers even more undervalued relative to prevailing gold prices, portending massive catch-up rallying coming in this high-flying sector.

The leading mid-tier-gold-stock benchmark is the GDXJ VanEck Junior Gold Miners ETF. With $5.1b in net assets mid-week, it remains the second-largest gold-stock ETF after its big brother GDX. That is dominated by far-larger major gold miners, though there is much overlap between these ETFs’ holdings. Still misleadingly named, GDXJ is overwhelmingly a mid-tier gold-stock ETF with juniors having little weighting.

Gold-stock tiers are defined by miners’ annual production rates in ounces of gold. Small juniors have little sub-300k outputs, medium mid-tiers run 300k to 1,000k, large majors yield over 1,000k, and huge super-majors operate at vast scales exceeding 2,000k. Translated into quarterly terms, these thresholds shake out under 75k, 75k to 250k, 250k+, and 500k+. Today only one of GDXJ’s 25 biggest holdings is a true junior!

Its Q3 output is highlighted in blue in the table below. Juniors not only mine less than 75k ounces per quarter, but their gold output generates over half their quarterly revenues. That excludes streaming and royalty companies that purchase future gold output for big upfront payments used to finance mine-builds, and primary silver miners producing byproduct gold. But mid-tiers often make better investments than juniors.

These gold miners dominating GDXJ offer a unique mix of sizable diversified production, excellent output-growth potential, and smaller market capitalizations ideal for outsized gains. Mid-tiers are less risky than juniors, while amplifying gold uplegs more than majors. So we’ve long specialized in the fundamentally-superior mid-tiers and juniors at Zeal, actively trading these smaller gold miners for a quarter-century now.

With gold blasting higher, this year’s pickings have been good. Our recent realized gains triggered by gold’s overdue and healthy pullback have run as high as +158%!We just started reloading our newsletter trading books this week, adding five fantastic mid-tiers and juniors with imminent big production growth from expansions and mine-builds. GDXJ itself has soared 79.5% higher at best over this past year, big gains!

Yet even they are small compared to historical precedent, really lagging gold. Its monster upleg since early October 2023 has rocketed up 53.1% at best!Before big gold uplegs give up their ghosts, the better mid-tiers and juniors often see their stock prices triple or quadruple. So the best gains in the cream-of-the-crop smaller gold miners are still ahead. Their latest quarterly fundamentals support way-higher stock prices.

For 34 quarters in a row now, I’ve painstakingly analyzed the latest operational and financial results from GDXJ’s 25-largest component stocks. Mostly mid-tiers, they now account for 65.4% of this ETF’s total weighting. While digging through quarterlies is a ton of work, understanding smaller gold miners’ latest fundamentals really cuts through the obscuring sentiment fogs shrouding this sector. This research is essential.

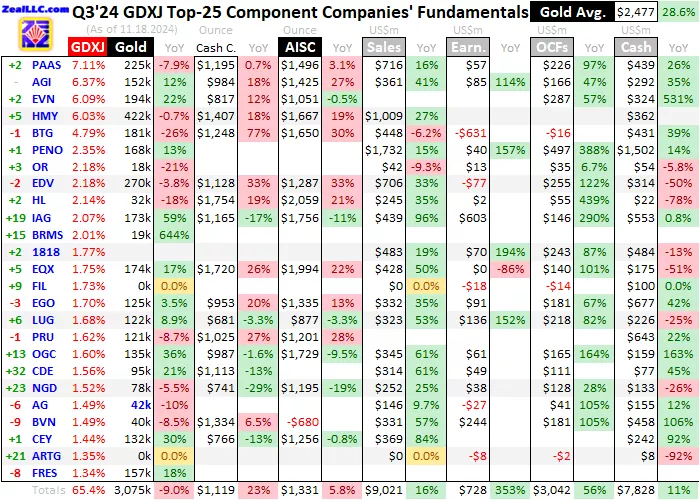

This table summarizes the GDXJ top 25’s operational and financial highlights during Q3’24. These gold miners’ stock symbols aren’t all US listings, and are preceded by their rankings changes within GDXJ over this past year. The shuffling in their ETF weightings reflects shifting market caps, which reveal both outperformers and underperformers since Q3’23. Those symbols are followed by their recent GDXJ weightings.

Next comes these gold miners’ Q3’24 production in ounces, along with their year-over-year changes from the comparable Q3’23. Output is the lifeblood of this industry, with investors generally prizing production growth above everything else. After are the costs of wresting that gold from the bowels of the earth in per-ounce terms, both cash costs and all-in sustaining costs. The latter help illuminate miners’ profitability.

That’s followed by a bunch of hard accounting data reported to securities regulators, quarterly revenues, earnings, operating cash flows, and resulting cash treasuries. Blank data fields mean companies hadn’t disclosed that particular data as of the middle of this week. The annual changes aren’t included if they would be misleading, like comparing negative numbers or data shifting from positive to negative or vice-versa.

Back in mid-October before gold miners started reporting Q3 results, I wrote an essay predicting they’d achieve an epic record quarter. That indeed proved correct, with smaller gold miners well-outperforming their larger major peers. Yet despite practically printing money at these lofty gold prices, the smaller gold miners still remain largely-unknown. That should change soon with the huge numbers they are putting up!

These fundamentally-superior smaller miners’ phenomenal Q3 performances trounced those of the major-dominated GDX top 25 I analyzed in depth in last week’s essay. The mid-tiers and juniors’ epic quarter is easier to understand compared to the majors’ still-mostly-great results. That contrast begins with gold miners’ Q3 production. The GDXJ top 25’s collective output sure looks weak, falling 9.0% YoY to 3,075k ounces.

That’s much worse than the GDX top 25’s only slumping 1.4% YoY to 8,491k in Q3. And both shrinkage rates fell way behind global gold mining output according to the World Gold Council. It publishes the best-available worldwide gold fundamental data, which showed total global production actually surged an impressive 5.8% YoY to 31,824k ounces in Q3’24! But GDXJ’s shrinking output is a composition thing.

As this table shows, there’s lots of shuffling among GDXJ’s top component stocks. This ETF’s managers periodically add or remove components for various reasons. A year ago in Q3’23, the heaviest-weighted stock in this mid-tier gold-stock ETF was super-major Kinross Gold. While one of the best larger gold miners with a higher weighting in GDX too, KGC was far too big to include in GDXJ. So it was finally booted.

If KGC’s colossal 585k ounces mined in Q3’23 is replaced with the 26th-largest GDXJ component then, the GDXJ top 25’s aggregate production actually surged 10.0% YoY in Q3’24! That is wildly better than the GDX top 25’s lagging 1.4%-YoY shrinkage. Unlike majors often struggling to overcome depletion, the mid-tiers and juniors are firing on all cylinders on the output front. And this is nothing new for smaller miners.

Even with no adjustments like KGC, the GDXJ top 25’s production has grown through eight of the last ten quarters!Meanwhile the GDX top 25’s only grew in three of those. Production growth is the primary mission of gold miners, trumping everything else. Higher outputs boost operating cash flows which help fund mine expansions, builds, and purchases. That fuels stock-price-lifting virtuous circles of growth.

While great growth stories are rare in majors, they abound in mid-tiers and juniors driving big stock-price gains. Case-in-point is the GDXJ top 25’s fastest climber into its upper ranks since Q3’23, IAMGOLD. This larger mid-tier operates three gold mines in Ontario, Burkina Faso, and Quebec. Its flagship one is brand-new, recently achieving commercial production in early August. That mine is truly company-changing.

IAG’s 70% stake in it is expected to average 347k ounces annually over its initial six years of operations, and 256k across its long 18-year life!That’s big growth on top of IAMGOLD’s older pair of mines, which are expected to yield around 540k ounces in 2024. Even better, this new mine is super-profitable with all-in sustaining costs forecast to average just $854 over its entire lifespan!That’ll greatly improve IAG’s fundamentals.

Its two older mines are guided to higher AISCs around $1,700 this year. But that new mine’s fantastic low AISCs mixed in will really drag down the overall average, really boosting IAG’s future earnings. We just added five new trades with similar and some better growth stories than IAMGOLD’s. And there are more to come, as the best smaller gold miners excel at consistently bringing more lower-cost production online.

Great mid-tier and junior growth plays are often analyzed in our popular newsletters, enabling subscribers generously keeping us in business to buy in earlier and lower. With such amazing opportunities and big gains among smaller gold miners, why bother with GDX which is retarded by deadweight majors?While GDXJ is way better, even its upper ranks are saddled with plenty of gold stocks that chronically underperform.

There’s actually considerable overlap between GDXJ and GDX. Fully 14 of these GDXJ-top-25 stocks are also GDX-top-25 ones!GDXJ effectively lops off the 11 largest GDX stocks, the world’s biggest gold miners which mostly drag down sector performance. Then GDXJ weights the common components heavier. These GDXJ-top-25 stocks in GDX only have a 23.1% weighting, which GDXJ nearly triples to 65.4%!

Unit gold-mining costs are generally inversely proportional to gold-production levels. That’s because gold mines’ total operating costs are largely fixed during pre-construction planning stages, when designed through puts are determined for plants processing gold-bearing ores. Their nameplate capacities don’t change quarter to quarter, requiring similar levels of infrastructure, equipment, and employees to keep running.

So the only real variable driving quarterly gold production is the ore grades fed into these plants. Those vary widely even within individual gold deposits. Richer ores yield more ounces to spread mining’s big fixed expenses across, lowering unit costs and boosting profitability. But while fixed costs are the lion’s share of gold mining, there are also sizable variable costs. That’s where recent years’ raging inflation hit hard.

Cash costs are the classic measure of gold-mining costs, including all cash expenses necessary to mine each ounce of gold. But they are misleading as a true cost measure, excluding the big capital needed to explore for gold deposits and build mines. So cash costs are best viewed as survivability acid-test levels for smaller gold miners. They illuminate the minimum gold prices necessary to keep the mines running.

The GDXJ top 25’s average cash costs soared 23.2% YoY to a record $1,119 per ounce in Q3’24! While not ideal, that’s better than the GDX majors. Despite their touted economies of scale, their cash costs last quarter surged 19.2% YoY to a higher $1,142. The GDXJ top 25 have reported declining cash costs in four of the last ten quarters, compared to one for the GDX top 25. And cash costs remain way under gold.

All-in sustaining costs are far superior than cash costs, and were introduced by the World Gold Council in June 2013. They add on to cash costs everything else that is necessary to maintain and replenish gold-mining operations at current output tempos. AISCs give a much-better understanding of what it really costs to maintain gold mines as ongoing concerns, and reveal the mid-tier gold miners’ true operating profitability.

The GDXJ top 25’s AISCs last quarter also rose 5.8% YoY to $1,331 per ounce. That was actually the first quarter in six they climbed, and even those remained way under the GDXJ-top-25 record of $1,442 in Q4’22. Incredibly the mid-tiers and juniors held the line on mining costs much better than the supposedly-superior GDX majors!The GDX top 25’s average AISCs surged 8.0% YoY in Q3’24 to a higher record $1,431.

You read that right, the smaller gold miners are producing their metal $100-per-ounce cheaper than the larger ones! Bigger is not necessarily better in gold stocks, which most traders don’t understand. The GDXJ top 25’s AISCs declined in five of the last ten quarters, compared to three for the GDX top 25’s. Interestingly both leading gold-stock ETFs’ AISCs were skewed lower in Q3 by an extraordinary outlier.

Included in the upper ranks of both ETFs, Peru’s Buenaventura actually reported negative $680 AISCs last quarter!That sorcery is righteous, driven by massive byproduct credits more than offsetting gold’s mining costs. Last quarter BVN’s gold output slumped 8.5% YoY to 39.7k ounces. But thanks to a big revamped silver, zinc, and lead mine ramping up, those outputs skyrocketed 187%, 177%, and 287% YoY!

Buenaventura is no longer a primary gold miner, with only 29.7% of Q3’24 revenues driven by gold. Silver was responsible for another 37.6%. But probably because gold miners command higher multiples in markets than other metals, BVN and plenty of other poly-metallic miners report in gold-centric terms. Buenaventura’s high base-metals production will continue for many years, contributing to super-low AISCs.

In the 34 quarters I’ve been advancing this research thread, I’ve never excluded high-cost outliers from GDXJ-top-25 AISC averages. While I pointed them out, they remained in the calculations. So BVN’s byproduct-credit-fueled low ones also have to stay in for consistency. Again this doesn’t affect GDXJ-versus-GDX comparisons, since BVN is a top-25 component in both. Negative AISCs are rare, but not unique.

The best proxy for gold-miner earnings as a sector subtracts quarterly-average AISCs from quarterly-average gold prices. Last quarter proved monumental for the yellow metal, which averaged a dazzling record $2,477 which rocketed up 28.6% YoY! That less the GDXJ top 25’s $1,331 AISCs made for the most-profitable quarter ever for gold miners, implying epic profits running way up at $1,146 per ounce!

Those skyrocketed a colossal 71.4% YoY, and easily bested the GDX top 25’s $1,046 last quarter!Utterly-massive unit-earnings growth is nothing new for these high-flying smaller gold miners. Over the last six quarters, GDXJ-top-25 per-ounce profits have soared 34%, 106%, 126%, 63%, 66%, and 71% YoY!No other sector in all the stock markets comes anywhere close to that kind of performance, it is mind-boggling.

And this off-the-charts earnings growth isn’t finished. We’re about halfway through Q4, and so far gold is averaging a much-higher record $2,675!For conservatism’s sake let’s assume that gets dragged down to $2,600, which would require gold to average just $2,525 until year-end. In 2024’s first three quarters, the GDXJ top 25’s AISCs averaged just $1,289. But let’s assume they climb again from Q3’s heights to hit $1,350.

Even that implies this current quarter ought to see smaller gold miners earn an amazing record $1,250 per ounce!That would make for another quarter of 92%-YoY unit-profits growth. And odds are this quarter’s average gold price will shake out considerably higher than that lowballed estimate. With fundamentals like this, speculators and investors should be kicking down the doors to flood into mid-tiers and juniors.

But they haven’t yet, which is why fundamentally-superior smaller gold stocks are likely to double, triple, or more from current levels. Mid-week GDXJ was trading under $48 per share. That’s where it was in mid-2020, when gold was only around $1,800 and GDXJ-top-25 unit earnings were closer to $750!Like all stocks, sooner or later gold-stock prices need to revalue to reflect this sector’s vastly-better fundamentals.

Because GDXJ’s managers have added and removed super-majors over the years, its hard accounting results reported to securities regulators aren’t consistent. Last quarter the GDXJ top 25’s total revenues surged 16.2% YoY to $9,021m, even though Kinross Gold was included in Q3’23. Removing KGC from that comparable quarter and subbing in the 26th-biggest component, that revenue growth soared to 35.4%.

But the GDXJ-top-25 record was $9,328m way back in Q4’19, when GDXJ was stuffed with two super-majors and four other large majors that should’ve been exclusive to GDX!Adjust for that, and the GDXJ top 25’s sales last quarter were a major new record. The bottom-line earnings under Generally Accepted Accounting Principles or other countries’ equivalents were similarly distorted by composition changes.

The GDXJ top 25’s still skyrocketed a stunning 353.3% higher YoY to $728m!But that fell well short of the major-skewed Q4’20 record of $1,547m. If GDXJ was properly limited to a handful of small majors but mostly mid-tiers and juniors, Q3’24’s earnings would’ve also been a major record high like those unit profits. Like usual some of these mid-tiers did flush big unusual non-cash items through income statements.

I track those to compare adjusted earnings, but they were mostly a wash in Q3’24. For example B2Gold ran through a huge $661m impairment charge on a mine-build due to higher construction costs. I think that was overdone though, as BTG assumed just $1,900 gold going forward. That was offset by a $462m impairment-reversal gain at IAG due to higher gold prices, and a $210m gain at BVN for selling a company.

Netting all those out, GDXJ-top-25 adjusted earnings barely budged at $723m last quarter. Those fat-and-rich bottom-line profits forced gold-stock valuations even lower, leaving plenty of crazy bargains. Some of these elite mid-tiers and juniors are now trading at absurdly-cheap single-digit trailing-twelve-month price-to-earnings ratios!Those phenomenal fundamentals will attract even value investors eventually.

The GDXJ top 25’s cash flows generated from operations soared 55.9% YoY to $3,042m last quarter. That too would be a record if not for 2020’s anomalous major-dominated quarters. Still that was close to their distorted peak of $3,580m in Q3’20. All that cashflow pushed the mid-tiers’ treasuries up 11.1% YoY to $7,828m. That’s lots of money available to expand existing mines and build new ones to keep growing outputs.

With gold powering to many new record highs this year and smaller gold miners earning money hand-over-fist, gold stocks remain seriously undervalued relative to these lofty prevailing gold levels. This makes for an exceptionally-bullish setup for massive gains ahead!Sooner or later gold-stock sentiment will reach a psychological tipping point, where traders increasingly rush in to chase their mounting gains.

The bottom line is smaller gold miners just reported epic record quarterly results. Gold’s dazzling all-time-high prices were the main driver, but mid-tiers and juniors way outperformed the majors in containing costs. Together that fueled the fattest-and-richest profits ever earned by gold miners!That was the sixth consecutive quarter of colossal unit-earnings growth for smaller gold stocks, unparalleled in all of stock markets.

That forced gold-stock prices to even-more-seriously-undervalued levels relative to gold. Sooner or later traders will figure that out, and flood in greatly amplifying gold-stock gains. That overdue fundamentally-righteous sentiment shift should catapult fundamentally-superior smaller gold miners’ stocks wildly higher. We are talking doublings, triplings, or even more, so traders need to do their homework and get deployed.

More By This Author:

Gold Miners’ Q3’24 Fundamentals

Big U.S. Stocks’ Q3’24 Fundamentals

Gold Stocks’ Winter Rally ‘24

Comments

Log in or sign up to join the conversation.