When last I wrote, corporate credit was trading at extreme levels only seen during two or three brief periods in the last 30 years. At the time, we were extolling the opportunity to buy credit assets at historically cheap levels, and while we could not predict where the market would bottom out, we could be highly confident that the result would be positive for performance over a horizon of a year or more.

In the last couple of months, the market has come storming back faster than any of us could have predicted. Today, high-yield corporate spreads sit at nearly the same level as when the U.S. had its first known COVID-19 death on Feb. 28.1 That level is essentially the same as the historical average for the sector over the past 20 years, which begs a rather obvious question. Credit was the place to invest for right now … two months ago. But, is that still true today and into the future?

The short answer is yes. Eye-popping double-digit bond returns may no longer be an offer, but credit remains an attractive investment for the foreseeable future. Why? Well, there are a few reasons credit can be attractive at only average spread levels normally—and particularly so in the current market.

With Treasuries near all-time lows, there’s no alternative

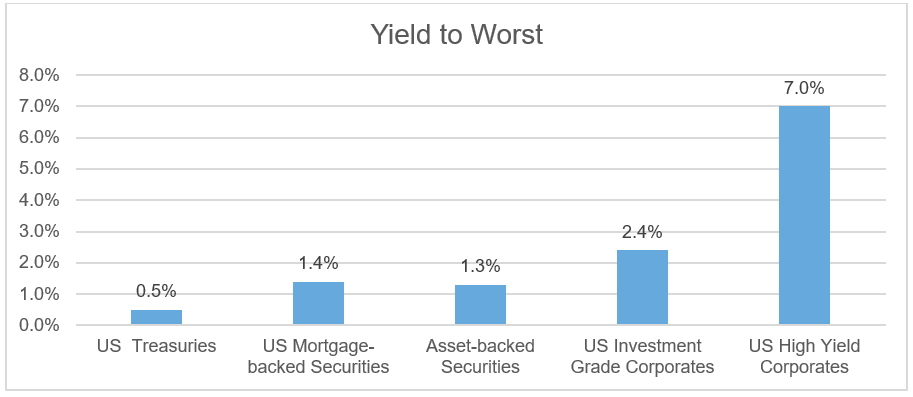

First, is the classic TINA argument. Investors, especially retirees, love income. And with U.S. Treasuries still at or near record lows, there is no alternative (TINA) to credit for generating meaningful income. Sure, we can quibble over the various flavors of credit and which is slightly more or less attractive, but the U.S. corporate market remains the most liquid and first stop for most investors reaching for yield in their portfolios. Until more juice is squeezed out of that market, many investors are going to see little reason to venture into more esoteric sectors with less policy support from the Fed.

(Click on image to enlarge)

Source: Based on Bloomberg-Barclays index data as of 5/29/2020

Favorable cyclical outlook

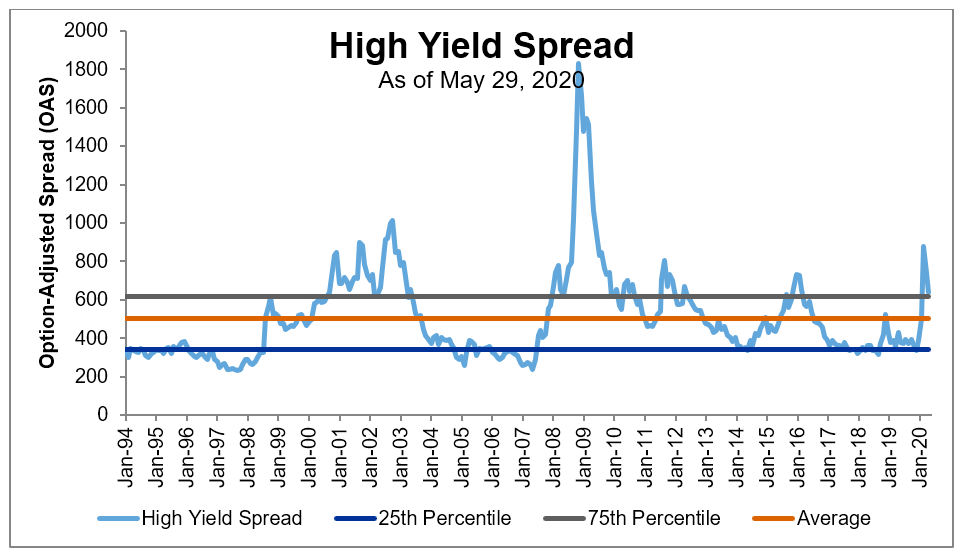

Next, we should think about why the credit cycle is called a cycle in the first place. It ebbs and flows like the tides. Typically, when it goes through the average heading up, it keeps right on going to a peak, as we saw in March. When it comes back through the average on the way down, it grinds lower for quite some time, clipping a coupon and additional excess returns over Treasuries along the way. So, while the valuation may be the same, the cyclical outlook for credit risk is very different depending on whether the average is being approached from below or, as is the case today, from above.

The latter would tend to imply more room to run ahead. Of course, we can’t fully discount the possibility of a double-dip in markets—as happened in the late 1990s and early 2000s—so it would only be prudent to hold less credit risk than a month or two ago. Still, the cycle favors continuing to ride some additional credit risk even at an average valuation.

(Click on image to enlarge)

Source: Based on Bloomberg-Barclays index data from 12/31/1993 to 5/29/2020

Compensation for defaults

Lastly, at average spreads investors are more than compensated for most plausible future levels of defaults. The nature of a risk premium like the credit spread is that it not only compensates you for the risk that bad things will happen (defaults), but also for the uncertainty about which companies that bad thing will happen to. That latter component is rather big for each individual bond. Thankfully, we have that most magical of forces known as diversification to help us out!

How? When you buy a broad and diversified portfolio, the uncertainty about who is going to default gets diversified away, yet you are still able to get all that yield in your portfolio. With skillful active management, you can perhaps even have fewer defaults than the broad market.

Using a back-of-the-envelope calculation, at a spread of roughly 500 basis points, or 5%, and an average recovery of 40 cents, defaults would need to be ~12.5% to eat up all that 5% cushion in a given year. That’s a high default rate versus history, though not implausible in a major recession. But, for anyone with an investment horizon longer than one year, the math starts to get more favorable the longer you look out. That 5% spread is annual, so recessionary default rates have to keep happening, which is far less plausible.

All of this lends further support to continuing to hold a diversified exposure to corporate credit in bond portfolios—for now, and into the foreseeable future.

1 The spread of the Bloomberg-Barclays U.S. High Yield Index on that date was 500 basis points versus 536 basis points on 6/8/2020. Note also that subsequent post-mortem analysis has found earlier deaths in the U.S. due to COVID-19 that were not known at the time.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and ...

more

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

The Bloomberg Barclays U.S. Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2020. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11689

Disclaimer: Opinions expressed by readers don’t necessarily represent Russell’s views. Links to external web sites may contain information concerning investments other than those offered by Russell Investments, its affiliates or subsidiaries. Neither Russell Investments nor its affiliates are responsible for investment decisions with respect to such investments or for the accuracy or completeness of information about such investments. Descriptions of, references to, or links to products or publications within any linked web site does not imply endorsement of that product or publication by Russell Investments. Any opinions or recommendations expressed are solely those of the independent providers and are not the opinions or recommendations of Russell Investments, which is not responsible for any inaccuracies or errors.

Investing in capital markets involves risk, principal loss is possible. There is no guarantee the stated outcomes in the presentation will be met.

This is a publication of Russell Investments. Nothing in this publication is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The contents in this publication are intended for general information purposes only and should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional concerning your own situation and any specific investment questions you may have.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

less

How did you like this article? Let us know so we can better customize your reading experience.