A Closer Look At Fading Rate-Hike Expectations For The U.S

Is the Federal Reserve still pondering a rate hike in 2015? Possibly, but the recent weakness in employment growth and industrial activity suggest that keeping the Fed funds rate close to zero may persist for “much longer, well into 2016 or potentially even beyond,” counsels Jan Hatzius, Goldman Sachs’ chief economist, in a note to clients.

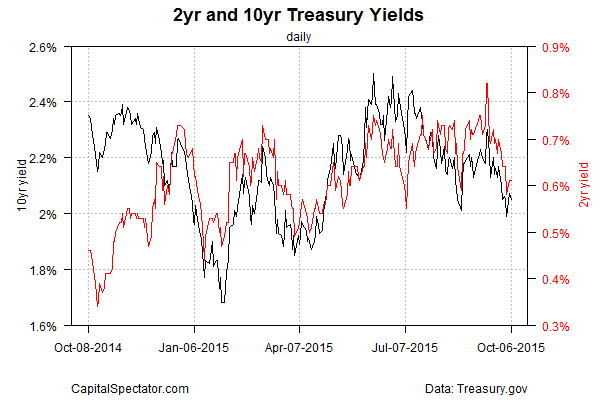

The Treasury market appears to be pricing in that outlook. The 2-year yield, which is highly sensitive to rate expectations, remains well below its recent highs. Briefly rising above 0.8% last month, the 2-year yield has since fallen sharply, holding steady at 0.61% this week through yesterday (Oct. 6), based on Treasury.gov’s daily data.

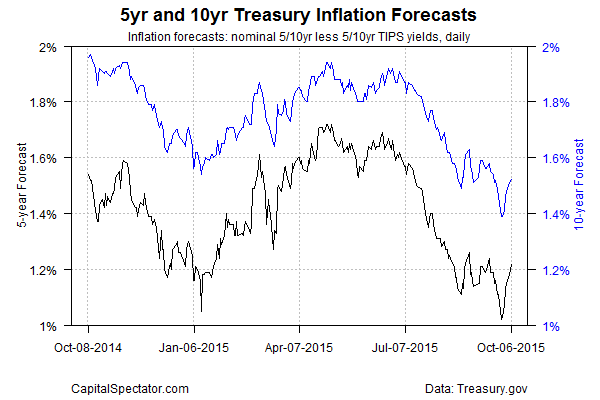

Meanwhile, the Treasury market’s inflation expectations have bounced back modestly in recent sessions, albeit after several months of nearly non-stop declines. The yield spread between nominal and inflation-indexed 5-year Treasuries has increased recently, to roughly 1.22% as of Oct. 6.—the highest since mid-September. Nonetheless, the 5-year’s current inflation estimate remains well below this year’s high of just over 1.7% in the spring. The crowd’s no longer cutting inflation expectations, but it’s not clear that the market’s inclined to reverse the recent trend in projecting weaker pricing pressure.

Meantime, Fed policy, as expressed through the effective Fed funds rate (EFF), appears to be signaling that the prospects are fading for a near-term rate hike. The 30-day moving average for EFF has been inching lower lately. The slight decline follows several months of increases. The reversal, although mild, suggests that the central bank is no longer laying the groundwork for squeezing policy.

The diminished odds for a near-term rate hike are weighing on the benchmark 10-year yield. Momentum for this maturity has turned negative lately, based on a set of exponential moving averages (EMAs). For the first time in months, the 10-year’s EMAs are in a bearish pattern: the 50-day EMA has fallen below the 100-day EMA, which is below the 200-day EMA.

What catalyst might revive expectations for a rate hike? Stronger economic data, of course. But in the wake of recent disappointments on payrolls and other indicators, that’s a high bar at the moment. This week’s remaining schedule for US macro releases is light. The potential for a major attitude adjustment will have to wait until next week’s September reports on consumer inflation and industrial production.

Nonetheless, some analysts advise that it’s still too early to fully dismiss the possibility of a rate hike before the year is out. “The jobs report had put a question mark on the notion that the US economy is [continuing to heal],” says Allianz Chief Economic Advisor Mohamed El-Erian. But “it is continuing to heal and I would suspect that at the end of the day there is a 50/50 chance they will hike rates in December but it’s a pretty tough call right now.”

Disclosure: None.

Comments

No Thumbs up yet!

No Thumbs up yet!