Best Retirement Stocks For 2020

The best retirement stocks will provide a combination of a steady stream of income (dividend) and stock value stability. While some retirees prefer high yielding stocks, I tend to pick companies with a 4-5% yield along with a decent dividend growth rate. In a rare occasion, you will find retirement stocks with a 6%+ dividend growth rate that will assure you to not only keep up with inflation but rather increasing your paycheck at retirement.

The following article will present 3 of the best retirement stocks you can find for your portfolio in 2020. They are leaders in their markets and show strong dividend growth potential on top of being generous with their shareholders.

The selection methodology of those companies is explained in this article: What a Dividend Growth Investor Buys in 2020?

Let’s take a look at the best retirement stocks for 2020:

Dominion (D)

Market cap: 66B

Yield: 4.58%

Revenue growth (5yr, annualized): 0.37%

EPS growth rate (5yr, annualized): 5.00%

Dividend growth rate (5yr, annualized): 8.22%

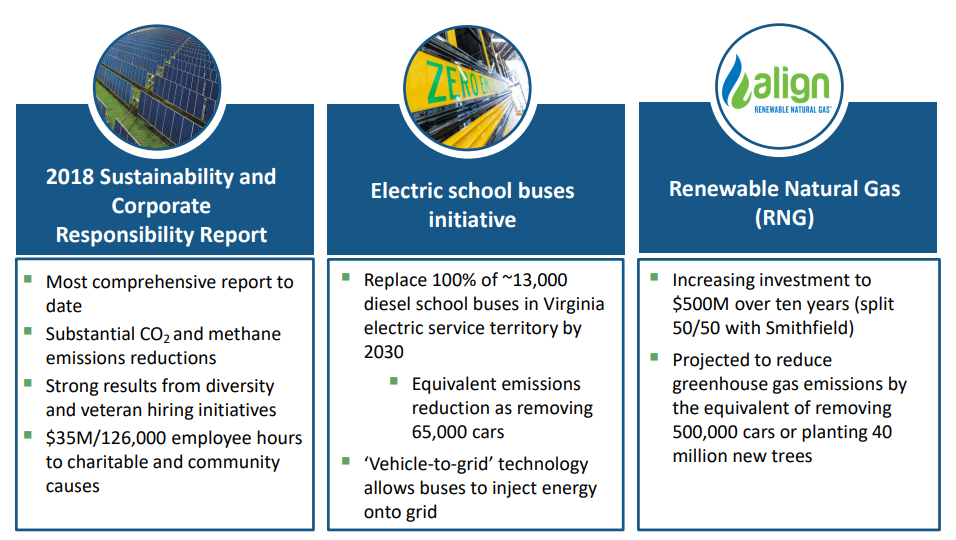

Dominion is one of the largest utilities in the U.S. and still pays a generous yield (around 4.30%). The company has predictable revenue streams as 95% of its income is coming from regulated assets. Growth is on the table as management intends to invest $26B between 2019 and 2023. Such growth plans are expected to generate EPS growth of 5% annually. What I like about all this is that D focuses on “green” projects.

Source: Dominion investors presentation

Dominion also owns a 48% stake in the Atlantic Coast Pipeline (ACP). The ACP, now estimated to cost $8 billion, is a natural gas transmission line that will run from West Virginia to North Carolina, passing through Virginia. Partners in the ACP are Dominion (48%), Duke Energy (47%), and Southern Co. (5%). Dominion will construct, operate, and manage the ACP. There are obvious legal concerns around this project, but management teams seem confident overall. This will become another strong revenue stream for all participants as they signed long-term contracts (20 years) for the pipeline capacity.

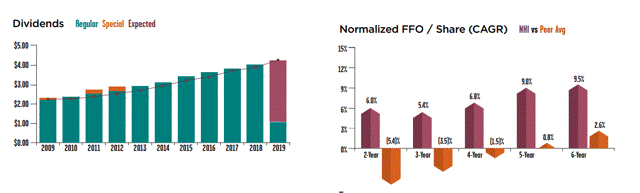

The dividend payments have been increasing significantly over the past 5 years (+42%). We expect a high single-digit to mid-single-digit dividend growth rate in the future. Considering the current yield, this is definitely better than buying a “deluxe bond”.

Broadcom Inc (AVGO)

Market cap: 126.3B

Yield: 4.10%

Revenue growth (5yr, annualized): 39.55%

EPS growth rate (5yr, annualized): 39.09%

Dividend growth rate (5yr, annualized): 53.60%

Broadcom is in a bowl of growth. It manufactures one of the best RF filter, used by all high-end smartphones to improve connectivity. Companies like Apple would not risk their connectivity, right? AVGO’s large size brings economy of scale and enables it to build millions of filters. Its growth-by-acquisition strategy has turned it into an expert in integrating companies. In a decade, AVGO went from $2 billion to nearly $18 billion in sales. Finally, its technology will be required in the next decade. The growth of the IoT and the rise of artificial intelligence applications are just examples.

Broadcom isn’t a classic dividend payer. It needs lots of cash to finance its fast growth and its R&D to keep its edge. Still, it shows 9 consecutive years with a dividend increase and went from a yield below 1% to 3.8% in a few years. In 2016, the dividend was $0.51/share and is now $3.25. While the payout ratio seems quite hectic, the cash payout ratio is under control. You can expect future increases.

National Health Investors (NHI)

Market cap: 4B

Yield: 5.09%

Revenue growth (5yr, annualized): 20.12%

FFO growth rate (5yr, annualized): 9%

Dividend growth rate (5yr, annualized): 6.64%

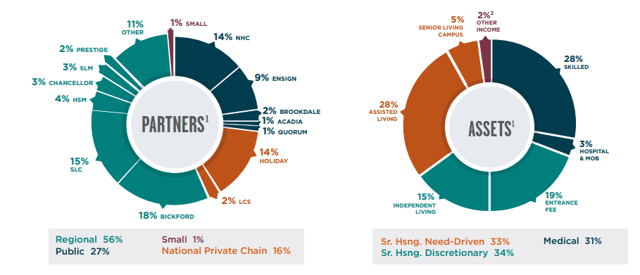

NHI just appeared on our Mike’s Buy list not too long ago. What just happened to National Health Investors (NHI) on the market is just a classic story. The REIT started its earnings report by beating both Funds from Operations (FFO) (+2.1%) and revenue growth expectations (+9%). Unfortunately for current unitholders (but fortunately for you if you are looking for an addition in this sector) management also issued weaker guidance than expected. The Company’s guidance range reflected the existence of volatile economic conditions as well as the impact of three non-performing leases which account for less than 1% of their third-quarter 2019 revenues.

Source: NHI investors meeting presentation

I like REIT’s great partners and their asset diversification. This ensures that NHI will continue to generate steady cash flows even if there is some bad news coming from one of their tenants. The REIT typically enters into long-term leases with attractive renewal options and annual lease escalators based on inflation. This REIT has a long history of generating higher FFO growth than the industry. When I select a company for my portfolio, I like finding leaders in their market. NHI is well-positioned to surf on the U.S. aging population phenomenon for many years.

Disclaimer: Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full access to 12 real-life portfolio models, readers can also ...

more