Turkey: A Weak Start To 4Q

Industrial production data shows a relatively weak start to the fourth quarter with -0.9% month on month in October. However, this should be temporary given the current pace of recovery in economic activity and attributable to the volatile nature of the industrial production index.

Source: Shutterstock

The industrial production (the seasonal and calendar adjusted, SA) recorded negative growth in the first month of the fourth quarter by -0.9% MoM, after a significant 3.4% MoM expansion in September. The contraction in industrial production shouldn't last for long given the improvement in the economic activity, though the recovery process will remain challenging given the volatile trajectory of the production and signs from the 3Q GDP data that the economic rebound is losing some momentum.

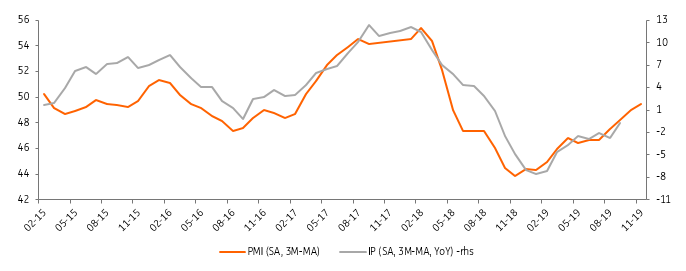

Industrial production vs PMI

Source: TurkStat, Markit, ING

Manufacturing stood out as the sole driver of the headline figure. Among the sectors, printing and reproduction of recorded media turned out to be the top underperformer with a -0.5ppt drag to the headline, followed by electronic products and other transport equipment (dominated by defence industry products), providing -0.4ppt and -0.3ppt contributions, respectively. For those lifting industrial production growth, repair and installation of machinery and equipment and chemicals stood out with +0.2ppt contribution from each sector.

Among broad economic categories, nondurable consumer goods, energy, and capital goods were drags, though the performance of intermediate goods and durable consumer goods, sustaining growth in October, should be viewed positively given that they are highly correlated with economic activity.

On the other hand, the (calendar adjusted) industrial production growth stood at +3.8% YoY, maintaining recovery after reverting to positive territory in September following a sequence of negative readings since the currency shock in 2018. Despite the October change is below of the consensus, the expectation is that the uptrend will continue in the months ahead with the support of large base effects.

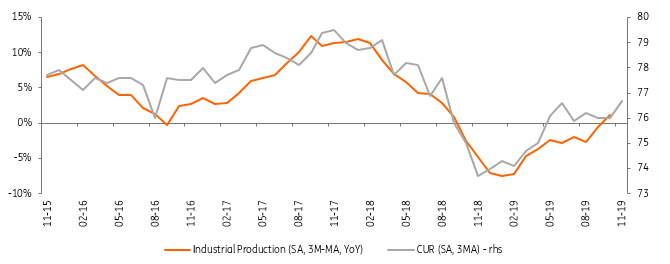

Industrial production vs CUR

Source: CBT, ING

Overall, the current pace of economic activity remains below the growth target presented in the government’s new economic program announced at the end of September.

However, it is likely that further acceleration in lending with changes in reserve requirement framework and front-loaded cutting cycle should be supportive for the outlook in the period ahead.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more