Record Breaking Silver Factors In 2015 Can Make 2016 Quite Interesting

There were two record-breaking silver factors in 2015 that could turn out to be quite an interesting development for 2016. The figures that make up these separate factors don’t seem so striking until we combine them and study at the trends.

This is what I enjoy doing the most. Why? Because I can see interesting developments that aren’t readily apparent when we look at the figures or data individually. By combing this data, we can spot noteworthy trends that would likely set up the market for stunning price movements in silver.

For example, 2015 turned out to be a record year for total U.S. and Indian silver imports. Combined U.S. & Indian silver imports didn’t just surpass the previous record set in 2014… IT SMASHED IT by 20%:

As we can see, U.S. and Indian silver imports surged to 14,446 metric tons (mt) in 2015, up 20% from 12,045 mt in 2014. This turns out to be a cool 464 million oz (Moz) of silver. Furthermore, the combined silver imports of these two countries accounted for 53% of total global mine supply. Thus the percentage of U.S. and Indian silver imports versus global mine supply continues to grow from 29% in 2012.

Note: While it’s confusing to some readers to see figures stated in metric tons and troy ounces, that is due to the way it’s reported by the industry. I could convert everything to one standard, say metric tons, but this wouldn’t help because many official sources report data in troy ounces. So, the reader just has to get used to making the conversion by using the following: (1 metric ton = 32,150 oz).

Investors need to realize that the U.S. and India importing 53% of total mine supply is a significant figure. I would imagine India is importing a lot of silver not only because of it’s an excellent investment at the low $15 price, but due to their huge demand for future solar installations.

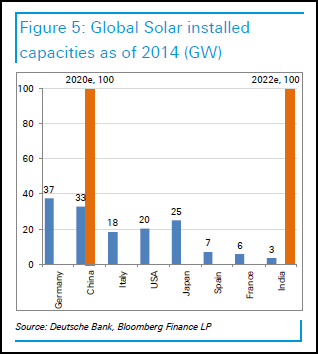

India Plans To Get Stupid With Massive New Solar Installations

India plans to bring online 100 Gigawatts (GW) of solar installations by 2022. As of 2014, they only had 3 GW of solar installed. India’s drive to add that much solar to their energy mix will consume a great deal of silver. I don’t see their silver imports falling off a cliff anytime soon. That being said, I would like to say a few things about the solar industry.

As I have stated in several articles and interviews, large solar power installations are not economically viable when we consider their full cycle costs over their lifespan. Just about every cash flow analysis I have studied on Solar Farms and large installations show they don’t pay back the originally investment over the functional lifespan of the project (20-25 years).

However, to make these BOONDOGGLES somewhat feasible, the public utilities pay the Solar Farm 2-3 times higher the going wholesale electric rate. I am not saying this occurs on every project, but I have seen it to be the industry standard. Why? Because the Solar Farm can’t pay its bills over the lifespan of the project when it has to compete with regular (coal or natgas fired plants) wholesale electricity rates.

So, even though I would advise the Indian Government or private companies in the country not to waste their capital dumping it into Solar Projects, they will continue to do so by installing 100 GW by 2020.

According to the recent article, Tilting at Windmills, Spain’s disastrous attempt to replace fossil fuels with Solar Photovoltaics:

The gold rush to get the subsidy of 47 Euro cents per kWh began. Because the subsidy was so high, far too many solar PV plants were built quickly — more than the government could afford. This might not have happened if global banks hadn’t got involved and handed out credit like candy.

Even before the financial crash of 2008 the Spanish government began to balk at paying the full subsidies, and after the 2008 crash (which was partly brought on by this over-investment in solar PV), the government began issuing dozens of decrees lowering the subsidies and allowed profit margins. In addition, utilities were allowed to raise their electric rates by up to 20%.

Solar companies went bankrupt after the financial crash, including the Chinese company Suntech, which sold 40% of its product to Spain. About 44,000 of the nation’s 57,900 PV installations are almost bankrupt, and companies continue to fail (Cel Celis), or lay off many employees (Spanish photovoltaic module manufacturer T-Solar).

Do you see the problem here? First, the utilities were allowed to raise their rates 20%. Why would the utility companies have to raise their rates if Solar was such a technological innovation for the world?? Second, at the time of the article (Sept 2015), 44,000 of the nations 57,000 PV installations were nearly bankrupt. Does this sound like a commercially viable enterprise?

Well, we humans… especially the ones making policy decisions in governments, will not learn from Spain’s Solar Industry disaster. Basically, the less economic sense things make to Governments, the more STUPID they become.

Again, it doesn’t bother me one bit that India plans on consuming millions of ounces of silver to build their massive solar farms and installations. Why? It’s less silver remaining for the market and investors. Thus, it adds more pressure on the silver market going forward.

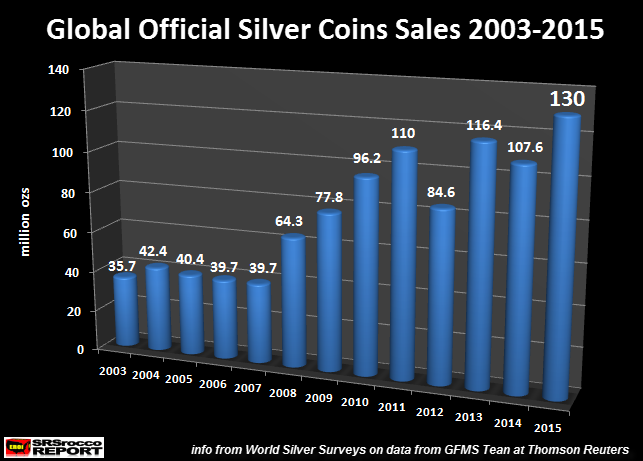

Official Silver Coin Sales in 2015 Smash Previous Records By Wide Margin

Another record silver factor that occurred in 2015 were Official Silver coin sales. Not only did Official Silver coin sales hit 130 Moz in 2015, it surpassed the previous record set in 2011 (116.4 Moz) by a hefty 12%:

While there have been some down years (2012 & 2014) since Official Silver coin sales jumped in 2008, I don’t see this trend reversing anytime soon. Furthermore, the massive amount of increased debt and leverage in the financial system since 2008 only guarantees that demand for Official Silver coins will become even stronger in the following years.

As I mentioned in my article, Silver Eagle Sales To Jump 25% Due To Deteriorating Market Conditions:

Silver Eagle sales will likely jump by 25% in the first quarter due to deteriorating market conditions. During the first three months last year the U.S. Mint sold 12 million Silver Eagles. Already, sales of Silver Eagles have reached 13 million. There are two weeks remaining in March and the U.S. Mint will likely sell another two million. This will put total Silver Eagle sales for the first quarter at 15 million….. the highest ever.

Already the U.S. Mint sold 13.9 Moz of Silver Eagles and there is a week and a half remaining in March. We will easily hit the 15 Moz mark by the end of the month. If the U.S. Mint can continue pumping out 1 Moz of Silver Eagles per week and if demand also remains strong, we could see total sales for 2016 reaching 50-52 Moz.

Just think about the huge increase of U.S. and Indian silver imports and record Official Silver Coin demand in 2015. If these two trends continue to grow in 2016, it could turn out to be quite an interesting year.

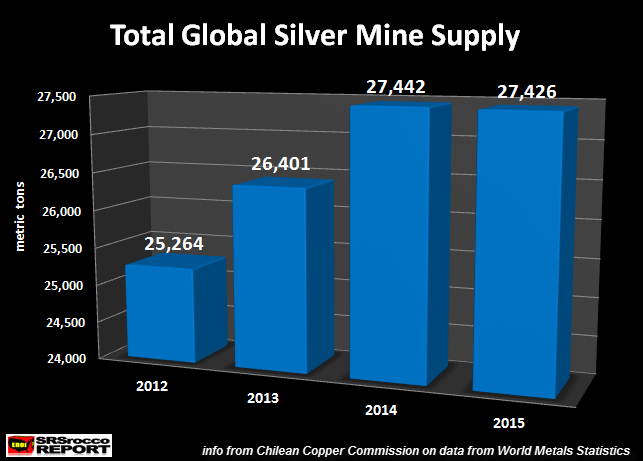

One more thing. I don’t know if you all noticed in the first chart, but according to the data put out by the World Metals Statistics, they show a slight decline in global silver production in 2015:

The World Metals Statistics shows 2015 global silver production down slightly from 27,442 mt in 2014 to 27,426 mt in 2015. I thought world silver mine supply would be down 1-2% in 2015, but I don’t have all the detailed data on all foreign countries.

I do believe global silver mine supply will be lower in 2016 due to the shutting down of several base metal mines. If the price of copper falls even lower in the second half of the year, we could see even more copper mines shut down… thus causing more declines of by-product silver production.

When you add up all of these silver factors, I believe 2016 could surprise investors even though we are currently experiencing a short-term bullion bank precious metal price take-down.

Disclosure: None.