Market Briefing For Jan. 2, 2019

New Year's Greetings might well be mixed; but not an omen for the entire 2019 market prospects. Sure, there are lots of variable contingencies early in this New Year; with my suspicions that we work through them (even if that means lower lows in the S&P before all is said and done).

Remember, this is a 'transition year for technology', plus ahead of the 2020 Election tensions; so that reinforces the idea that most significant 'problems' for the market require sorting-out in the year's first half. Perhaps oddly, from a market standpoint, getting an 'acceptable' Trade Agreement with China is probably the most potentially favorable issue confronting markets; while the unknown characteristics of the political probe (inquisition?) the greatest odd unknown takeaway for markets down the line a bit. If there's anything really capable of disruption past the year's first half, that might be on the agenda.

During 2018 bond traders began to see an increase in 'Auction sizes' after President Trump signed off on tax cuts. That surely heightened prospects of trilltion-dollar deficits and a surge in bond supply in coming years; beyond of course the already-heavy roll-off calendar the Fed has to deal with. Maybe, just maybe, the Fed is grappling with this knowledge and thus absolutely is moving as they are, before that surge creates more bloated (dire?) scene.

So that's probably 'why' the classic equity/rate relationship got distorted plus the subsequent (more recent) rush to Treasures for perceived safety. To put this in a summary form (remember I'm not a bond guy), consider that a Fed, nervous as heck about what's coming, started to price a fiscal premium into US Government long-rate bonds.

If so the historic correlation between stocks and bond yields may not just be temporary as Washington aims to give us trillion dollar deficits for sometime into the future. And frankly (aka Japan) things deter that when rates firm on their own beyond this incredibly bloated supply situation, which would really be exacerbated if they don't roll-off the so-called 'automatic pilot' 600 billion, as they planned; but Wall Street and politicians are trying to dampen.

In sum: this is basically what I've talked about for months as far as 'why' we have a Fed hell-bent on snugging-up, and rationalizing monetary policy 'as if' it were related to domestic economics in 'this' situation. I thought it global in nature; recognize the ECB is coming down a similar path; that China too has enormous debt issues; and that indeed the US economy is sluggish to a degree that does 'not' support higher rates; but the overall picture required.

In fact, this 'infinite vision' deficit picture, might 'demand' even higher yields on the long-end for some time, 'even if' stocks under-perform and economic sluggishness (recession officially or not) prevails. Needless to say, 'if' one is looking for a 'potentially bearish' picture beyond obvious price corrections or trade issues, or the many variables, consider this.

A teetering stock market, if also combined with unavoidable higher rates, is a truly concerning proposition, is it not? This is the backdrop we've indirectly reflected upon through much of 2018's Fed policy (thinking they have to do this regardless); and I thought I'd take a few moments to more clearly try to explain how this could affect a sketchy market environment for 2019.

Sure, we'd get huge rebound rallies from a 'trade deal' (or avoiding political chaos), which is also short-term in terms of market response. While 'trade' and regulatory relief remains will become more favorable for stocks once a 'deal' is done; tax cut benefits won't have the impact of the past; and - very notable to all this as well - buybacks will diminish with enduring higher long rates. This becomes a competitive issue to equities, should that prevail. So it is a reason I suspect this topic needed to be simplified a bit.

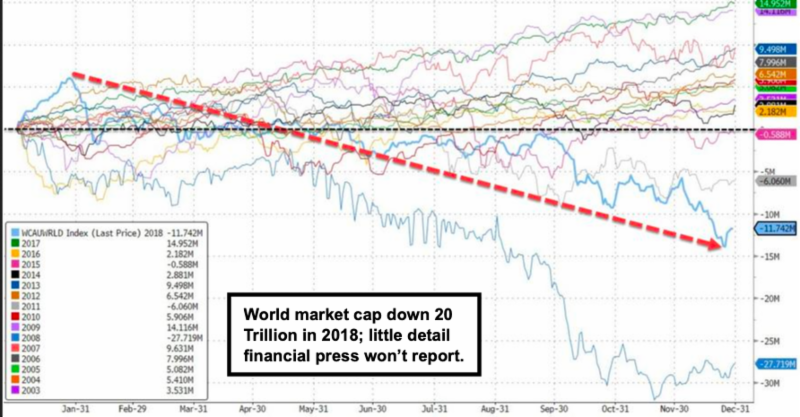

Bottom-line: 2018 was a challenging but rewarding 'bear market year'. It's one in which most only belatedly recognized it for what it was. And in 2019 it will only reluctantly be acknowledged that it was the overly-easy for so long Fed (Bernanke's) that set-up a problem to normalize policies; and what has become an unavoidable necessity to unwind the Balance Sheet (that's the supply issue I've referred to); given the new additions forthcoming.

Shame of course the Fed couldn't truly explain the extent of this challenge; but we shall see if that is sufficiently offset by a potential China trade deal or not. Remember, our bullishness for 2017 was predicated on tax relief (and so on) propelling the market even though the Fed was already removing the punch-bowl at as gradual a pace as they could. The market was already in shaky territory, which is why I thought it could buy time and 'shoot to the moon' if Trump won and we got the fiscal set-up. Of course that also trims the Treasury; so now the other side of the coin is the ballooning deficits as it's not really feasible to 'truly' grow our way out of the situation with ease.

It will be a challenging 2019; but in a different way; and ideally (for those of us who built liquidity in 2018's rallies months ago) good periodic entry points (and I intent that to be plural), as there are many variables ahead.