Biotechs Feel The Bern

- Healthcare is entering a period where election cycle impact will grow.

- The Medicare for All healthcare plan will begin to get factored based on the success of the proponents in the primary election cycle starting next week.

- Different segments of healthcare will be impacted differently.

- No need to assume the worst-case scenario.

- Biotechs & healthcare overall can witness a spike in volatility, but opportunities exist.

Healthcare Pulse

The market doesn't like uncertainty.

And when you think about healthcare, that uncertainty is immediately magnified.

Fundamentally, healthcare couldn't be better positioned, with an aging America, rapidly advancing therapies, a faster-moving FDA, easy access to risk capital, and healthcare spending growing to 1/5th of GDP, as discussed in the Biotech Bonanza 2020 Outlook.

However, healthcare is at a critical point in this election year as the outcome can possibly set in motion a restructuring of the industry. As the primary election season is about to get underway, this appears to be an appropriate time for a quick update on a major healthcare investing issue.

The healthcare sector has the dubious honor of being the hottest potato this election cycle, giving the fossil fuel industry and the banking industry a little breathing room from the political onslaught.

So, with this backdrop, healthcare valuations are going to be heavily influenced in 2020 by political considerations. Although the country is still in the early stages of the election cycle, the dynamics are shifting and sub-trends are beginning to emerge as the Democratic field is narrowing.

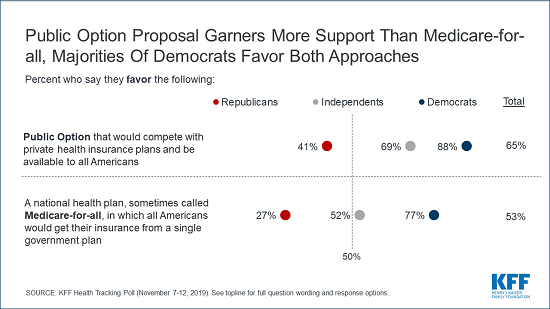

The primary elections kick-off on February 2 and the slate of candidates have proposals that will all materially expand public healthcare access and how it's provided for in America. But some candidates have proposals that are much more far-reaching than others. The one with the most far-reaching proposal and timeline to implement is Senator Bernie Sanders, who intends to shift healthcare to a universal healthcare system referred to as Medicare for All. Senator Elizabeth Warren also supports Medicare for All, but over a phased-in period of 2-to-4 years.

Medicare for All

The Medicare for All healthcare system is envisioned as a single-payer system. This means there will be one national, tax-financed, healthcare insurance plan. It will be the single-payer entity responsible for receiving the premiums, through specific taxes, and distributing the payments to healthcare providers. This single-payer system will get rid of administrative layers and take over the roles of health insurance companies and employers in delivering healthcare coverage.

Most variants of Medicare for All plans have key similarities, as outlined by healthcare researcher Kaiser Family Foundation. They are tax-financed, replace private health insurance, have a lifetime enrollment unaffected by retirement, and no separate premiums. There are nearly 28 million uninsured Americans who can finally be covered, and so will be the many underinsured within the private health insurance market who can't afford the costs and underuse healthcare, as per a December 2019 study by JAMA.

With employer-based family healthcare average cost rising to nearly $20,000 annually, there are many who find the plan appealing. This is reflected in the surge of the two most prominent candidates for Medicare for All - Senator Elizabeth Warren in Sep 2019 and Senator Bernie Sanders now in Jan 2020. But there will be significant Federal government costs as well associated with such coverage, and the healthcare sector will go through a major restructuring, in the process recasting many segments. All this breeds uncertainty.

Nearly all plans by other Democratic candidates support Medicare for All with a public option. This means the same Medicare for All plan will be provided as another available option on the menu joining the other existing private insurance plans in the market.

Will Biotechs Feel The Bern?

Since last week, multiple polls in more than one state are showing Senator Sanders surging and even acquiring front-runner status in some polls. His supporters fondly refer to his movement as feeling the Bern.

Strictly from the standpoint of the healthcare valuations and nothing to do with the merits of the Medicare for All plan, Senator Sander's proposal will be the most aggressive in changing the industry structure. Consequently, it will create more uncertainty relative to other plans.

In our opinion, biotechs will feel the burn.

And so will many other industry groups within healthcare, like pharmaceuticals, health insurance, managed care, hospital operators, with some feeling the burn more than others.

The big question is when to adjust the portfolio exposure to healthcare in what will now be a politically volatile period for the rest of the year.

If next Mon, Feb. 3, Sanders wins Iowa, the first polling state, and then New Hampshire a week later, building up momentum heading into a 10-day period from Feb 29 of delegate-rich contests, healthcare valuations can begin to display signs of anguish and higher volatility. Although it certainly won't be a call for the exits as the road is still long and frontrunners change often.

Also, some context to the Medicare for All debate is important.

What also has to be asked is if Medicare for All can really happen in one fell swoop?

Even with all its merits, it may not be possible to shift to Medicare for All unless there is broader support. We believe the passage of such proposed legislation is not as relatively straight-forward even after winning a Presidential election, which itself is a complex and uncertain battle. Medicare for All in its entirety may perhaps not even be possible in 2021 as it will require the approval of Congress. At this stage, it doesn't even appear that all the House and Senate members of even the Democratic party are on board with the Medicare for All plan. Although that can change if a majority of public opinion supports it.

Perhaps Medicare for All is a road that will begin to be traveled after this election, but most likely won't be a destination reached immediately.

How will Healthcare react?

Last September, when Senator Warren with a similar plan was ascendant in the polls, the healthcare sector experienced a period of sharp volatility which was overcome as Warren's poll numbers slipped, and some favorable industry events occurred.

Healthcare is diverse. The various segments are exposed differently towards Medicare for All.

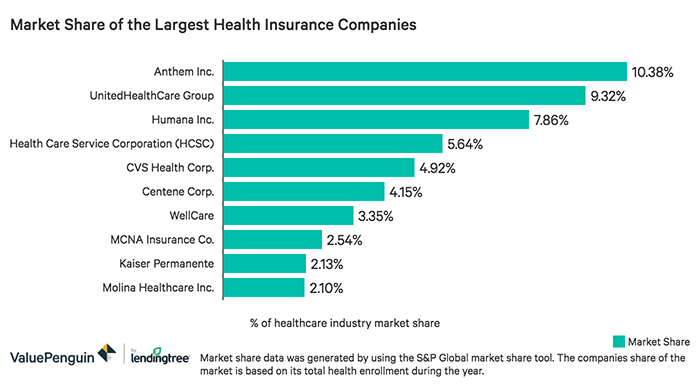

The industry groups that will feel the pain much earlier than others, for the consequences are existential for them, will obviously be the healthcare insurance and managed care providers. These will be companies like Anthem, UnitedHealth Group (UNH), Aetna (CVS), Cigna (CI), and Humana (HUM).

Hospital operators like HCA Healthcare (HCA) and Tenet Healthcare (THC) will benefit from rising demand although there will be some offset from reduced rates as Medicare reimbursement rates are typically lower than private insurance rates.

Biotechs and pharmaceuticals (biopharma) are affected by the pressure that will be exerted on drug pricing as the national health plan will acquire the role of a direct negotiator on behalf of the patients. This is a risk that has been growing even without Medicare for All. The pressure continues to increase to empower the Centers for Medicare and Medicaid Services ((CMS)) the authority to negotiate prices directly with the pharmaceutical companies. In fact, the recently passed House Bill, H.R. 3, last December includes that power to CMS to negotiate drug prices for at least 50 to up to 250 drugs. Although the bill will not make much progress in the Senate, there are other bills being worked upon there to address healthcare costs.

The drug pricing issue has been casting a long shadow over biopharma for a significant length of time. The primary elections will most likely elevate uncertainty and raise volatility. However, in our opinion, such volatility should be transitory in the earlier stages, till such time a more concrete nomination result is available clarifying the nature of the Democratic healthcare plan.

Conclusion

The broader market is experiencing general uneasiness around the unmitigated spread of the Wuhan strain of Coronavirus and its possible escalation to a pandemic designation by the World Health Organization (WHO). This would mean we may experience some nervous days in early February.

But we feel that the market is also poised for a sharp rally if there is any positive news suggesting that the Coronavirus may have peaked and is spreading at a slower rate. Just like influenza (flu), the Coronavirus is highly contagious, but not as fatal as influenza which kills thousands each year in the US. Coronavirus does appear to have a lower mortality rate suggesting it may not be as deadly as similar viral outbreaks in the past, like SARS. Similar to influenza, people with pre-existing conditions, aged, and very young, are most at risk. Healthier people are very likely to recover. The anxiety comes from the novelty of the Coronavirus and the fact that we don't have a targeted cure yet. But that's a matter of time.

Which industry is relatively insulated from the potential disruption of the Coronavirus?

Biotechnology would be one such industry.

In fact, one can also make an argument that healthcare, in general, is better off relative to other sectors when it comes to managing any economic disruption that may result from the Coronavirus.

However, in our opinion, healthcare and biotech fortunes near-term may be predicated on the outcomes of the primaries. Healthcare investors should prepare for likely bouts of higher volatility in the earlier part of February.

The Democratic primary season is from February 3 to June 16. Most likely, the Super Tuesday (Mar 3) primary voting, when 14 states vote, and the 10th March elections, when 6 states vote, can clarify the race leader with the best chance for a Democratic nomination.

At the same time, the first two contests will provide early signs of momentum. If Senators Sanders or Warren win or are a close second in the first two elections (Feb 3 & 11) then the volatility can increase for healthcare. By the same token, if former Vice President Joe Biden, with a relatively less aggressive healthcare plan, has strong early successes then from an investor standpoint that will be a positive development, ahead of the contests in March.

It doesn't appear to be a time for either aggressive buying or panic selling. Some discretion is prudent, based on your investment objective and outlook. We had turned cautious in mid-January and subsequently reduced our exposure to varying degrees in the Prudent Biotech, the Prudent Healthcare, and the Graycell Small Cap model portfolios. It is a difficult time to reduce exposure for there are many attractive ideas for a healthcare and biotech portfolio. We will adjust higher if the situation clarifies favorably in the early contests and the market correctly decides to disregard the primary election events this early-on and wait for the final nomination.

It will also be helpful to keep in mind that after a primary election, policy plans undergo a revision as the winning candidate shifts towards the center or mainstream. So whether it is Medicare for All or Medicare for All with a public option, in the end, what would be possible will be a plan with the requisite votes in Congress. Most likely in a Democratic victory, it will be a meaningful expansion of Obamacare. But we don't have to think so far out yet.

Some of the attractive portfolio ideas, which may be now or in the past part of our model portfolios, include Vertex Pharmaceuticals (VRTX), Alnylam Pharmaceuticals (ALNY), Nevro (NVRO), NovoCure (NVCR), Seattle Genetics (SGEN), Mirati Therapeutics (MRTX), Reata Pharmaceuticals (RETA), BioMarin Pharmaceutical (BMRN), Sarepta Therapeutics (SRPT), Acadia Pharmaceuticals (ACAD), Deciphera Pharmaceuticals (DCPH), Kodiak Sciences (KOD), CRISPR Therapeutics (CRSP), uniQure (QURE), Aimmune Therapeutics (AIMT), Amarin (AMRN), Zymeworks (ZYME), Karyopharm Therapeutics (KPTI), Axsome Therapeutics (AXSM), Karuna Therapeutics (KRTX), Principia Biopharma (PRNB), Momenta Pharmaceuticals (MNTA), Fulgent Genetics (FLGT), Apellis Pharmaceuticals (APLS), Arvinas (ARVN), Aurinia Pharmaceuticals (AUPH), Moderna (MRNA), Neogenomics (NEO), Radnet (RDNT), Provention Bio (PRVB), and TG Therapeutics (TGTX). Some hedging can be done using bullish and bearish ETFs.

Always take a portfolio approach to overcome mistakes.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.