The looming energy crisis in Europe is grabbing investors’ attention but markets cannot dismiss a hawkish Fed. The ingredients are in place for a further widening of USD-EUR rates differentials, even in the long end due to falling inflation swaps.

EUR rates are increasingly immune to inflation risk

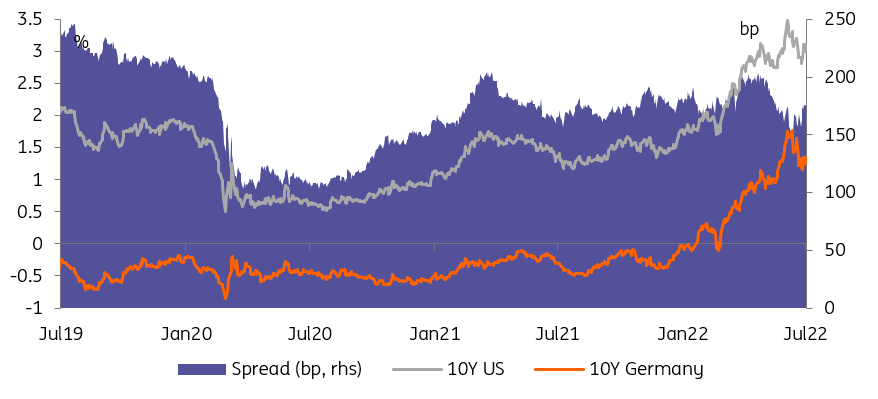

The week has only just started but we can already draw some conclusions on the two themes that are driving markets. First, recession fears continue to grip investors and limit interest rate upside. Second, Europe is still the epicenter of these recession fears, with uncertainty relating to its energy supply further driving a wedge between USD and EUR rates. In the short end, this has driven EUR/USD ever closer to parity, as our FX colleagues have flagged. At the longer end, the spread between 10Y US Treasuries and Bund yield is getting nearer to its 200bp peak in this cycle.

The energy crisis could widen the 10Y Treasuries-Bund back to 200bp

Image Source: Refinitiv, ING

The long end of the EUR curve may move down more easily

The result was another day of double-digit trading ranges across most bond markets. If 10Y yields are still well within their 2Q 2022 range, it feels the long end of the EUR curve will more easily move down, with long-term inflation swaps also dipping back towards the ECB’s 2% target. The implication is that one way or another, inflation will come back under control, and so long-dated bonds are safe to invest in. This collapse in a proxy for inflation expectation might also be the reason why front-end EUR rates failed to rise on hawkish comments from Austrian central banker Robert Holzmann. Currency weakness has been quoted as a key reason for central banks to hike rates across the world but EUR markets have so far ignored that risk and continued pricing out hikes.

Gloom in Europe, but inflation is still a theme in the US

This may change if releases later this week cement the case for a more hawkish Fed. Germany’s Zew confidence survey should add to the overall gloom but the consensus is already for a worsening of both the current and expectations components. Any energy-related headlines would be more relevant but hard facts could prove elusive until the reopening of the Nord Stream pipeline scheduled 10 days after its planned closure for maintenance. In the meantime, markets are tempted to see the glass half empty.

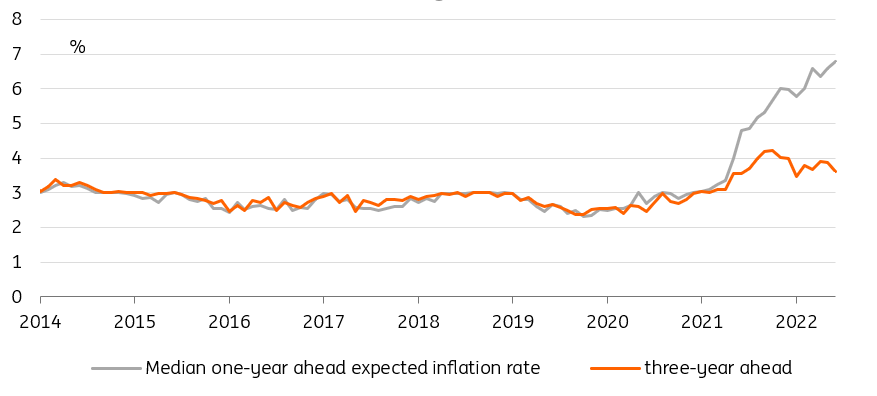

Consumer inflation expectations are sending mixed messages to the Fed

Image Source: Refinitiv, ING

For now, US rates may be tempted to ignore market indicators of falling inflation expectations. The NY Fed’s consumer survey shows increased expectations for the near term, but a stabilization for longer periods. In a context of high uncertainty, and of egregious forecasting errors, one could be tempted to focus on the near-term picture, or even on backward-looking inflation indicators. If this is indeed the case at the Fed, then the curve would be right to price aggressive tightening until the end of this year, but subsequent cuts next year, as our economics team forecasts.

Today’s events and market view

Sentiment indicators feature prominently on today’s calendar. In Germany, the Zew survey will give an early read on local sentiment for the month of July. If financial market sentiment, and the flurry of energy crisis headlines, are anything to go by, further worsening from low levels are likely. In the US, the National Federation of Independent Business small business optimism will be the highlight. With housing being one of the first sectors to feel the pinch from Fed tightening, markets are braced for another low reading.

Germany is due to auction €5.5bn of 2Y bonds. The EU will also launch a new 7Y benchmark alongside a tap of its 2041 bond for a total of €8bn. This will come hot on the heels of the Netherlands selling 10Y debt.

Central bank speakers due today include Francois Villeroy of the European Central Bank, Thomas Barkin of the Fed, and Andrew Bailey of the Bank of England.

More By This Author:

FX Daily: EUR/USD Can Drop To 0.98FX Daily: Surfing On Parity

Key Events In Developed Markets For Week Of July 11

Comments

Log in or sign up to join the conversation.