Aluminium: Still Standing, For Now

Despite poor demand prospects and rising supply, aluminum is standing its ground. The bearishness rooted in its fundamentals will continue to weigh on the medium-term outlook, but this may not lead to a bear trend anytime soon amid an asymmetric recovery path following Covid-19.

Source: Shutterstock

1. 'V' or 'U'? depending on which market you are looking at

Aluminum recovered during the second half of 2Q20 in defiance of surging inventories (LME) and a widely expected market surplus. Compared to some of its peers in the industrial metals complex, aluminum's recent recovery path looks to be more U-shaped. Having spent a month carving out a bottom, LME aluminum was initially reluctant to follow its peer on the ShFE, which has seen more of a V-shaped rally. We have discussed the market decoupling and recent convergence, and their background dynamics in previous notes.

In the second half of the year, aluminum shares the same macro background as copper, including negative dollar themes and US election-related trade rhetoric growing louder. Aluminum has always been at the forefront of trade friction, and the light metal (premium) was recently caught in the crossfire of US tariff threats on Canadian aluminum exports. We also continue to see risks of a more difficult environment for world aluminum trade in other markets such as the EU and China.

A surplus market continues to be supported by weak demand prospects and rising production, and more alarmingly, we are anticipating another 1.8 million of capacity in the pipeline to come online during the remainder of the year. Thus, it's hard to be optimistic towards this metal. However, in the meantime, and while this may sound strange, it's equally hard to call for a broad bear trend in the short-term.

2. To bet against demand, not an easy thing…for now

The asymmetric recovery path following Covid-19 around the globe has caused some confusion in the London aluminum market. Though different market dynamics are sometimes affected by trade, London and Shanghai market prices influence each other. London aluminum has been anchored around US$1,600 for a while since late May. Some themes are playing underneath to fend off the bears, and aluminum could end up caught in a range-bound market in the short term.

- Ex-China: As aluminum consuming countries are still sticking to reopening plans, optimism about pent-up demand could outweigh concerns about any surpluses. Also, note how much is readily available for purchase when stocks that have been locked away for financing purposes are stripped out.

- China: It is not clear how much pent-up demand there will be in China after Covid-19, or whether such demand would be sustainable in the short term.

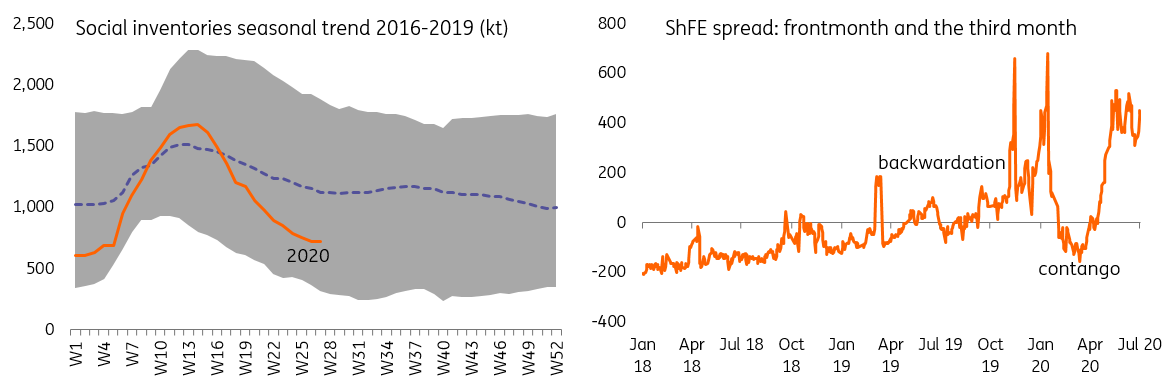

- In the ingot market, continuous destocking has reinforced this view. In particular: a) ShFE is still in backwardation and the physical is at a premium. b) the market hasn't sorted out scrap supply completely, and it's been importing an increasing volume of alloys and ingots so far this year, which will continue to add to apparent demand. c) housing construction is still pointing to a recovery in terms of completions and there is hope for stronger demand, along with better copper demand in China. Sales in some consumer products and car sales have been holding up well, perhaps suggesting that pent-up demand has not yet dried up.

Fig 1. Falling inventories and tight spreads

Source: Bloomberg, ING

Meanwhile, the market continues to expect an even looser liquidity environment and fiscal stimulus packages to kick in over the coming months. For the rest of the year, we generally see prices, in average terms, gravitating lower from the current level towards US$1570/t, but spikes towards US$1,650 are likely.

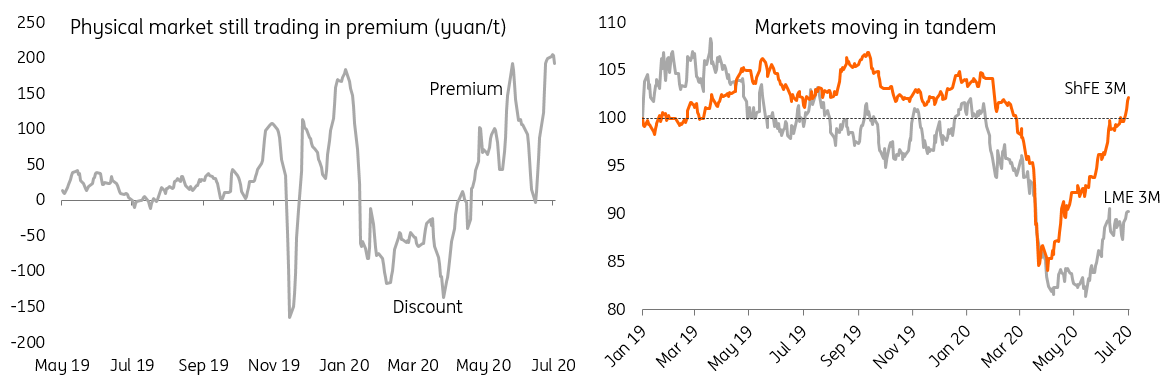

Fig 2. China physical still implies tightness

Source: Bloomberg, ING

3. Potential themes to unfold in 2H20

Some market themes could potentially unfold in either direction this year, throwing a curveball to the price path and giving both bulls and bears something to latch onto.

- China apparent stays elevated (positive) - whether be it backed by arb-driven imports or commercial stockpiling domestically.

- Exports of semis products fall more deeply (bearish) - A further slide in aluminum semis exports coming alongside a drop in exports of other aluminum products, could weigh heavily on China consumption.

- Cost inflation (neutral)- So far, risks on this front look rather moderate. With recent disruptions (Hydro Alunorte/Shanxi Huaxing), and Chalco's announcement yesterday that it would implement so-called 'flexible production' at its three alumina refiners in Shanxi province (possibly affecting 1.8mn tonnes of capacity) things are worth monitoring in the short-term, particularly in light of further aluminum smelting capacity coming online.

- Finally, Covid-19 remains the largest uncertainty.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more