3 Ways To Be Your Own Financial "Superhero"

The latest in the Marvel movie portfolio, Avengers: Endgame, has blown away every theatre attendance record. The film has earned $1.48 billion on a global level (as of this writing).

There’s little doubt that humans love heroes, especially super-human types. We relish the conflict between good and evil. We cry when our heroes face setbacks and applaud when they gain the upper hand on the enemies because if we were superheroes, we’d fight dark forces and win, too.

We also get a bit overzealous and scream “take our money!” when our Avengers with all their special talents, are also all too human. They love, feel loss deeply, they’re sort of funny, seek revenge and as passionately overcome obstacles to right the wrongs which hurt their own and innocent people.

To become a financial superhero, one must take to heart-specific disciplines. There’s no fanfare, no grand battles; you won’t save an entire universe. The little piece of the world you call your own, however, will be better off. The greatest of accomplishments come from the smallest, consistent actions.

Here are 3 financial superpowers that are easy to cultivate.

Pay Yourself First – Aggressively.

I’m not a fan of personal finance dogma. Many of the stale tenets preached by the brokerage industry are part of a self-serving agenda to direct retail investor cash into cookie-cutter asset allocation portfolios, all to appease shareholders.

Whether communicated across a broker’s desk or broadcast by financial personalities in mainstream media, these myths persist with the hope you’ll continue to fall for them. Perhaps you’re too busy living life to investigate further. Maybe you’re not as suspicious as I am. Someone who was employed by an organization that cared first about selling product. For some, unfortunately, it’s just plain ignorance to continue to fall for silver-tongued money traps.

For example, a well-known financial showman was lamenting, stretching the meaning (again) and hitting sound effect buzzers over this pearl called the “Rule Of 72.”

As a reminder, the Rule is a method to determine how long an investment will take to double given a fixed annual rate of interest. Just divide 72 by an annual rate of return.

When working with low rates of return, interestingly, the rule is precise. As returns increase, the rule gets less precise per Investopedia.

Yet, this rule is bandied about when it comes to stock investing where rates of return are anything but fixed.

Perhaps, the Rule Of 72 should be reworked to consider how long it may take to recover from investment setbacks.

Could it be plausible that it may take 72 years to fully utilize losses incurred during the tech bubble and the financial crisis?

Hey, that’s nowhere near as farfetched as applying the Rule to volatile investments.

When you come across Rule Of 72 (and if you haven’t yet, you will), I need you to remember that it only holds water for fixed, low rates of return which clearly dismisses stocks as part of the equation.

One rule I’m happily a complete sucker – Pay Yourself First. It’s not just a good one. It’s the core, the very foundation, of every strong financial discipline. Why? Paying yourself first, whereby dollars are directed to savings or investments before anything else, reflects a commitment to delayed gratification. An honorable trait that allows the mental breathing room to avoid impulse buys, raise the bar on savings rates and minimize the addition of debt.

Per Ilene Strauss Cohen, Ph.D. for Psychology Today, people who learn how to manage their need to be satisfied in the moment thrive more in their careers, relationships, health, and finances when compared to those who immediately give in to gratification.

Again, the root of Pay Yourself First is delayed gratification; the concept goes back further than some of the concepts the financial industry has distorted just to part you from your money. People who syphon 20-40% of their annual gross income consistently year after year, no matter what, are true superheroes of family household wealth.

Think Roth 401k, Roth IRA, Roth conversion before all else.

Forget what you’ve read or heard about the alleged benefits of pre-tax retirement accounts – just for a few minutes. You are acquainted with the pre-tax savings mantra. It’s been force fed to the masses by finance and tax pros for decades. The reduction of current tax liability, years of tax-deferred compounding. I mean, what’s not to love, right?

But, wait.

At retirement, we’ve been told that we’ll happily ever after within the lowest marginal tax rate. For some people, this is the case. However, for most pre-retirees, we witness firsthand the long-term financial damage of sheltering every retirement dollar in pre-tax accounts and the negative impact of ordinary income taxes on distributions.

What’s rarely considered are a few important points (your broker is primarily focused on the accumulation of dollars in managed accounts and not concerned about the tax impact you may suffer when it’s time to distribute tax-deferred dollars to meet expenses):

- Most likely, you will not drop to a lower tax bracket in retirement. Nobody knows where tax rates are going; although I’ll make a solid guess that future projections must move higher due to fixes required to entitlements such as Medicare along with other rising costs of an aging population. When the taxation of Social Security retirement benefits is considered, there’s a high probability that the ordinary income tax distributions from pre-tax accounts are going to generate an additional tax burden that rarely gets considered unless a person’s overall retirement distribution strategy is analyzed.

A married couple filing jointly with provisional income (a convoluted mix of ordinary income, tax-exempt income & ½ Social Security benefits), within the threshold amounts $32,000-$44,000, must add to gross income the lesser of 50% of Social Security benefits or the amount by which provisional income exceeds the threshold amount. Provisional income over $44,000 raises the percentage to 85%. Retirees must pay attention to the marginal tax rate danger zone where Social Security benefits are not fully taxed at 85% yet provisional income is high enough to trigger additional tax. A marginal tax rate danger zone is the point where each additional income dollar has the potential to be taxed at $1.50 or $1.85. For example, if married filing jointly, the 12% marginal tax bracket threshold is $78,950. However, depending on Social Security income received, (the average benefit is $33,456), a retiree can experience a tax rate as high as 22% on each additional dollar above Social Security provisional thresholds.

Per CFP Elaine Floyd’s tremendous work examining this insidious bracket creep, $30,000 in annual social security income along with $17,000-$59,000 in modified adjusted gross income (not counting Social Security), can cause your marginal income tax rate to increase to as much as 22%. Roth accounts being 100% tax-free on withdrawals, do not get added to the provisional income equation (even though tax-exempt or municipal bond income does!).

A retiree may delay the receipt of Social Security benefits until age 70. This decision will lead to greater lifetime income due to the delayed 8% annual retirement credits which accrue every month from FRA or full retirement age until age 70. Concurrently, a recipient can reduce a future tax burden on benefits by drawing down an IRA or 401(k) account to fund retirement living expenses.

Currently, we plan for many clients to initiate annual surgical Roth conversions along with coordination of distributions for living expenses to accelerate the reduction of IRA or 401(k) balances prior to mandatory distributions at age 70 ½. It’s important that your financial partner and tax advisor work together to ensure that the upper limits of your personal tax rate aren’t exceeded. For example, if you and your spouse require $4,000 a month to meet living expenses, even with taxes withheld there’s still ‘bandwidth’ in the 12% bracket to complete a surgical Roth conversion. You want to make sure you have enough cash outside your IRA to pay taxes on conversion dollars.

- If you follow a Pay Yourself First strategy, in almost every case a Roth is a better choice. I’m not concerned about your current tax bracket; nor am I worried about your possible tax bracket in retirement. I do care about how you’re going to gain more consumption dollars in retirement and the impact of taxation on Social Security benefits. John Beshears a behavioral economist and assistant professor of business administration at Harvard Business School in a study – “Does Front-Loading Taxation Increase Savings?: Evidence from Roth 401k Introductions,” along with co-authors, outlines that plan participants who place their retirement savings on auto-pilot and direct a percentage of gross income, say 10%, into a Roth vs. a traditional pre-tax 401k, will wind up with more dollars to spend in retirement.

It’s rare when a financial rule-of-thumb is a true benefit. And you don’t need to do much to receive it! The reason the strategy works is front-loading of taxes. In other words, sacrificing tax savings today (when working and paying the taxes isn’t as much of a burden as it would be in retirement when earning power drops dramatically), and failing to adjust the percentage of auto-pilot savings to compensate for the current tax impact of switching from pre-tax to Roth, allows for additional future consumption dollars.

From Lauren Lyons Cole Business Insider article on the study:

“If a worker saves $5,000 a year in a 401(k) for 40 years and earns 5% return a year, the final balance will be more than $600,000. If the 401(k) is a Roth, the full balance is available for retirement spending. If the 401(k) is a traditional one, taxes are due on the balance. Let’s say the person’s tax rate is 20% in retirement. That makes for a difference of $120,000 in spending power, which a life annuity will translate into about $700 a month in extra spending.” John Beshears

Create and respect your financial boundaries.

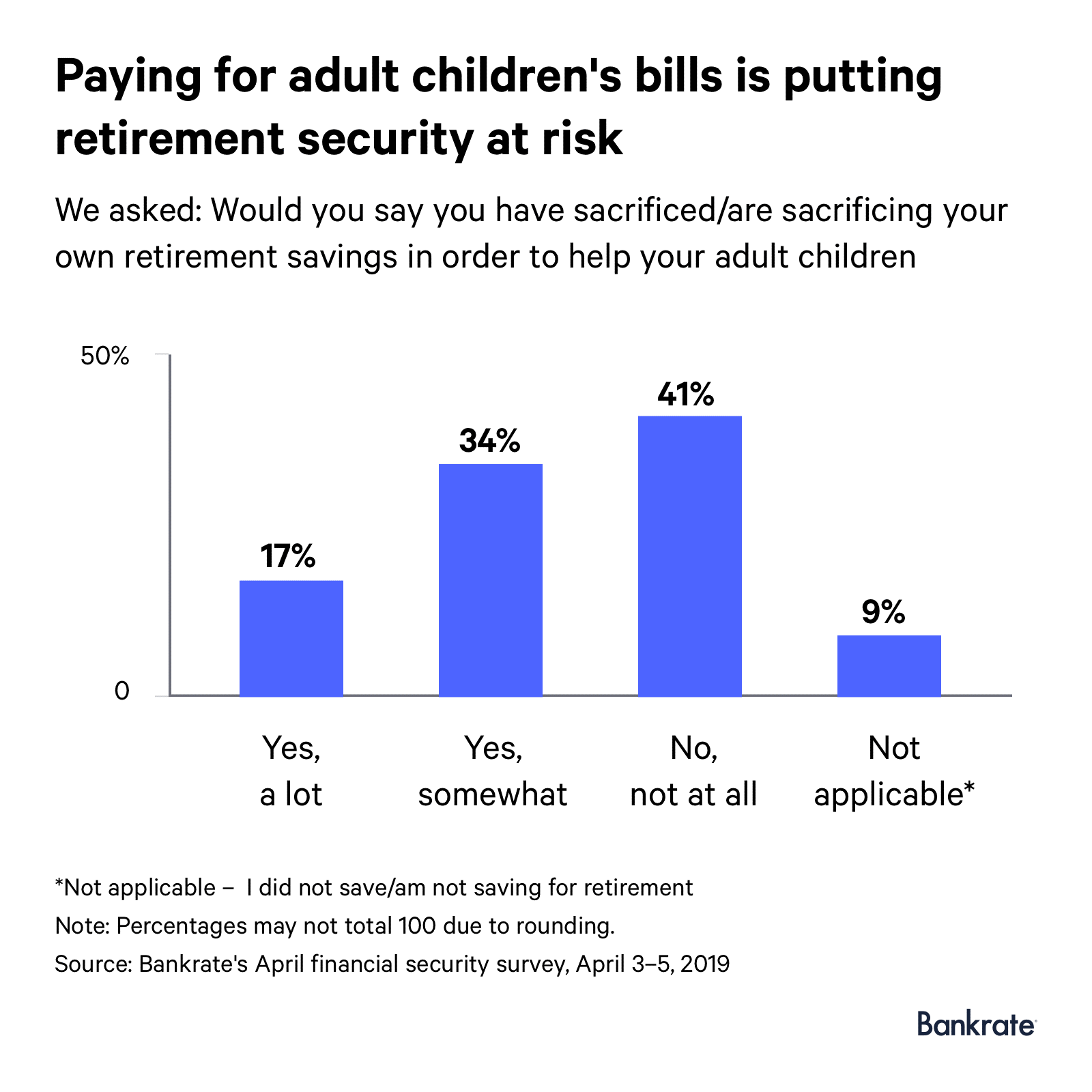

According to a recent study from Bankrate, half of parents financially helping their adult children are placing retirement savings at risk.

I know it’s a challenge to place parameters on adult children who require financial assistance. However, to plan adequately for retirement, it’s important to establish rules and take to heart the words – “enough is enough.”

It’s a tough lesson for some, but once learned, never forgotten. There’s nothing inappropriate about maintaining boundaries and saying “no” to obligations that may place your personal financial security in jeopardy.

For example, we witness parents who extend themselves to co-sign for children. We know of those who lend to friends and family members only to be disappointed when loan obligations are not met. It’s acceptable to establish in a household budget, charitable intentions and gifts; it’s honorable to help people you love who are in need.

However, it’s best to understand upfront what the financial impact to your personal situation is going to be. Know your boundaries and adhere to them. If you say ‘no’ enough, others will respect them, too.

Inside of all of us is a little superhero we have the opportunity to call upon.

Bigger-than-life heroic financial actions come down to small, consistent steps.