Since the end of the fake debt ceiling fight on June 2, the Treasury has borrowed an additional $700 billion pushing the national debt over $32 trillion. Looking at the interest rates on this new debt, it becomes clear that the US government has a big problem.

The surge in borrowing in the wake of the debt ceiling deal was expected. The Treasury is playing catch-up after nearly six months up against its borrowing limit. But even after the Treasury replenishes the federal government’s checking account (called the Treasury General Account or TGA at the New York Federal Reserve Bank), borrowing won’t suddenly stop.

The debt ceiling deal supposedly cut spending, but we know actual spending will continue to rise. Given that the Biden administration is blowing through an average of $500 billion each month and running massive deficits month after month, it’s clear the misnamed “Fiscal Responsibility Act” did nothing to address the root problem.

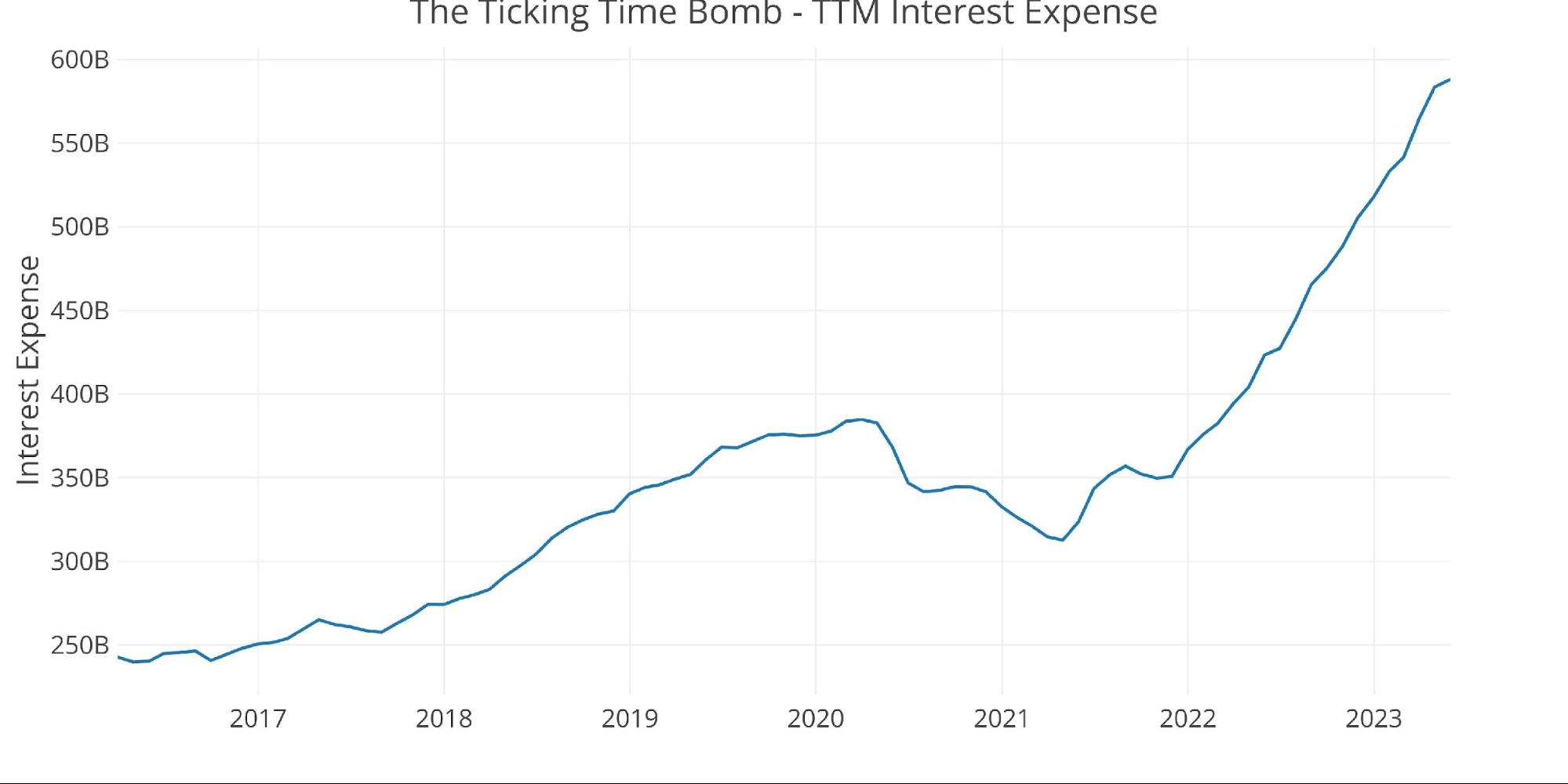

The problem isn’t purely a function of more debt. The bigger issue is that this new debt comes with a much steeper price tag. Interest on the national debt is rising at an alarming clip.

The trailing 12-month (TTM) interest on the debt clocked in at just under $600 billion in May. This was up from $350 billion at the start of 2022, less than 18 months ago. The government has added an extra $250 billion in expenses per year on just debt service.

This is just the beginning of an upward trend. Based on the current interest payments, the Treasury is paying less than 2% interest on the total debt. But a lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bills, notes, and bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

Looking at the Treasury sale on June 26 reveals the extent of the problem. The Treasury sold $162 billion in securities, with $120 billion in short-term Treasury bills with high yields.

- $58 billion in six-month bills at an investment yield of 5.45%

- $62 billion in three-month bills at an investment yield of 5.34%.

- $42 billion in two-year notes at a high yield of 4.67%, amid very strong demand. Longer-term yields are still far below short-term yields.

With this flood of Treasury bills, the share of short-term paper underpinning the debt is approaching 20%. That’s considered the upper limit, meaning the Treasury will soon have to turn to issuing longer-term notes and bonds. That means the Treasury will be locking in higher interest rates for the long term.

An analyst cited by Bloomberg projects a $600 billion rise in notes and bonds beginning in August through the end of the year. Issuance will likely ramp up further in 2024 with a projected additional $1.7 trillion in notes and bonds.

Who Will Buy All This Paper?

This raises another important question: who is going to buy all of these notes and bonds?

Some of the biggest buyers are in the process of reducing their holdings.

- According to the Treasury Department’s TIC data, foreign buyers shed $140 billion in holdings in April compared to 2022.

- US banks shed $210 billion in Treasury securities and $332 billion in mortgage-backed securities in May compared to a year ago, according to Federal Reserve data. This is continuing fallout from the financial crisis as banks struggle with unrealized losses from holdings they bought when yields were artificially low.

- As it tightens monetary policy to fight inflation, the Fed has been unloading Treasury securities at a rate of around $60 billion a month to shrink its balance sheet.

In effect, the US Treasury is increasing the supply of Treasury securities even as demand is falling.

It could result in a ‘demand vacuum’ that would be resolved by higher yields for longer maturity securities, according to Bank of America, cited by Bloomberg. Yield solves all demand problems, and long-term yields have been much lower than shorter-term yields, with the 10-year Treasury currently at 3.71%.

The only way demand will rise to absorb this supply is if yields on the upper end of the curve rise. And that means additional interest expenses for the federal government locked in over many years.

If interest rates continue to rise and remain elevated for an extended amount of time, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

This calls into question the Fed’s ability to stay in the inflation fight. Eventually, it could be forced to cut rates in order to keep the US government solvent. And it also may need to go back to quantitative easing in order to artificially boost demand for Treasury securities.

More By This Author:

Gold Correction Is At Or Near Completion

Comex Countdown: The Pressure Grows In Silver And Platinum

What’s Going On With The Fed Balance Sheet?

Comments

Log in or sign up to join the conversation.