Unraveling Retirement Strategies: Floor-And-Upside (An Update)

When a reader recently quoted me from a four-year-old post, I realized I needed to update a few of them. I've learned some things in the past few years and, like many of us who research retirement finance, my thinking has "evolved."

(My wife would undoubtedly question both claims, but I refer specifically to retirement finance matters at present.)

Sometimes reading an old post is like seeing a photo of yourself from 1975 with mutton chop sideburns a la Neil Young and saying out loud, "What was I thinking?"

One such post is Unraveling Retirement Strategies: Floor-and-Upside[1], from February 6, 2014. I've made a few changes to reflect my updated perspective and to incorporate some of the excellent reader comments that post attracted. Specifically, I've become more enamored with annuities and less with TIPS ladders.

The floor-and-upside strategy for financing retirement is sometimes referred to as “safety first” and derives from The Theory of Life-Cycle Saving and Investing[1].

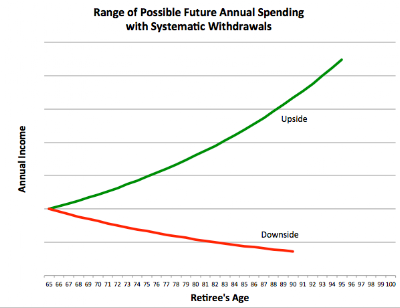

The basic idea behind floor-and-upside is that a retiree devotes some of her retirement funding assets to building a lifetime stream of income and the remainder to an investment portfolio to provide liquidity and the possibility of increasing wealth over time.

It's important to note that growth of the upside portfolio isn't guaranteed and, in fact, the "upside" investment portfolio may shrink over time or even be depleted prematurely (an "upside portfolio" also has downside). The "floor" is a safety net that will provide income should the upside portfolio fail. The rest of your retirement plan should ensure that having to live off the floor income alone is very unlikely.

Assets suitable for constructing the floor portfolio include Social Security retirement benefits, life-contingent annuities, and pensions. A TIPS bond ladder is not guaranteed to last a lifetime but it is conceivable that one could be built for 35 years, for instance, that would be highly likely to outlast a joint lifetime. Whether or not the cost of the ladder would be acceptable is another matter.

You could build a really simple floor-and-upside strategy by using part of your retirement savings to buy a life annuity to guarantee a certain amount of income for as long as you live and then investing whatever is left of your savings in an S&P 500 index fund.

In fact, since most Americans are eligible for Social Security retirement benefits, most Americans have a "floor." Those who also have some savings to invest in retirement, therefore, have a floor-and-upside strategy. Social Security benefits alone, however, may not provide as much floor as desired.

Deciding how much floor income you should build into your plan is sometimes easy. I've had clients say, "I don't care about upside potential, I'm not as impressed with my husband's investing skills as he is. I just want a check in the same amount monthly for as long as I live." This is a person who wants nothing but floor.

I also have had clients and readers say, "I believe in my investing skills and that the market will always eventually go up throughout my lifetime." Since some suggest that they should invest their Social Security benefits, too, I assume there is a group of retirees who want no floor at all.

In between these extremes, the decision can be more difficult. The best I can recommend is that you imagine that you are 85 and your upside portfolio balance just went to zero, a victim of sequence of returns risk. What is the least amount of income you could have remaining that would not make your life an economic misery? This is the floor level you wish to have.

The next question, of course, is whether you can afford that much floor and your level of wealth may or may not dictate that you choose a lower level. Interest rates are historically low at present so floors are expensive.

(A reader once commented that anyone who can afford a floor doesn't need one. Not true. Everyone can afford some level of floor even if it consists only of Social Security benefits. No one suggests that your floor cover 100% of what you hope to spend in retirement. That would indeed be expensive. Floor income should cover food, housing, clothing, and the like, but not the annual European vacations you planned before your upside portfolio confirmed your wife's suspicions about your investing skills.)

Here's an example. Let's say you want to spend $60,000 annually in retirement and your household expects $30,000 from Social Security retirement benefits. Non-discretionary spending totals $48,000 of the $60,000 total. (The floor doesn't have to be your non-discretionary expenses, it can be whatever makes you comfortable, but that's a reasonable starting point.) You have saved a million dollars for retirement.

You need another $18,000 of longevity-protected income. Wade Pfau's Dashboard[3] (or a quick online annuity quote from someone like myabaris.com) tells us that a single-premium income annuity (SPIA) for a 65-year old couple today will generate about a 5.63% payout at today's rates. Divide 18,000 by .056 and you can estimate that you need to annuitize about $320,000 of your savings to generate the safe floor you desire.

Invest the remaining $680,000 in stocks and bonds (I recommend index funds) and you have a floor-and-upside plan with $48,000 of longevity-protected income (from Social Security benefits and the SPIA) in the unlikely event that you prematurely deplete your savings portfolio.

There are a few critical concepts to consider at this point. First, the income from both the floor and upside portfolios assumes normal expenses. There will always be a risk of unpredictable, catastrophic expenses — a lawsuit, medical expenses, a child or grandchild who needs your financial support — that can blow up your retirement plan. Insurance may help and a reserve fund might, too, but there is always the risk that neither will be enough. We're planning only for the expenses that we can predict to some extent.

The second important concept is that, if we depend on a portfolio or a TIPS bond ladder for income, their liquidity is somewhat illusory. Both are sometimes referred to as "fettered" assets because we depend on them for future income. We often can't really spend them on something else. Spend from either of these sources when they're intended to provide future income and we give up all or part of that future income.

An annuity will become worthless at death unless you purchase (often ill-advised) options to prevent that. A TIPS bond ladder or an investment portfolio may have a remaining balance at death but that residual balance will be available to our estate, not to us while we are living.

It is true that an annuity provides less flexibility (more liquidity) than a TIPS ladder but the flexibility of the ladder is limited. A large medical expense can't be paid immediately from an annuity, it's true, but paying it from a TIPS ladder isn't much better. You're paying the expense from the source of funding for future years of retirement. An annuity will always provide more income than a bond ladder so you might be better off using the higher income to pay the large expense over time.

Bottom line, if you suffer a huge uninsured expense in retirement, you have a serious problem with any strategy.

A third important concept is that in many scenarios annuitizing part of your savings will result in a larger estate. This is counter-intuitive. In the above example, many retirees would think, "I just took $320,000 out of any future estate value because the annuity will be worthless when I die."

But, the annuity enables the upside portfolio to be invested more aggressively and lowers the retiree's sequence of return risk by reducing the periodic amount spent from savings. This will often lead to a larger estate than a portfolio-spending strategy alone.

Floor-and-upside is a compromise between using all our savings to buy annuities and investing it all in the stock market. We buy enough annuities to provide a safety net and invest the rest.

Annuities will provide for maximum lifetime consumption but have no value at death. Depending entirely on the stock market will provide more consumption and possibly a residual balance at death if the stock market gods favor us and less spending and a smaller bequest if they don't.

How does this fit into the theory of life-cycle saving and investing? That economic theory suggests that households should prefer reducing their consumption a bit in good times if it will improve consumption a bit in bad times ("consumption-smoothing"). We buy health insurance when we are healthy in good economic times, though it may have no immediate benefit, so we will be able to consume more at times when we are unhealthy and have large medical expenses.

Floor-and-upside gives up some of the stock market gains in the good outcomes to make sure we have a bit more income in worse scenarios with poor market returns.

The floor-and-upside strategy will combine the two such that they provide a safety-net level of lifetime income and an opportunity for more consumption if those stock market gods smile down on us.

If they find us annoying, we'll still have the safety net.

I'll describe the remaining major category of retirement funding strategies, the “bucket”, or “time-segmentation” strategy, in future.

REFERENCES

[1] The Retirement Café: Unraveling Retirement Strategies: Floor-and-Upside.

[2] The Theory of Life-Cycle Saving and Investing, Federal Reserve Bank of Boston.

[3] Dashboard, RetirementResearcher.com.

Disclosure: None.