AgMaster Report - Tuesday, Dec. 29

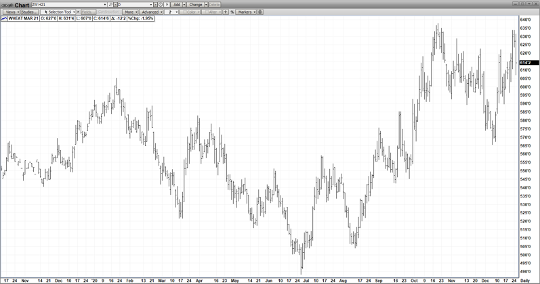

JAN BEANS

Wow! The end of 2020 & not soon enough! RIGHT? But the latter half of this year, the CBOT has been the beneficiary of two very powerful S/D fundamentals – an unrelenting La Nina savaging S/A crops & stellar export demand! And the macros have supported as well with record highs in the DJI & Nasdaq (what pandemic?), a deteriorating US Dollar & a resurgent Crude Oil mkt! So it’s not too surprising that Jan Beans corrected 35 cents interday after their $4.00 rally ($8.80-$12.80) since Mid-August with only 4 days left in the trade year! Also, the Argentine dock strike looks to be settled this week – finally, a plethora of exports this morning were either expected/below exp! Meanwhile, S/A’s reproductive period is now!!

MAR CORN

While beans & wheat slumped to double-digit losses – succumbing to year-end profit-taking & the imminent settlement of the Argentine Dock Strike, Mar corn STOOD TALL – gaining 6 cents & forging new highs for the move! The mkt is benefiting from positive fundamentals including extraordinary exports, worrisome supply concerns with the S/A drought, a weakening dollar & a soon-to-be strengthening economy! This has resulted in daily dwindling carry-over stocks – now pegged at 5-6 lows! Simply put, “ there’s much more going out the front door – than coming in the back”!And the long-suffering ethanol demand which Covid has decimated due to sharply lower driving – promises to make a big comeback in 2021 when the widespread vaccine dissemination fosters rapid economic growth! And what if the S/A dryness travels to the Northern Hemisphere! There is NO MARGIN FOR ERROR! But given all of this, corn is still historically cheap – still remaining in the lower 25% of a 10-year range! ($3 – $8)!

MAR WHEAT

Mar Wht has lost 30 cents in the past two trading days (635-605) as it corrected an overbought condition – after spillover strength from the bean/corn rally & the Argentine dock strike had rallied the mkt to its October highs! But the probable settlement of the strike this week promised resumed wht shipments out of Argentina & this deflated the mkt! Plus year-end settling-up & still record world stocks also weighed on the mkt! It will continue to coattail its sister mkts – corn & beans – as they have a stronger supply/demand scenario!

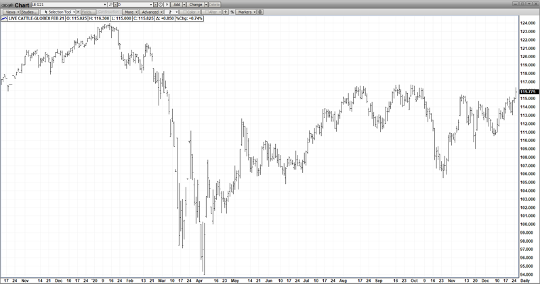

FEB CATTLE

Feb Cat demonstrated impressive stand-alone strength within the Meat Complex today soaring to its summer highs on the back of Covid vaccine optimism – with the general perception that that widespread vaccination into the 2nd Qtr of 2021 would encourage a re-opening of much of the economy! Also supportive was Trump’s signing of the relief package! There are some short-term hurdles to overcome between now & then but the mkt seems sanguine they will be resolved!

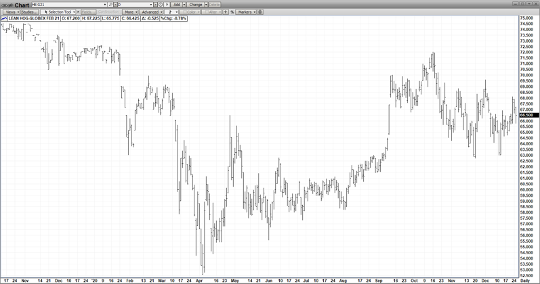

FEB HOGS

While Feb Cat challenged its contract highs today, Feb Hogs continued to languish in the middle of a two-month $6 range (63-69) bogged down by ample supplies, a disappointingly neutral Pig Crop Report last Wed & an anticipated slow-down in Pork imports by China in 2021! The mkt should receive a much-needed boost from a rejuvenated economy in the 1st/2nd QTR of 2021!