Ag Master Report - Wednesday, Sept. 23

NOV BEANS

(Click on image to enlarge)

Nov Beans were long overdue for a significant correction after a nearly vertical $1.80 ascent (8.65 – 10.45) since the August WADSE Report -and it came today – prompted by an extreme overbought condition, a bloated long OI, negative macro mkts, and open weather conducive to harvest! Nonetheless, rampant China buying continued today for the 10th day in a row! Their insatiable appetite for our grains is caused by excessive flooding in their farm areas, the re-building of their hog herds & their desire to rebuild their stockpiles! And South America supplies are tight! So its CHINA VS HARVEST! And China is winning! Also despite the sharp rally, beans are still historically cheap!

DEC CORN

(Click on image to enlarge)

Dec Corn – along with Nov Beans – was also ripe for a correction after a nearly uninterrupted 60 cent upmove (320-380). With the DJI down over 500 points, crude oil off $2.00 & the dollar up sharply, and harvest already 8% complete, the mkt finally succumbed to its overbought condition! Should yields fall under 176 BPA, then stocks could fall under 2BB – the lowest in four years! We feel China buying will outlast harvest!

DEC WHEAT

(Click on image to enlarge)

Yesterday, Dec Wht got bludgeoned along with many commodities by the negative Macro mkts – the DJI was down over 500 points, the US Dollar was up 70 points & crude oil was down $1-2 dollars! KC Wht had a sweeping downside reversal as well! But today due to dryness in the plains & South America plus a tender from Egypt, the mkt recovered! Winter Wheat is 20% planted (avg-20) & Spring Wht is 96% harvested! A “rising tide floats all boats” so continued China buying of US corn & beans will spillover to wht!

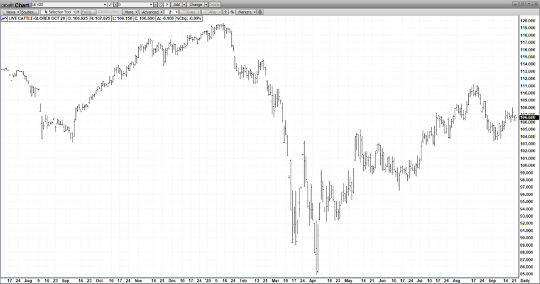

OCT CATTLE

(Click on image to enlarge)

Today is a stark reminder of the relative strength of the cattle & hog complexes – yesterday all commodities got nailed by the bearish onslaught that was very bearish Macro Mkts! But today in Turnaround Tuesday action, Oct Hogs are sharply higher but Oct Cat are languishing – stuck in a tight trading range! The issue is basically DEMAND! Cattle are pretty much dependent on only domestic demand – which has been faltering due to the slow pace of US restaurants reopens whereas Hogs are feeding off massive Chinese buying! As well, slaughter & avg weights are creeping higher in the cattle complex. Finally, the Sept Cattle-on-Feed issued Friday at 2 pm is expected to show a 6% increase in placements

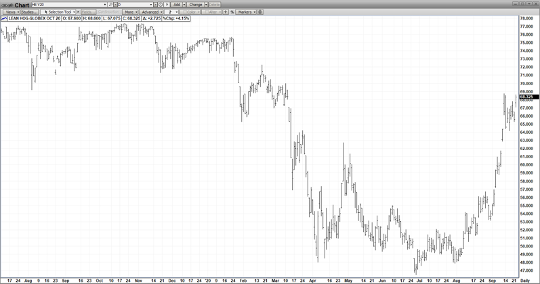

OCT HOGS

(Click on image to enlarge)

After getting pressured by bearish Macros Mon, Oct Hogs came back gangbusters today – gaping higher & pushing limit-up! That’s 3 upside gaps that the contract has left in 3 weeks' time! The same thing that has ignited the grains has likewise catapulted hogs to new rally highs – massive Chinese Demand! As well, Mexico has also contributed! So since early July, Oct Hogs have rallied $20 (47-67)! Should the US Economic Recovery continue, that would boost domestic demand – further augmenting already impressive “D”!