FOMC Minutes Signal Governors Divided Over When To End Policy-Easing

Having cut rates (as expected) and suffered dissents (2 hawkish, 1 dovish) at the September FOMC meeting, things have not gone exactly as planned for Mr. Powell and his pals.

Stocks are weaker, the dollar is stronger, gold is flat (so they'll be happy, but remember the Golden Week seasonals), and the long-bond is ripping higher (in price)...

(Click on image to enlarge)

And The Fed rate-cut appears to have perfectly top-ticked US Macro data also...

(Click on image to enlarge)

Source: Bloomberg

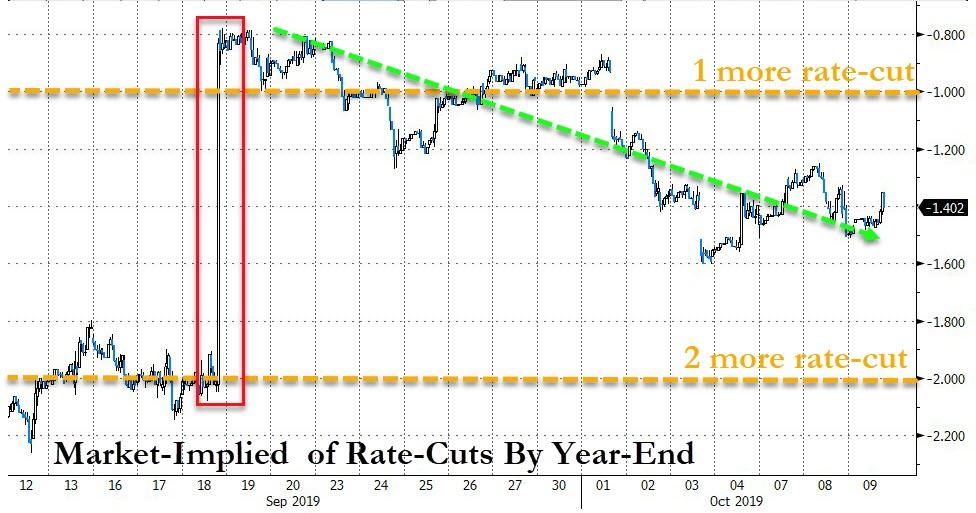

Since the Fed cut rates in September, the market has shifted to demanding more, now pricing in 1.4 more rate-cuts by year-end, considerably more dovish than the 0.8 rate-cuts on the day they actually cut in September...

(Click on image to enlarge)

Source: Bloomberg

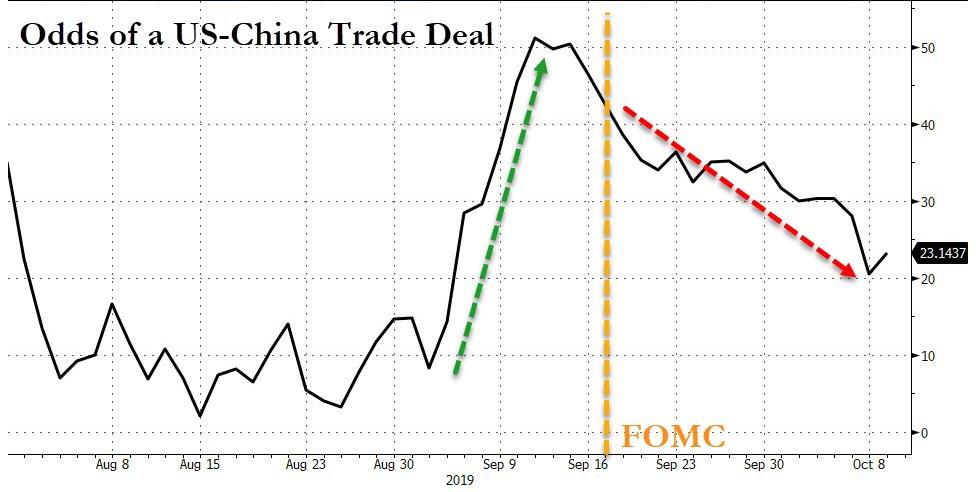

But, as far as buying insurance for a worsening trade outlook, The Fed's timing was good...

(Click on image to enlarge)

Source: Bloomberg

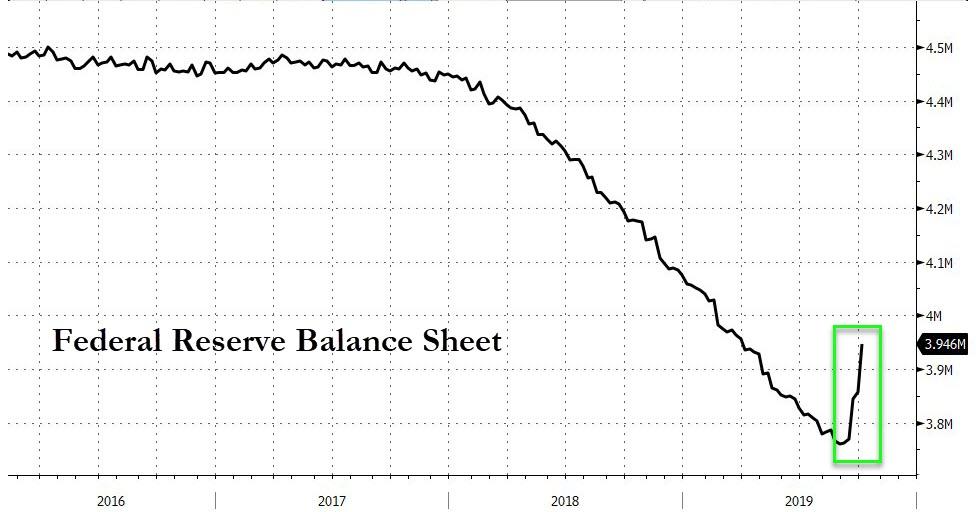

And don't forget that the Fed's balance sheet has started to re-inflate (NotQE)...

(Click on image to enlarge)

Source: Bloomberg

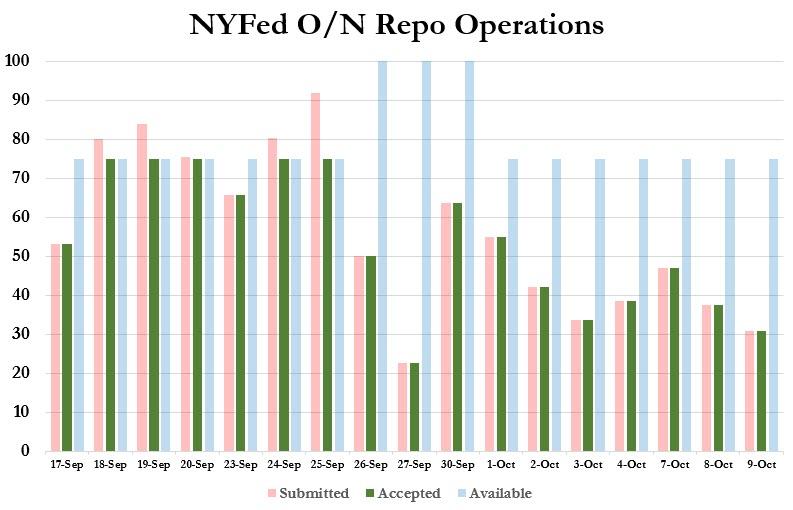

And its liquidity bailouts have not stopped...

(Click on image to enlarge)

Source: Bloomberg

***

As Bloomberg Economics noted:

"A core focus in the meeting minutes will be to better assess not only the firmness of officials’ resolve to avoid substantial additional accommodation, but also the conditions which would lead them to potentially reconsider."

So, under the hood, what is it that The Fed's tightly narrative-controlled Minutes wants us to understand (bearing in mind, of course, that Powell unveiled NotQE yesterday)...

Most notably, The Fed appears more divided than was assumed, and definitely have a more hawkish tilt to them - fearful of the market wanting more at a time when the economy/inflation does not necessarily need them is a notable discussion.

Several participants cited considerations that led them to be concerned about financial stability, including low risk spreads and a buildup of corporate debt, corporate stock buybacks financed through low-cost leverage, and the pace of lending in the CRE market.

Some participants judged that a prolonged inversion of the yield curve could be a matter of concern. Participants also noted that equity prices had exhibited volatility but had been largely flat, on balance, over the intermeeting period.

The chronically underreported inflation measure was, as expected, used as a pretext to justify the latest rate cut:

Many participants also cited the level of inflation or inflation expectations as justifying a reduction of 25 basis points in the federal funds rate at this meeting. Inflation had generally fallen short of the Committee’s objective for several years and, notwithstanding some stronger recent monthly readings on inflation, the 12-month rate was still below 2 percent. Some estimates of trend inflation were also below 2 percent. Several participants additionally stressed that survey measures of longer-term inflation expectations and market-based measures of inflation compensation were near historical lows and that these values pointed to the possibility that inflation expectations were below levels consistent with the 2 percent objective or could soon fall below such levels.

What happens if inflation does spike? All good, the Fed can raise interest rates in 15 minutes:

Against this backdrop, participants suggested that a policy easing would help underline policymakers’ commitment to the symmetric 2 percent longer-run objective. With inflation pressures muted and U.S. inflation likely being weighed down by global disinflationary forces, policymakers saw little chance of an outsized increase in inflation in response to additional policy accommodation and argued that such an increase, should it occur, could be addressed in a straightforward manner using conventional monetary policy tools.

On foreign influence on US monetary policy:

Low interest rates abroad were also considered an important influence on U.S. longer-term rates.

On waiting for more cuts:

Several also noted that, because monetary policy actions affected economic activity with a lag, it was appropriate to provide the requisite policy accommodation now to support economic activity over coming quarters.

On "makeup" strategies:

The staff also illustrated the properties of “makeup” strategies using model simulations. Under such strategies, policymakers would promise to make up for past inflation shortfalls with a sustained accommodative stance of policy that is intended to generate higher future inflation. These strategies are designed to provide accommodation at the ELB by keeping the policy rate low for an extended period in order to support an economic recovery. Because of their properties both at and away from the ELB, makeup strategies may also more firmly anchor inflation expectations at 2 percent than a policy strategy that does not compensate for past inflation misses.

On turmoil in the repo market :

developments in money markets "implied that the Committee should soon discuss the appropriate level of reserve balances."

On balance sheet expansion:

A few noted the "possibility of resuming trend growth of the balance sheet to help stabilize the level of reserves in the banking system" and several participants suggested that they could also benefit from "considering the merits of introducing a standing repurchase agreement facility."

And, so in three weeks, we went from "a few" to Powell making the decision to go ahead with NotQE.

And finally, the Fed is worried about a bubble

A few of the participants favoring an unchanged target range for the federal funds rate also expressed concern that an easing of monetary policy at this meeting couldexacerbate financial imbalances.

Sounds like the Powell Put just got removed.

***

Full Minutes Below:

Copyright ©2009-2015 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every time you engage ...

more