Gold Miners: Are PMs The New Titanic?

Inflation is lurking for investors like a well-hidden iceberg. One false step and there is nothing left but a massive price-drowning.

With the PMs becoming an ocean of optimistic and pessimistic mood swings, their daily waves have disguised a storm surge that’s building off in the distance. With inflation soaring and one policy error liable to capsize their entire vessel, precious metals investors, like the Titanic, are blindly sailing toward their demise – with a band playing aboard.

Case in point: while market participants believe that the U.S. Federal Reserve (FED) has the ability to control interest rates, its powers are actually extremely limited. And with the FED’s bark much more vicious than its bite, the central bank has a monopoly on the ‘confidence’ market, not the bond market. Translation? As long as investors believe in the FED’s narrative, the ‘confidence’ filters across financial markets and allows asset prices to reflect the FED’s wishes. However, as history has shown, if that confidence erodes, all bets are off.

On Apr. 30, I warned that inflationary pressures could force the FED to raise interest rates much sooner than expected.

I wrote:

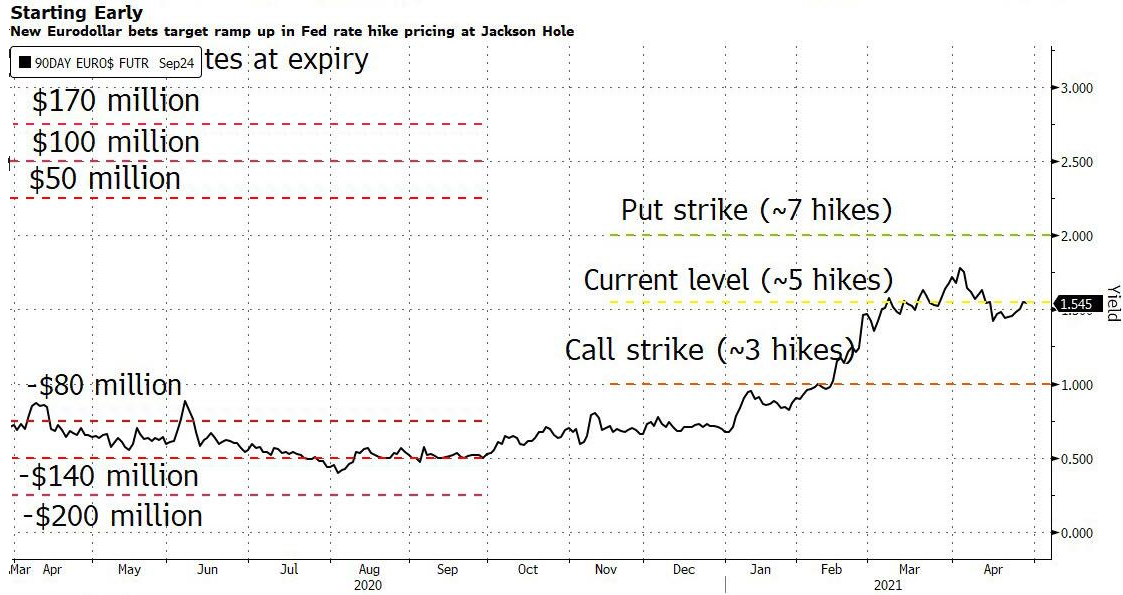

A material Eurodollar options position signals that a hawkish shift could occur by late August. With the options bet expiring on Sep. 10 – right before the FED’s Sep. 22 policy meeting – the date is rather peculiar. But with the FED’s annual Jackson Hole Symposium held in late August – where Powell unveiled a new policy framework for inflation in 2020 and then-FED Chair Ben Bernanke teased more bond purchases in 2012 – this year’s event could result in similar fireworks.

Please see below:

Source: Bloomberg/ZeroHedge

To explain, Eurodollar futures and options are used to speculate on short-term interest rates. More specifically, the contract reflects the implied 3-month U.S. dollar LIBOR (London Interbank Offered Rate). And with Eurodollar futures currently implying roughly five rate hikes by the FED by Mar. 2024 (contract settled at 98.7700 on Apr. 29), the large trader bought Eurodollar put options that imply roughly seven rate hikes by the FED by 2024. As a result, the "extremely high conviction" trade could be a $60 million windfall if Eurodollar futures fall sharply by Sept. 10.

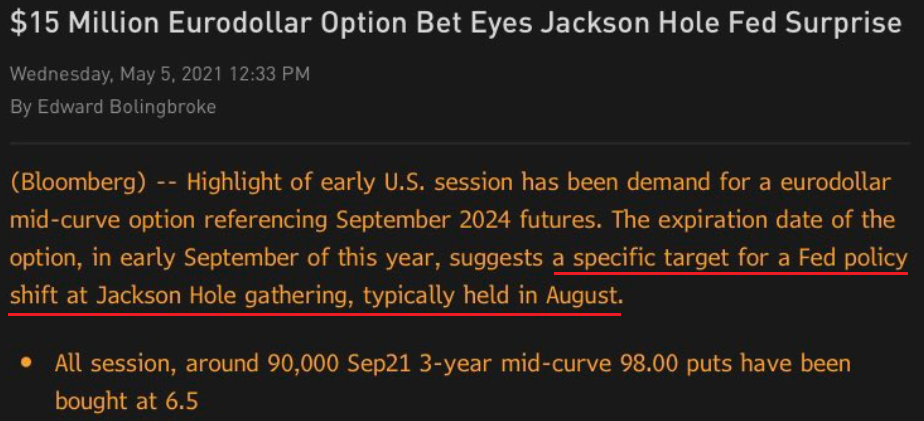

And with ‘confidence’ beginning to crumble, another 90,000 Eurodollar put options were purchased on May 5, mirroring the 200,000 put-option position that was opened last week. Thus, while a bevy of FED speakers reaffirmed their commitment to quantitative easing (QE) on May 5, investors suddenly aren’t so sure.

Please see below:

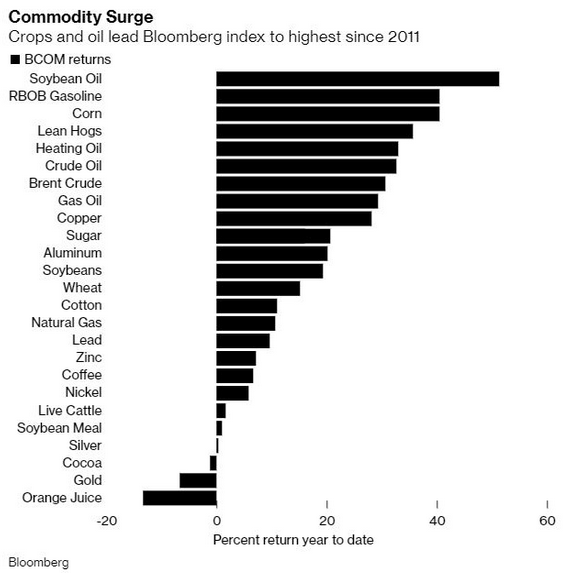

Hiding in plain sight, cost-push inflation continues to skyrocket. And with speculation in the commodities market showing no signs of slowing down, lumber futures have already surged by nearly 9% this week.

In addition, it’s not only lumber that’s sounding the alarm. While gold has been the second-worst performing commodity year-to-date (YTD), basic necessities like heating oil and pork products have been on a tear since New Year’s Day.

Please see below:

More importantly, though, once the effects of rampant commodity speculation have time to filter through the real economy, the FED’s promise of “transitory” inflation will likely lose credibility.

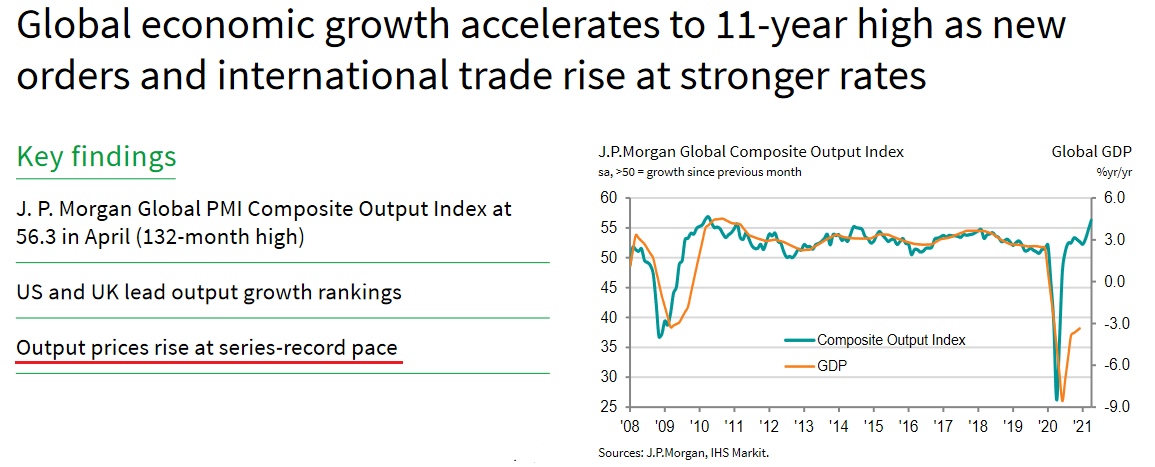

Source: IHS Markit/Bloomberg

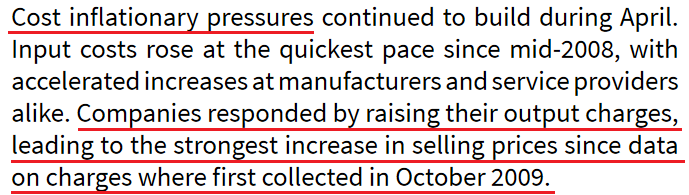

If that wasn’t enough, the Institute for Supply Management (ISM) released its services PMI on May 5th. And in what’s become a recurring theme, the report read:

“The Prices Index figure of 76.8 percent is 2.8 percentage points higher than the March reading of 74 percent, indicating that prices increased in April, and at a faster rate. This is the index's highest reading since it reached 77.4 percent in July 2008 ….All 18 services industries reported an increase in prices paid during the month of April.”

For context, the ISM requires written permission before redistributing any of its content, and that’s why I quoted the findings rather than included a screenshot of the report. However, if you want to review the source material, you can find it here.

Continuing the theme, the J.P. Morgan Global Composite Output Index (also released on May 5) rose to its highest level (56.3) in 132 months. For context, the survey tallies responses from roughly 27,000 companies in more than 40 countries that account for roughly 89% of global GDP.

Please see below:

More importantly, though, rising commodity costs have already caused output inflation to surge at its fastest pace ever.

Sources: J.P.Morgan, IHS Markit

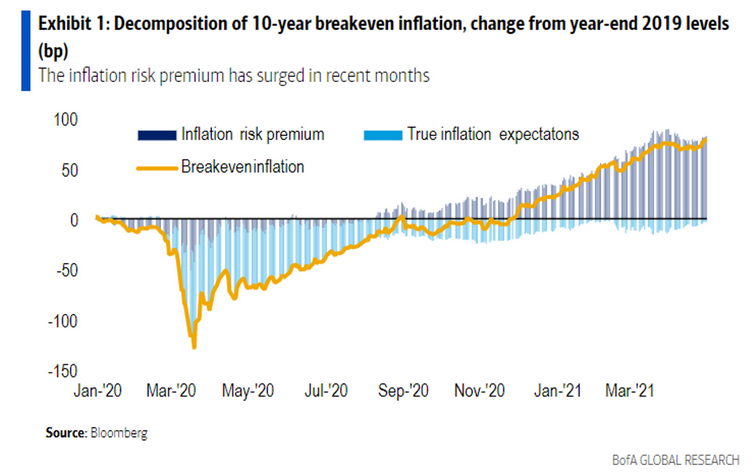

What’s more, Bank of America revealed on May 5th that investors have become increasingly skittish about rising inflation. Case in point: while the inflation risk premium has surged in recent months, we haven’t even scratched the surface of what’s likely to occur once coronavirus restrictions are lifted. And with investors already demanding increased compensation to weather the current storm, more bouts of volatility are likely to erupt over the medium term.

Please see below:

To explain, the dark blue bars above (they look gray) track the inflation risk premium. For context, the inflation risk premium represents the additional compensation that investors demand in order to hold assets that are negatively impacted by rising inflation (like long-term bonds and technology stocks). If you analyze the right side of the chart, you can see that investors have already started to doubt the FED’s ability to control the situation. More importantly, though, with Bank of America recommending that investors “shorten duration” – which is finance vernacular for “don’t own long-term bonds or technology stocks” – it’s only a matter of time before we witness another yield spike.

Source: Bank of America/MarketWatch

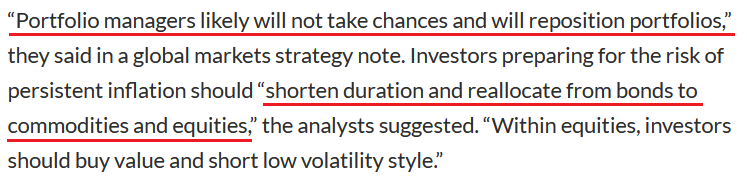

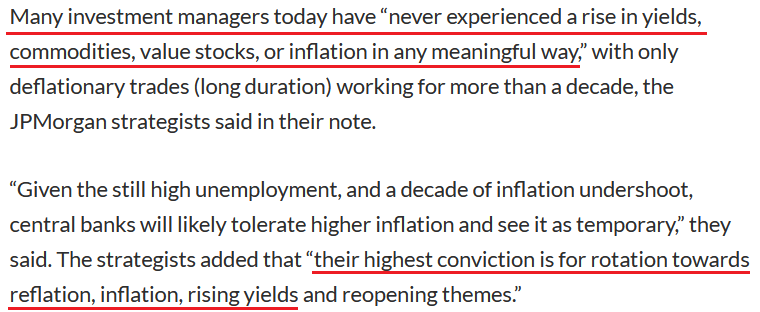

Likewise, J.P. Morgan is also singing a similar tune:

Source: J.P. Morgan/MarketWatch

The bottom line?

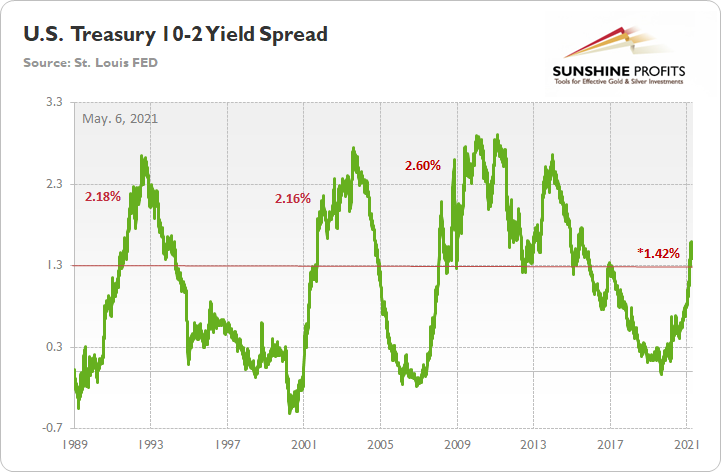

While the U.S. 10-Year Treasury yield remains in consolidation mode, it’s important to remember that the U.S. Treasury 10-2 yield spread hasn’t made a new low.

To explain, when the green line above is rising, it means that the U.S. 10-Year Treasury yield is increasing at a faster pace or declining at a slower pace than the U.S. 2-Year Treasury yield. Conversely, when the green line above is falling, it means that the U.S. 2-Year Treasury yield is increasing at a faster pace or declining at a slower pace than the U.S. 10-Year Treasury yield. In addition, the 10-2 spread is more relevant than analyzing their behavior in isolation because the ‘neutral rate of interest’ has changed dramatically over the last 30 years.

More importantly, though, after peaking at 1.59% on Mar. 29, the 10-2 spread corrected back to 1.39%. However, with the milestone marking a 20-basis-point decline over 18 trading days, the 10-2 spread’s behavior mirrors what we witnessed in 2001/2002.

To explain, I wrote previously:

After reaching an interim peak in 2001, the 10-2 spread declined by 20 basis points over a 17-day stretch. However, the 10-2 spread followed its 2001 swoon by rallying by 105 basis points over the following 97 days (into 2002).

If you analyze the horizontal red line, 1.30% is where historical roads got a little rocky. However, after recording a major bottom, rallying above 1.30% and then suffering a meaningful correction, the 10-2 spread proceeded to rally to 2.18% (1991), 2.16% (2002) and 2.60% (2008) before suffering a second meaningful correction.

Thus, while the PMs have enjoyed the U.S. 10-Year Treasury yield’s recent calm, the tranquility is unlikely to last over the medium term. Moreover, while the FED’s gambit of letting the genie out of the bottle is the easy part – by flooding the system with liquidity – putting him back in the bottle is unlikely to happen so smoothly.

In conclusion, gold moved higher on May 5th, while silver demonstrated relative weakness. And with the upside-down price action highlighting a lack of conviction among precious metals investors, the PMs have become increasingly rangebound. Moreover, with the U.S. 10-Year Treasury yield suffering from a similar affliction, the standoff is likely to continue until one side officially draws their guns. However, with fundamentals favoring the latter, the U.S. 10-Year Treasury yield has a lot more bullets in its chamber. As a result, the FED’s loyalty to liquidity will likely cause the PMs more harm than good over the medium term.

Disclaimer: All essays, research and information found on the Website represent the analyses and opinions of Mr. Radomski and Sunshine Profits' associates only. As such, it may prove wrong ...

more