Rates Spark: Powell To Cement US Curve Dynamics

Fed chair Jerome Powell’s testimony, if it confirms recent themes in Fed communication, will likely push rates higher and flatten the yield curve. Despite the growing focus on recession risk, bonds are finding no favor among investors.

Hard to see what could prevent more yield upside

One salient characteristic of rates price action so far this week is bonds’ ability to sell off on both risk-on and risk-off markets. Arguably, in each instance, it was a different part of the curve that was in the lead, but this is beside the point. In a week that looked like a prime candidate for a bond consolidation, with light supply and event risk, rallies look to have been systematically sold into. It seems to us that the macro environment is conducive to rates testing higher levels still, with 3.5% and 2% the obvious near-term targets for 10Y Treasuries and Bund.

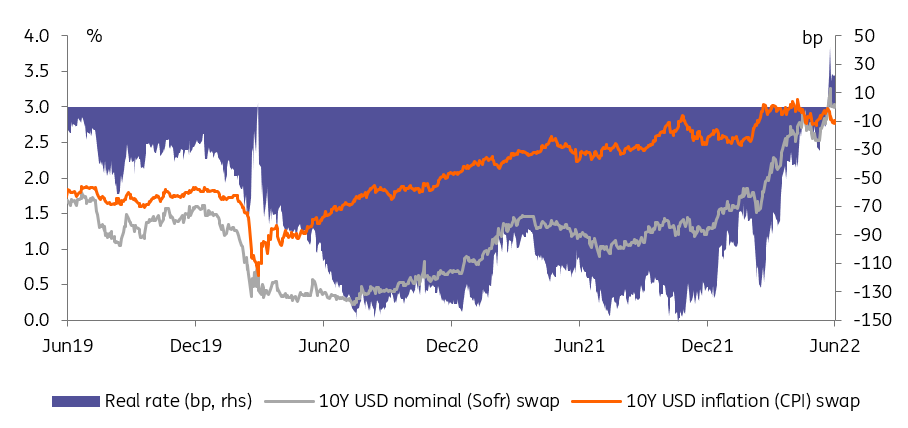

The Fed has capped long-term inflation expectations, but not nominal rates

Image Source: Refinitiv, ING

The macro environment is conducive of rates testing higher levels still

Only a sharp rise in already elevated recession risk, or a change in central bank tone, could change this dynamic in our view. After consistently underestimating inflation, we would discount the latter. Bostic brandishing the prospect of a pause in the Fed’s tightening looks like a communication accident that is unlikely to be repeated anytime soon. As for rising recession risk, it is notable that that idea has already entered the market’s subconscious, and failed to prevent rates upside. Exhibit one is the Fed’s June dot plot, featuring growth forecast downgrade and unemployment upgrades. Hopes of a “soft(ish)” landing were also relegated to just that, hopes.

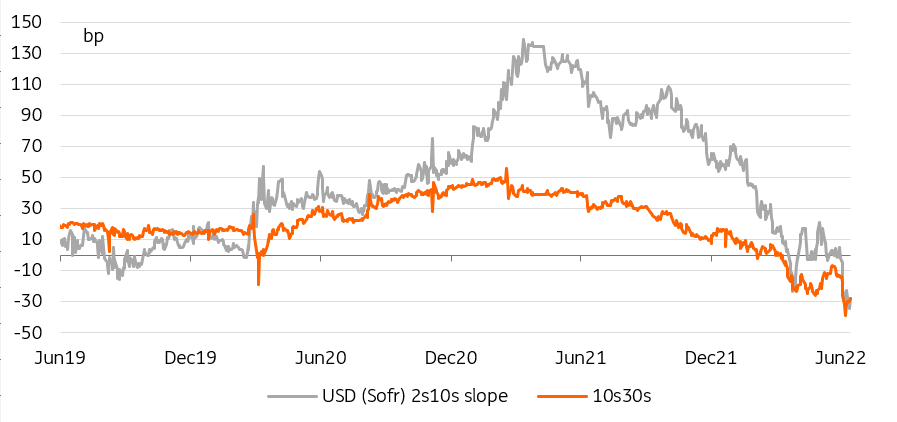

Recession risk and the Fed’s short-term focus mean a flatter curve

With a Fed finally on its front foot when it comes to fighting inflation, and markets already aware of growing recession risks, one can reasonably ask what Powell could say today that would catch markets off guard. We entertain the hope that has caught up with the market’s way of thinking about inflation dynamics, Fed policy, or rather its disconnect with the market consensus, is no longer a factor adding to market volatility.

Bonds and swaps are paying attention to short-term developments, especially on energy markets

A continued focus on more short-term inflation developments, and on headline inflation rather than core, would reduce the inflation swap markets’ ability to cap long-term nominal yield upside. Taking 10Y CPI swaps dipping once more below 3% as an example, long-term inflation fears have been kept in check by an increasingly hawkish Fed. The continued sell-off in nominal rates shows that bonds and swaps are instead paying attention to more short-term developments, especially in energy markets. This is a step in the right direction, particularly if Thomas Barkin’s comments that his aim is to see positive real rates across the curve are to be taken at face value.

Recession risk and curve inversion appear to be stuck in a self-fulfilling narrative loop

Image Source: Refinitiv, ING

Combined with the growing focus on recession risks, the admission by the Fed that taking the Fed Fund rate well above neutral implies subsequent cuts. This points in the direction of a further inversion of Sofr forwards, and also a flattening of the spot-starting yield curve. This may only be a short-term phenomenon, either until the outlook worsens so much that the market pares back hike expectations (bull-steepening), or until markets converge with the view of stubbornly high inflation, dashing hopes of subsequent easing (bear-steepening). For now, however, growing recession risks and a curve inversion are self-sustaining dynamics that cannot be ignored.

Today’s events and market view

It will come as no surprise that Fed chair Jerome Powell’s congress testimony is the main focal point in rates markets today. If recent central bank comments are anything to go by, the tone should be hawkish. The pull-back in rates since their pre-FOMC peak suggests markets can still be caught off guard, for instance by Powell keeping the door open to more than one 75bp hike should data require it.

The chairman is the most important Fed speaker on the calendar, but by no mean the only one. Thomas Barking, Charles Evans, and Patrick Harker complete the line-up. Jon Cunliffe, of the Bank of England, Luis de Guindos, and Frank Elderson, of the European Central Bank, are also due to speak.

On the economics calendar, Eurozone consumer confidence is expected to stabilize at levels already consistent with a recession.

Germany will raise funds by tapping its 15Y benchmark. This will be followed in the US session by the US Treasury selling 20Y debt.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more