AgMaster Report - Wednesday, Dec. 23

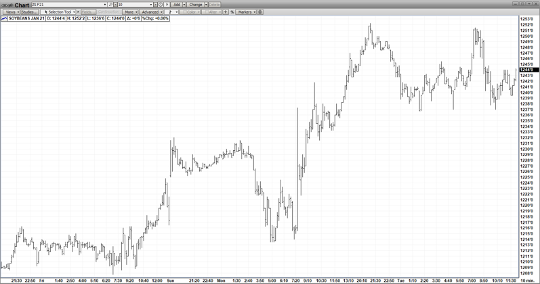

JAN BEANS

A COVID mutation was discovered in England – sparking a panic sell-off in the financials as traders feared another pandemic! But the row crops showed their resilience – bouncing back from early double-digit losses to post new contract highs! Adding to already stout supply-demand fundamentals were the ongoing Argentina dock strike & the upcoming Russian export tax! All of this has elevated Jan Beans to plus $12 heights & six-year highs on the monthly charts! The El Nina pattern that has ravaged S/A has centered in Argentina & South Brazil! This means their production will be late & less – both very advantageous to the US! Stocks are already on 6 yr lows! What if it turns dry during planting?

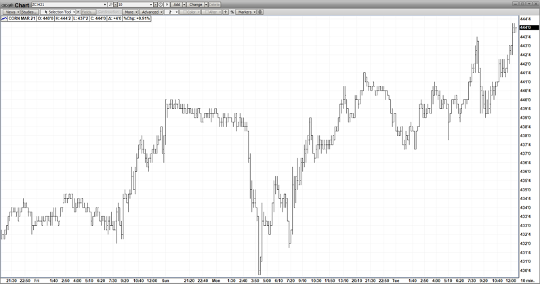

MAR CORN

Whereas beans are clearly the upside leader, Mar Corn has been no slouch – posting new contract highs on Monday! One thing holding corn back is much-diminished ethanol demand as Covid has dramatically reduced driving! But today’s passage of the relief package will provide financial aid to the ethanol industry – part of an overall $13 billion legislation – which should help bridge the gap between Covid & widespread vaccination in 2021! Plus, the simple fact that US Corn is the cheapest feedgrain anywhere – really enhances its exportability! Dryness in Argentina will hurt their corn crop & a falling dollar will really jump our exports! Finally Mar Corn Futures – even after their impressive rally – are still in the bottom 20% of their 10-year range ($3.00 – $8.00)! Corn stocks are on 5-year lows & dwindling under the pressure of massive exports! And to date, no “demand rationing” has occurred yet! In 2021, THERE IS NO MARGIN FOR ERROR!!

MAR WHEAT

The most momentous news to impact the wht mkt was Russia’s announcement last week that they would implement an export tax beginning on Feb 15 & extending thru the end of June! Since the move had been widely expected, the mkt reacted in a “buy-the-rumor/sell-the-fact fashion immediately selling off! The mindset was that the mkt was already overbought & that Russian exporters would flood the mkt wht before the 2/15 deadline! but after all the smoke cleared, export taxes are friendly for global wht prices – and will support the mkt! Also, help could come from very dry Plains condition – which may jeopardize our WW crop & from spill-over from our row crops – in the midst of an aggressive the bull move off of a S/A drought & stellar exports!

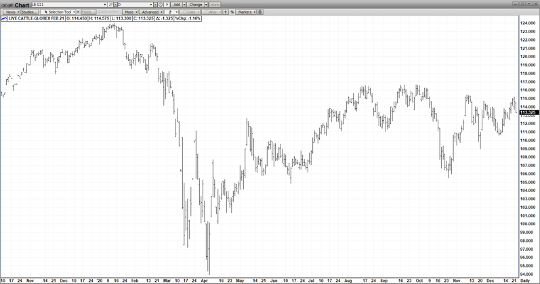

FEB CATTLE

Feb Cat ran into some formidable headwinds on its way to the top end of its recent trading range (109 -115) not the least of which was Covid-weakened demand! In addition, the mkt had to negotiate a large premium to cash, high average weights & generally ample supplies! However, we feel amped-up economic growth coming in early 2021 – coinciding with more widespread vaccination – will re-ignite beef demand – enabling the contract to break-out of the narrow price range on the upside!

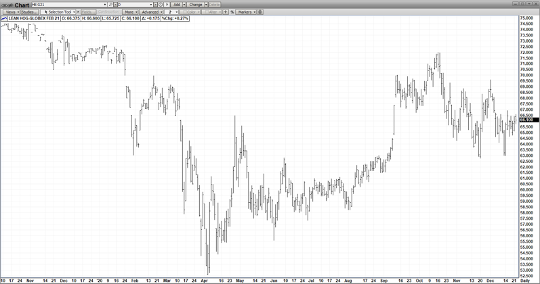

FEB HOGS

Feb Hogs – much like its sister mkt Feb Cat – has been range-bound (63-69) since early November – being pushed & pulled byCovid negativity & vaccine optimism! Now in this holiday-shortened week, the mkt awaits two USDA Reports – today's Cold Storage & Wed’s Quarterly Pig Crop – which together should give the mkt some direction into year-end! But a big uncertainty is to what degree Chinese pork imports will tail off in 2021?Hopefully, any drop-off in import demand with be more than offset by an increase in domestic pork consumption as the economy recovers in the 1st Quarter!