Rates Spark: Let The Music Play

A tame US CPI print in January means markets don't have to worry about a hawkish Fed for now. A look at a broader set of indicators than just interest rates shows the reflation trade is alive and kicking. Risk appetite should continue to improve, pushed by ever lower real rates.

Source: Shutterstock

Overnight: Powell helps yields stay low

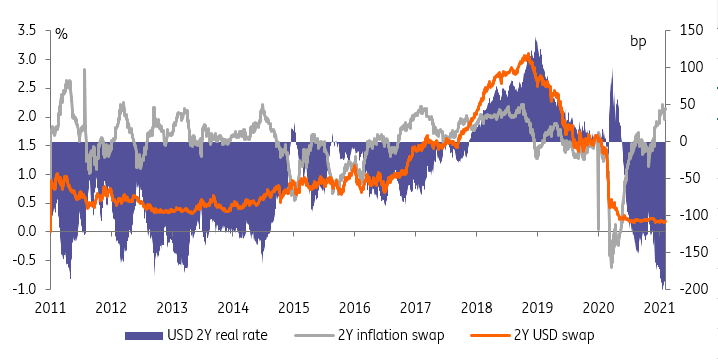

In a speech that was very much in keeping with the Fed's cautious tone of late, chairman Jerome Powell stressed a large amount of slack in the job market, with around 10 million jobs lost in a year. His call for further support to the job market in addition to monetary policy comes at a time the Biden administration's stimulus plan has been accused of being inflationary, and will likely be understood by markets as another sign the Fed won't try to preempt any overheating as a result. It is consistent in our view with the rise in inflation swaps continuing to outpace nominal rates, especially at the front-end of the curve (see chart below).

These comments and the decent demand at yesterday's 10Y T-note auction were enough for US Treasuries to hold on to their gains in the Asian session. There were signs of improving risk sentiment, however, in the form of higher stock futures and in the EURUSD exchange rate.

Nominal rates muted, but other markets are pricing in higher inflation

When one focuses only on the path of nominal yields, this week could seem like a bruising one for proponents of greater economic optimism and reflation. Last week’s sell-off in 10Y US Treasuries has reversed by around 2.5bp, while 10Y German yields have remained stable. To be sure, some of the blame lies at the feet of a disappointing US CPI print yesterday, but our economics team cautions against the relevance in recent figures, heavily impacted by the distortions of the pandemic, especially compared to price dynamics as the economy reopens in the coming months.

2Y USD real rates dipped, propping up risk asset valuations

Source: Refinitiv, ING

A look at a broader set of market indicators yields a more upbeat conclusion for proponents of the reflation trade. Oil and copper for instance staged impressive rallies this week. Not only will these key input prices eventually feed into future inflation prints, they also betray a degree of optimism about the global economy. The same can be said about stock indices printing new highs this week.

The grind higher in inflation swap rates can continue unabated

Taken together, the limited near-term inflation print and intact economic optimism suggest the grind higher in inflation swap rates can continue unabated. This should ultimately translate into higher nominal rates but for the time being, deeply negative real yields are supportive for risk appetite globally. The upshot of data so far is that there is no pressure on central banks to flag tightening just yet, so the party in risk assets can go on for a while longer.

Today’s events and market view

The US Treasury will carry out its second long-dated auction this week, in the form of $27bn 30Y T-bonds. We expected the run-up to the sale to add steepening pressure to the USD curve this week but we were proven wrong. The macro rationale for higher rates remains in place although yesterday’s US CPI print might extend the period of relatively orderly price action in USD rates until the prospect of higher inflation readings in mid-2021 dawns on markets.

Weekly jobless claims will be another potential flashpoint in a session otherwise bereft of major economic drivers. Here too, better data will have to wait until more states reopen.

Italy will also carry out 3Y/7Y/20Y debt sales. We extended the 10Y Italy-Germany spread tightening target from 90bp to 75bp yesterday as local bonds ride the wave of optimism created by the nomination of Mario Draghi as prime minister, and as deeply negative real yields are good for debt dynamics.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more