'Deflationary Undercurrent': Stock Market Update For The Week Ahead

The Past Week, In A Nutshell

What Happened: Last week ended negative on relative weakness from the technology sector.

Remember This: “August benefited from multiple tailwinds, resulting in one of the best Augusts on record. Those tailwinds look stretched and at risk, however,” said Brad McMillan, CIO for Commonwealth Financial Network.

“September is also historically one of the weakest months for the market, raising risks on a calendar basis, even before we consider the real possibility that the medical, economic, and market risks will reassert themselves.”

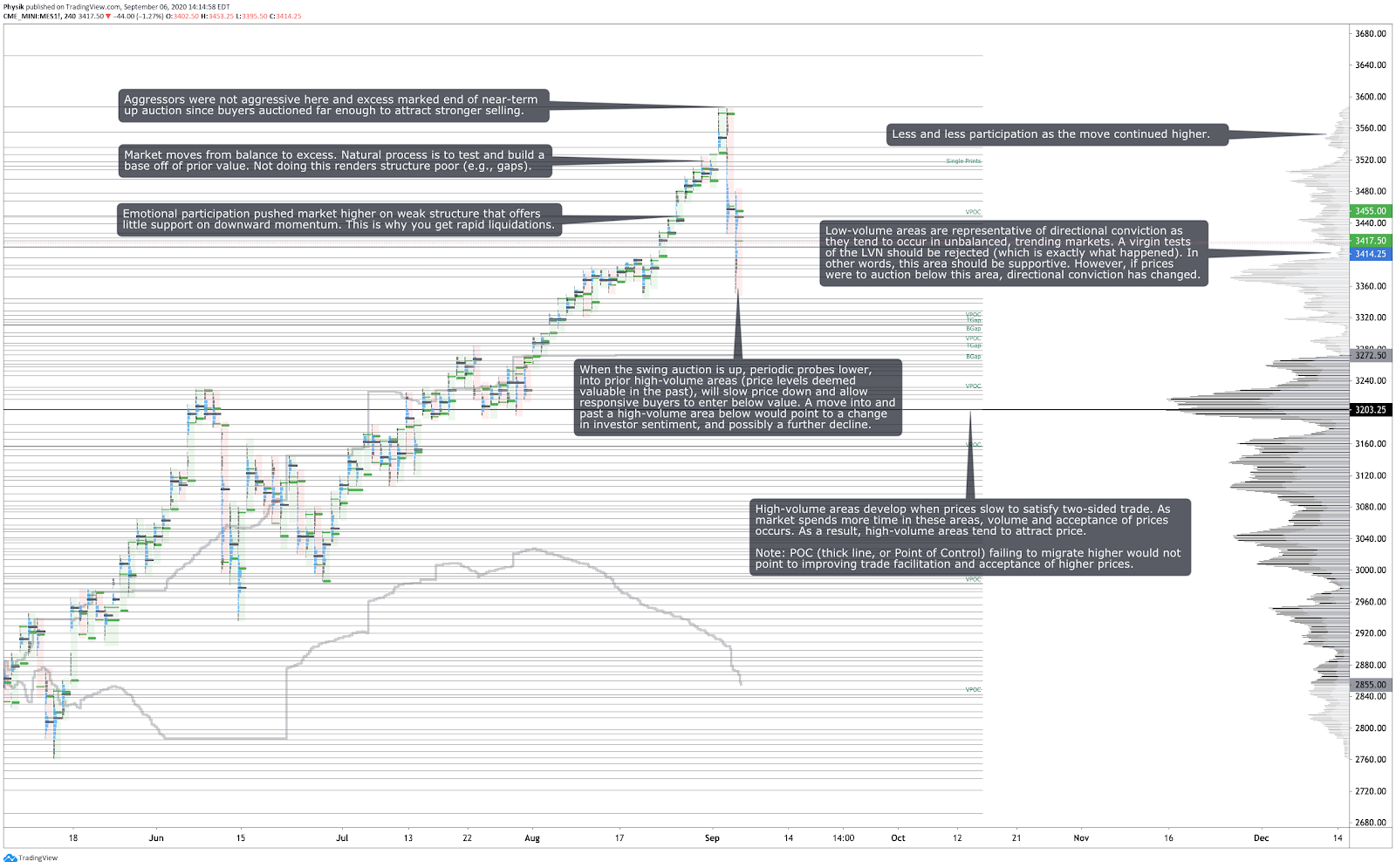

(Click on image to enlarge)

Pictured: Profile chart of the Micro E-mini S&P 500 Futures

Technical: Broad-market equity indices ended the week lower with the S&P 500 correcting nearly 7%.

Recapping Last Week’s Action: Alongside bets of an economic revival backed by prolonged central bank support, the S&P 500 established an overnight all-time high, prior to correcting lower, below value, and trading responsively into the close. On upbeat manufacturing data, Tuesday’s trade built on the prior day’s positive delta, finishing higher on a late spike.

Fueled by momentum in tech, Wednesday’s session opened on a gap, accepted the prior day’s spike, and placed initiative buyers firmly in control. After a brief test lower, regular trading discovered prices higher, leaving value and delta behind. At one point sellers finally entered and established excess on a spike high, suggesting the area could be resistive on subsequent tests.

Indices dropped overnight, Thursday, ahead of economic releases, catching up to the prior day’s divergent delta. After an open below the prior day’s excess, participants rejected higher prices and fueled an emotional liquidation that repaired numerous sessions worth of poor structure. In Friday’s auction, participants continued the push lower before rejecting the low-volume area at $3,400 on a virgin test, and rotating back to test the supply area near $3,460.

Overall, despite the speculative call-side activity in large technology names that forced dealers to hedge in the direction of the trend, prices did manage to auction high enough to attract stronger selling. Given the immense amount of poor structure created by the short-term, momentum-driven participation, it’s no wonder why the corrective action was so fierce.

Whether this sell-off is nothing more than a short-term inventory correction, the presence of additional poor structure below us, coupled with a mixed fundamental picture, suggests there may be more downside in play. That said, heavily-weighted index constituents are in an uptrend, while major market indices are in a short gamma, high-volatility environment.

Regardless of trend or volatility, it’s time to closely assess how far indices have come and the potential for further upside.

Scroll to the bottom of this page for non-profile charts.

Fundamental: Given the market’s strength going into the U.S. presidential election, ARK Invest CEO and CIO Catherine Wood suggested the multiple structure of the market will continue rising, given the deflationary nature of innovation.

“The P/E ratio of the S&P 500, right now, is at about 26 times on this year’s earnings and about 20 to 21 on next year’s earnings," said Wood. "Now, we should be looking into next year -- the market is a discounting mechanism. But, to the extent a correction makes people a little more focused on the short term, they’re looking at 26 times this year, and that typically has been the top of the market.”

“We’re in a deflationary world, thanks to the innovations that are sweeping through the world that are all deflationary in nature. You know the ones we talk about -- our five platforms -- DNA sequencing, robotics, energy storage, artificial intelligence, blockchain technology. As they sweep through the world, there’s going to be a deflationary undercurrent, even as unit growth is very rapid. That is highly positive for P/E ratios.”

Wood finished noting that investors may see multiples as high as 33 to 50 and near term corrections are a test of growth’s resilience in the new age of digital disruption and accelerated innovation.

Key Events: NFIB Business Optimism Index For August; Employment Trends; Consumer Credit; JOLTS Job Openings; TR IPSOS PCSI; PPI; Wholesale Inventory, Sales; Core CPI; Real Weekly Earnings; Cleveland Fed CPI; Federal Budget.

Recent News: Federal Reserve’s average inflation targeting underscores lower-for-longer rate view.

- Market prefers the continuation of Trump, but Biden win wouldn’t be negative.

- Illusions, Perceptions, and Reality: Discussing Stock Splits and Index Inclusions.

- What is next for markets? Investors should position for rising odds of Trump re-election.

- European Securities and Markets Authority warns of prolonged period of market risk.

- Berkshire Hathaway (NYSE: BRK-A) cut Wells Fargo & Co WFC stake.

- Canada added 245,800 jobs in August, but the pace of gains shows signs of slowing.

- Canada has big plans to use hydrogen to cut emissions and produce more oil.

- Demand for jet fuel in the U.S. is recovering faster than in many other markets.

- Three ways multilateral development banks can thrive after the COVID-19 pandemic.

- What the Pentagon’s report on China means for U.S. strategy -- including on Taiwan.

- Used car supply, demand to pressure auto lease asset-backed securities transactions.

- Credit implications of higher debt to depend on persistence of shock, policy buffers.

- Reduced steel quotas are credit positive for the U.S., but negative for Brazilian producers.

- California bans all flavored tobacco products, a credit negative for tobacco companies.

- Vanguard will convert its prime fund, the industry’s largest, to a government fund.

- Oil market’s rebalancing decelerated on slow consumption recovery, output slack.

- Analyzing differences between the 2000 tech-and-telecom bubble and 2020.

- U.S. employment growth slowed further in August and permanent job losses increased.

- Bank of Canada to revisit inflation-targeting, shadowing the Federal Reserve’s strategy.

- Amazon.com Inc AMZN plans to add 10,000 jobs in Bellevue, Washington.

- Moderna Inc MRNA could slow COVID-19 trials to add at-risk minorities.

- Re-evaluation finds Microsoft Corporation’s MSFT JEDI proposal is best.

- Larry Kudlow expects the Trump administration to unveil aid for airlines in weeks.

- AstraZeneca Plc AZN starts the final-stage trial of the COVID-19 virus vaccine.

- Nvidia Corporation NVDA taps Samsung, Micron Technology Inc MU for new gaming chips.

- U.S. factory activity accelerates as order data jumps to more than 16-½-year high.

- Airlines urge the U.K. and U.S. to start London, New York passenger testing trials.

- Carnival Corp CCL shares surge as cruises prepare to set sail this weekend.

- Pfizer Inc PFE sees virus vaccine data in the thick of the U.S. election fight.

Key Metrics

- Sentiment: 30.8% Bullish, 27.4% Neutral, 41.8% Bearish as of 9/2/2020.

- Gamma Exposure: (Trending Lower) 1,920,532,148 as of 9/4/2020.

- Dark Pool Index: (Trending Lower) 36% as of 9/4/2020.

Product Snapshot

S&P 500 E-mini Futures (ES) | SPDR S&P 500 ETF Trust SPY

(Click on image to enlarge)

Nasdaq-100 E-mini Futures (NQ) | PowerShares QQQ Trust QQQ

(Click on image to enlarge)

Russell 2000 E-mini Futures (RTY) | iShares Russell 2000 Index IWM

(Click on image to enlarge)

Gold Futures (GC) | SPDR Gold Trust GLD

(Click on image to enlarge)

Crude Oil (CL) | United States Oil Fund LP USO | Invesco DB Oil Fund DBO | United States 12 Month Oil Fund USL

(Click on image to enlarge)

Treasury Bonds (ZB) | iShares 20+ Year Treasury Bond TLT

(Click on image to enlarge)

Photo by Karolina Grabowska from Pexels.

© 2020 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.