Case Study Of Tidewater And The Capital Cycle

Below is a case study of the capital cycle using Tidewater an offshore oil and gas playas an example. This page will be updated over time. This is not an investment recommendation but an ongoing case study. by John Chew, CSInvesting.

Tidewater: offshore oil and gas

Tidewater (TDW) - $6 on March 17, 2020, $315 million Enterprise Value, EBITDA of $15.3 million) offers an asymmetric risk reward opportunity for investors who can understand:

- this deeply cyclical industry. An investor must relate Tidewater to its environment.

- what Tidewater’s clean balance sheet of only $61 million of net debt (debt of $279 – 218 million of cash or 24% net debt to market capital using a $6 price per share as of March 17, 2019 and 42.4 million fully diluted shares) allows management to further consolidate a depressed industry at its trough while almost all its public competitors are distressed with zero equity values. Those circumstances offer Tidewater’s management a strong strategic but temporary advantage.

- that Tidewater’s assets are trading perhaps at 1/8 to 1/10th of their replacement value, and--while the market may further deepen the discount between the market price and replacement value during the current market dislocation—it shows the potential opportunity. Replacement values will be relevant when and if the industry can return to its normal economic returns of 45% to 50% vessel operating profits. Currently, replacement values have no bearing on market prices because the entire industry is distressed. Replacement values indicate the price of new supply.

- management has had successful experience consolidating the industry during the industry’s last major trough of 1982 to 1990. Some industry participants (The Cajun Mariner) consider this the worst downturn in the 65-year history of the OSV industry. “Too many ships, too much debt, and too many managers.”

- the current perceived oversupply of 1,200 boats may be overestimated by the market because of the deteriorating economics of returning vessels to service and the length of layups. Vessels are rusting in place.

- institutional shareholders such as Robotti & Co., Third Avenue Value, Moerus, and Raging Capital are all experienced small cap investors who can protect the interests of long-term shareholders.

- the necessity to be a long-term (three-to-five year) shareholder who is not adversely affected by price volatility and who will sell when capital becomes available for building new vessels. When capital returns aggressively to this cyclical industry, will be the sign to exit.

- that the offshore oil and gas industry must resume projects to replenish dwindling reserves while onshore tight oil and gas (fracking) declines rapidly in supply due to capital constraints and less Tier 1 acreage.

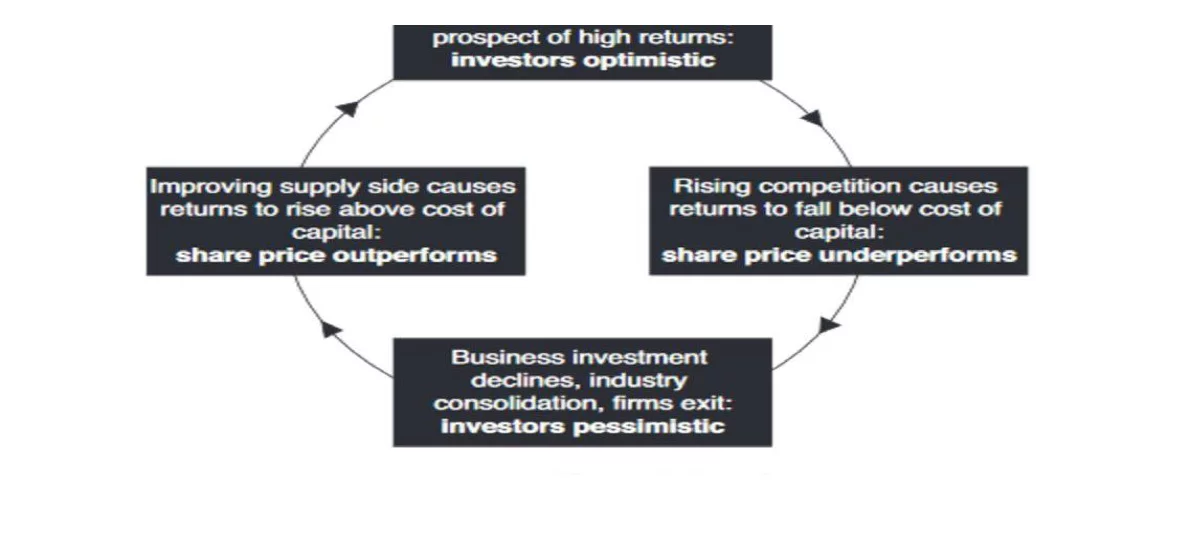

The Capital Cycle

Since the Offshore Support Vessel industry (“OSV”) is deeply cyclical because the vessels are capital equipment—vessels built new cost about $30 to $60 million--that service offshore oil and gas drillers who, in turn, are highly capital intensive and these customers base their spending plans on input costs to find and extract oil and gas and the expected price for their commodities. OSVs are a second derivative of offshore exploration and development activity. There are no barriers to entry in this commodity-based business except for capital constraints in a trough of the capital cycle like today.

Let’s go through the capital cycle diagram below starting from the left side moving clockwise. Improving supply allows for returns to rise to the cost of capital. Equity prices begin to ascend, analysts raise their earnings forecasts, growth investors take notice.

Returns go above the cost of capital, momentum investors pile in, the high current profitability often leads to overconfidence by managers, who confuse the robust industry conditions with their own skill. Investors and managers extrapolate the good times. The high profitability loosens capital discipline in the industry.

Capex expansion shown by capex greatly exceeding depreciation leads to more supply and competition. While investors are cheering expansion, returns begin to fall below the cost of capital and the share price underperforms.

The capital cycle turns down and bottoms as excess capacity becomes obvious and past demand forecasts are shown to be overoptimistic, profits collapse, losses mount, management teams are changed, capex is slashed, and the industry starts to consolidate. The reduction in investment and the contraction in supply allows for a recovery of profits. The full cycle can take years or decades. Since 2014, the OSV industry has been in contraction and is—I believe—with the double whammy of an oil price war and Covid-19 Virus pandemic close to a trough within the next few months if not year.

Read the full case study here.

Since Tidewater has been in business since 1955, its service is needed, but this is–at best–no more than an average business with no long-term competitive advantage. Currently, there is a trade-off between a decline in intrinsic value as time progresses without economic charter rates versus Tidewater’s competitive advantage over financially distressed competitors.

Disclaimer: This article is not an investment recommendation, Please see our disclaimer - Get our 10 free ...

more