A Generational Dose Of Financial Reality

Financial wellness is difficult to achieve without steeled resolve for fiscal self-preservation and an endlessly skeptical nature about the information provided by mainstream financial media.

You as a saver, investor, and commander of assets and liabilities that steer the household balance sheet toward achievement of financial milestones such as retirement planning, must carefully navigate popular financial advice which has progressively morphed into statistical click-bait.

The stock market is sliced and diced to present its prettiest façade. Investing time frames that I argue best fit the lifespan of vampires not humans indeed connect to consistent double-digit returns.

Statistical foreplay makes it easy to promote risk assets like stocks as the solution to every financial ailment. I posit this sentiment is fueled hot by overconfidence, a backstop provided by a Federal Reserve that listens to and fears market downturns and recency bias as professionals have forgotten the damage created by bear market cycles.

New advisors and brokers are convinced that bear markets are occurrences of the past and trained by their big box brokerage allegiances to perceive them as great opportunities. For young investors market derails may be opportunities; especially for those who are in accumulation mode and seek to purchase stock shares at lower prices. For people near or in retirement who require investment account distributions, a bear market can be devastating to the longevity of portfolio assets.

When (if) bear markets occur, every investor trades time for dollars. So, what is your time worth? How much of your overall portfolio should be allocated to stocks if you consider how long it may take to make up for losses? If you consider risk first, reward second, especially at a time when market valuations portend to lower future returns, outside of the media telling you to “eat your stocks!”, what do you believe is right?

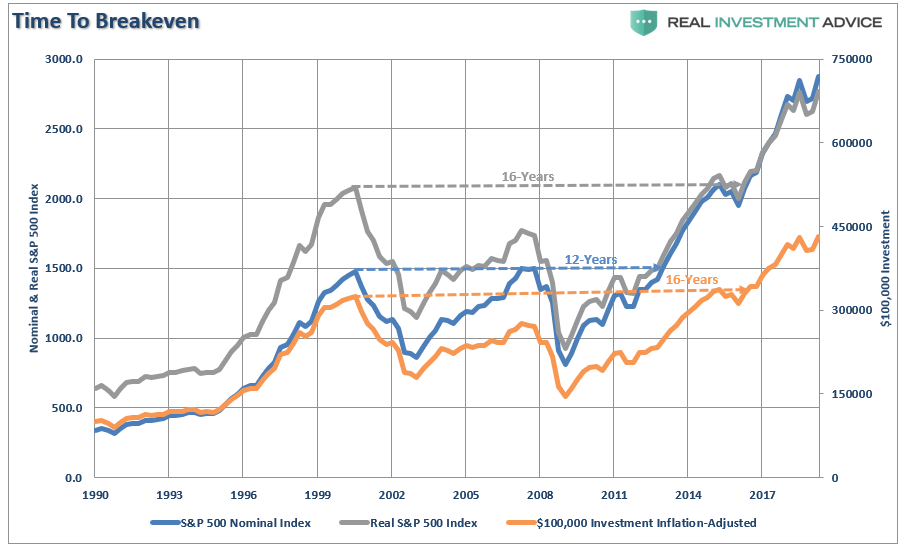

Search for the truth. It’ll crystallize sane thoughts. Understand how long it can take to break even from market disconnects and decide accordingly.

I’ve been studying individual stocks since I was 16. When I was 12 years old, I called the Dreyfus mutual fund company to receive information on a money market named Dreyfus Liquid Assets (ironically, I worked for Dreyfus from 1990-1998).

At that time, I recall the fund had a hefty front-end load to invest. Yes, a money market fund with a front-end charge! We’ve come a long way. I realized I was way over my head as I labored through voluminous square-stapled pages comprised of paragraphs in very small type. Each word came across as important. Although I comprehended a mere 2% of what I read, the exercise along with studying stocks helped me to realize that money is deadly serious and downturns in markets and flowery fabrication of long-term market returns should be taken seriously too – which is one reason I teamed up with Lance Roberts who I believe communicates money truth for today’s market and macro-economic conditions.

Please don’t misunderstand me – Stocks are indeed part of an overall lifetime financial strategy – they’re just not the solution to every financial shortfall. Even if they are the best answer, valuations and time frames as head or tailwinds to success of the asset class must be considered as a practical measure when helping investors meet long-term financial milestones.

I recall a period in my career when a blended portfolio of 60% stocks, 40% bonds provided solid double-digit returns. Over the last 20 years, the same asset mix, similar risk provided returns in low-to-mid single digits. I deem it a stealth financial repression.

Let’s imagine I’m 25 and save consistently for 40 years in an S&P 500 Index Fund; using past performance through December 2018 as a guide, I may achieve an annualized return greater than 11%. Not shabby. My beef with mainstream financial media is not their certainty of future rosy returns more than it is the financial reality today which prevents people from investing consistently for 40 years.

For example, many households have still not recovered financially from the Great Recession. A recent nationwide Bankrate survey discovered that 48% of Americans who were adults when the recession began in 2007 have seen no improvement in their financial situation. How does one save for the long-term to take advantage of market returns for 40 or 50 years if this is their present state?

Vanguard’s 2019 edition of their How America Saves analysis breaks down the behavior of 5 million participants in 1,900 defined contribution plans (most of them 401ks), they administer.

My beef on occasion with Bankrate is their sample size is too small – roughly 1,000. Although I do admire their initiatives to measure the pulse of the financial distress still prevalent in America that most outlets are reluctant to discuss. Vanguard casts a wide net as a lead provider of defined contribution plans.

In 2018, the average account balance for Vanguard participants was $92,148. The median balance was a paltry $22,147. For those 65 and older, Vanguard found these average balances at $192,877 with the median being a woefully deficient $58,035.

Something is broken. Now you know why I focus much in my writing about the importance of making smart, unemotional decisions about Social Security which is now America’s primary pension.

Today, I meet with individuals and couples – Millennials, Generation X’ers – I teach 20-something Gen Z young adults about financial basics; I wonder how in reality they’re going to be able to invest interrupted for 40 years, especially when more of the risk of saving for retirement and healthcare cost burdens are incurred by the employee, not employer.

Although wage growth has improved over the last 12 months, in real (inflation-adjusted) terms, median annual income is only $674 higher than it was in the beginning of 2008, according to Sentier Research.

I am encouraged by the fiscal habits of Generation Z, those born after 1995. They are aggressively price conscious with purchase decisions, seem to master the temptation of immediate gratification, save money at a higher rate than previous generations and are even willing to discuss formal financial planning.

I pray I’m dead wrong. However, based on how I assist young generations prioritize (juggle) their saving, debt and investment goals, without consistent, inflation-adjusted wage growth and strong resolve to live below their means, I am having a challenge envisioning how this group saves interrupted for two decades, let alone four.

If I’m correct, stock returns just due to lack of time invested in markets may be closer to 6.5%; if current valuations are considered then maybe returns are closer to 3%. Unless wages consistently increase which could allow for heftier savings and investing rates, Gen X and Gen Z populations are going to require information that’s based more on their reality than the ancient history of euphoric fiscal tailwinds that Baby Boomers faced in the 80s and 1990s.

I don’t believe the financial industry is up for the educational task nor the noble responsibility to align with the financial reality that younger generations are going to encounter. The focus would be less of an emphasis on stocks as a wealth-building tool or full-on retirement savior. Imagine?

Portfolios will need to include longevity insurance or annuities to replace lost pensions. These structures should only be offered if holistic, lifetime financial planning suggests they’re warranted.

I’m afraid it’ll be best for the industry to stick with lush memories of big returns derived within the expanse of semi-centennial stock investing.

Limited information which details the impact of bear markets may scare young generations away from stocks forever once 30%+ losses become part of their reality. I observe how risk-averse Generation X and Z tend to be; perhaps an imprint of their not so prosperous recollections of what their families went through during the financial crisis and the hardships they’re still experiencing. After all, breaking even is a b*tch as I meet with investors today who haven’t recovered from losses incurred during the Great Recession. Not just stock losses. There remains a drag on wages, which is worse.

It’s time for financial professionals to align with the mindset of these generations – help them focus on the basic skills required to create robust financial balance sheets. Help them to combat financial fragility by focusing on the benefits of building and maintaining emergency cash reserves as a priority over retirement accounts, debt control, small mortgages and the benefits of health savings accounts. It’ll be a refreshing change from myopia over the so-called magical financial elixir that only seems to be manufactured on Wall Street in the form of stock investing.

As fiduciaries, we can’t afford to be so narrow-minded.