3 High-Yield Buyout Candidates To Pad Your Portfolio

I remain intrigued by what I see as an investor hatred of stocks of companies that own infrastructure assets, primarily assets that support the energy sector.

Despite solid earnings reports, and growing cash flow coverage of dividends, share prices in the group remain low and fall even farther on any piece of perceived negative news. It has been frustrating to own stocks in this sector, yet any review of financial results shows that many of the companies are doing well, and the stocks are deeply undervalued.

I have thought and wondered what might trigger a renewed interest in energy infrastructure stocks, and what might trigger a rebound in share values. Personally, and for my readers, I am comfortable adding shares on the cheap if my analysis shows the dividends are sustainable.

However, I wouldn’t complain if share prices started to move higher, and yields came down back to more believable levels. I think it could be the very high yields themselves that scare investors away from these stocks.

One potential for share price gains is buyout transactions by private equity making offers to acquire whole publicly traded companies. The private equity money wants to own infrastructure assets that throw off huge cash returns. It’s the general investing public that is having a hard time seeing the value of these companies after recent share value struggles.

Recently I’ve had my eye on three high-yield stocks where the potential of a buyout offer is very much on the table.

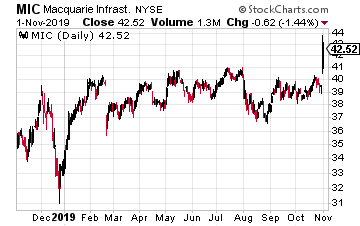

This is an easy one. Last week Macquarie Infrastructure Corporation (MIC) made an official announcement that it intends to “actively pursue strategic alternatives including a sale of the Company or its operating businesses as a means of unlocking value for shareholders.”

The MIC share price jumped 8% with this press release. During the earnings call, management said that it would take the rest of 2019 and into the early months of 2020 to evaluate the options. Any deal could push the share price 10% to 20% higher.

While waiting, management also confirmed the $1.00 per share quarterly dividend would continue through 2020 unless a deal was finalized.

That big dividend gives MIC a current 9.3% yield.

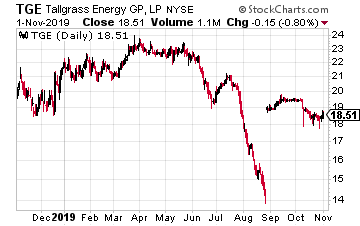

Tallgrass Energy LP (TGE), currently trading at $18.60, has recently been offered $19.50 per share in a “take private” offer by Blackstone Infrastructure Partners. Earlier in the year, Blackstone acquired the Tallgrass general partner interest.

Now it wants the operations of the company. This is a stock that traded in the mid-$20’s earlier this year, and the $19.50 is a low-ball offer that should get negotiated higher by the special Tallgrass Board of Directors committee.

I’m looking for a final offer of at least $24 per share.

In the meantime, the TGE dividend increases each quarter, and the current yield is 11.8%.

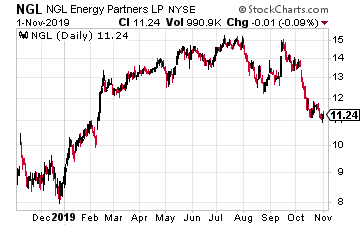

NGL Energy Partners (NGL) traded for as much as $15.40 per share in the 2019 third quarter. Nothing has changed concerning the company’s prospects, yet now shares are trading hands at $11.20.

With a $1.4 billion market cap, NGL could be scooped up by any number of well-heeled private equity firms.

The $0.39 per share quarterly dividend is secure, despite the 14% yield.

Even if an offer is not made for NGL, the large share price swings in this MLP make it easy to swing a trade for significant capital gains.

A climb back up to $15 works out to a 35% gain from the current value. This is a very real possibility and while we wait we get paid 14%.

Disclaimer: The information contained in this article is neither an offer nor a recommendation to buy or sell any security, options on equities, or cryptocurrency. Investors Alley Corp. and its ...

more